U.S. Bonds Flash Mixed Messages on Inflation as Real Yields Sink

Bondholders are increasingly willing to be paid less than nothing in the U.S. Treasury market.

(Bloomberg) -- Bondholders are increasingly willing to be paid less than nothing in the U.S. Treasury market.

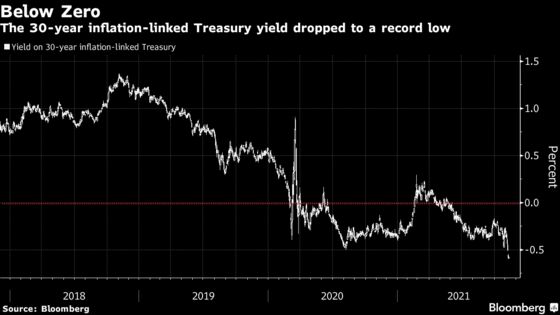

With consumer prices rising at the fastest pace since 1990, so-called real yields on U.S. government securities -- or the rate after inflation is taken into account -- have dived even deeper below zero. The rate on 30-year inflation-protected securities, a measure of real yields over the next three decades, dropped to a record low of around minus 0.62% Wednesday.

Such a slide would usually suggest the bond market has a deeply pessimistic view of economic growth, anticipating that a slowdown would keep rates low in the years ahead. But the movements in the world’s largest bond market now are defying such straightforward explanations as the U.S. emerges from the worst economic effects of the pandemic.

Strategists said the slide in real yields also reflects other factors, such as traders repositioning portfolios and concern in some corners that the high rate of inflation will become ingrained in the economy.

Jerome Schneider, head of short-term portfolio management and funding at Pacific Investment Management Co., said the downward spiral in real yields is really about ginned up inflation expectations.

“Bottom line, if you believe that real yields are attractive here, it means that your view is that longer-term inflation stays pretty dang high for a long time,” Schneider said.

He doesn’t subscribe to that view, predicting that the rise in consumer prices will start to abate in the first quarter of next year. “Real rates will get less negative as inflation gets more in the area that the Fed is more comfortable with.”

But so far, the bond market is pricing in more inflation risk, not less. Yields on 10-year Treasury inflation-protected securities, or TIPS, have dropped to around minus 1.2%. That has widened the gap between those yields and those on normal 10-year Treasuries. That difference, a proxy of inflation expectations known as the break-even rate, has grown to about 2.7%, up from around 2% in early January.

Such negative real yields aren’t unique to the U.S., said Subadra Rajappa, head of U.S. rates strategy at Societe Generale. U.K. and German 10-year real rates fell to all-time lows at minus 3.26% and minus 2.26%, respectively, on Tuesday.

Still, analysts say they have been exaggerated in the U.S. by the Federal Reserve’s Treasury purchases since the pandemic, though that will be less of a factor as the central bank winds down that buying.

Gary Pzegeo, head of fixed income at CIBC Private Wealth Management, is among those who see a mix of forces behind the fall in TIPS yields, saying it’s hard to nail down “one overarching theme.”

“There is a negative message,” said Pzegeo, whose firm manages about $96 billion in assets. “There’s low potential growth and high implied inflation, which absorbs what low nominal yield there is.”

While traditional Treasury yields rose Wednesday after the release of the consumer price index, longer-term rates are still down from a week ago, in part due to traders unwinding their short bets and speculation that the Fed could take an even more dovish shift if President Joe Biden replaces Chair Jerome Powell.

The wagers on TIPS could pay off if inflation outpaces the market’s current expectations. Were that to happen, even a buyer who purchased them at the current negative yields could profit. The securities also provide minimum coupon payments in the interim.

Yet Tom Porcelli, RBC Capital Markets’s chief U.S. economist, said the signal being sent by bond buyers is murky and out of step with his expectations for both growth and inflation.

“It can’t be a reflection of growth, because growth is quite strong,” Porcelli said. “Is it an inflation story? Inflation is going to slow down, there’s no question about that. So, I don’t know what you are left with -- and that’s the problem.”

©2021 Bloomberg L.P.