Bond Investors Fume at Price Talk Some Call ‘Bait and Switch’

Bond Investors Fume at Price Talk Some Call ‘Bait and Switch’

(Bloomberg) -- It was a big day for the bond pros at BNP Paribas SA - they were selling 1 billion euros ($1.1 billion) of the bank’s own debt to a market hungry for their product. So it’s no wonder buyers piled in when the notes were offered at a substantial discount.

As the morning wore on and the bids poured in, the price kept rising. By the time terms were set at noon, the discount was virtually gone.

“Everyone knows the game,” said Suki Mann, former head of credit strategy at UBS Group AG and founder of the CreditMarketDaily newsletter. “Banks make deals cheap enough to get investors in, then, once they’ve got huge books, they ratchet up the price.”

Times, though, are changing. Investors squeezed by ultra-low yields are getting fed up -- one fund manager complained to BNP Paribas after the June 25 issue. The data confirm their impressions: the compelling yields that pique their interest at the outset are increasingly vanishing in the marketing.

“It’s gotten much, much worse,” said Matthias Muth, a bond dealer at MRM Securities near Frankfurt and a veteran with more than 35 years in the industry.

It’s a sign of how central bank purchases and negative interest rates have distorted markets. Investors are fighting for every basis point they can get: In August, a record 30% of all investment-grade securities were bearing sub-zero yields, meaning if investors held them to maturity they would lose money. The clamor for anything that yields anything is driving prices up even more.

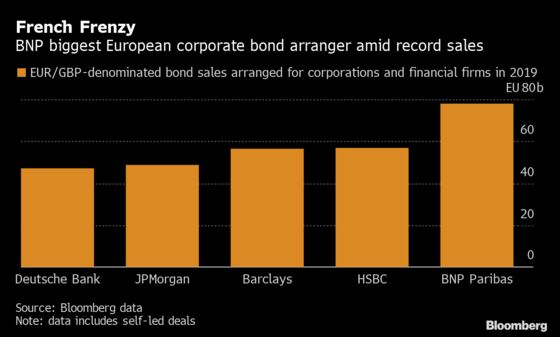

Read more about the record year in European corporate bond sales

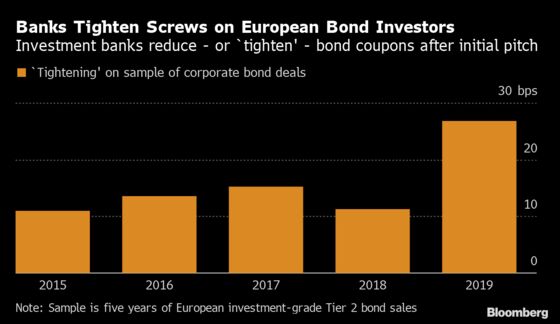

For euro-denominated tier 2 notes -- the kind of mainly finance-industry debt sold that day by BNP Paribas -- the average “tightening” between so-called initial price talk and pricing has averaged 26.9 basis points this year, according to Bloomberg data. That’s more than double last year’s 11.34 -- and the tighter the spread, the higher the price of the bond. In the investment-grade universe, the average this year is 23.1 basis points, up almost 50% from 2018.

Tactics aside, the whole process of selling corporate bonds is increasingly coming under scrutiny. Regulators have called for more detail on how the debt is allocated and fintech start-ups are pushing to automate parts of the process, reducing humans’ control.

For their part, bankers wonder what the fuss is about. They say pricing reflects nothing more sinister than supply and demand.

“The strength remains very much in the hands of issuers” as it has since the European Central Bank started adding corporate-bond purchases to its arsenal three years ago, said Tim Hall, former global head of debt capital markets at Credit Agricole SA. As years passed, the leverage “has shifted even more decisively to issuers.”

Umang Vithlani, head of credit at Fideuram Asset Management in Dublin, says he’s pulled out of deals when bonds he wanted got too expensive: he recalled a July sale by EnBW Energie Baden-Wuerttemberg AG, which included multiple managers such as BNP Paribas, Barclays Plc and Citigroup Inc. and tightened more than 70 basis points from guidance to sale. He also withdrew from one by Royal KPN NV that was arranged by BNP, Barclays, Goldman Sachs Group Inc. and Royal Bank of Scotland Group Plc.

On the other hand, he stayed in when French insurer La Mondiale’s spread narrowed a whopping 62.5 basis points from beginning to end in an Oct. 17 sale arranged by HSBC Holdings Plc, Morgan Stanley and Natixis. He still liked the 4.375% final coupon.

“People need to be invested,” said Vithlani, who oversees 4 billion euros. “Investors have no choice but to accept the price they’re being given in the primary market to get their money to work,” saying there’s sometimes not enough supply in the secondary market.

But it was BNP Paribas’ deal on June 25 that fueled a client complaint and led to an internal review. The French bank concluded that its syndicate desk in London had done nothing wrong. Alexandra Umpleby, a spokeswoman for BNP Paribas in London, declined to comment.

When the bank started circulating price guidance at 8:39 a.m. at 170 basis points over the base level known as mid-swaps, the yield curve implied that the fair market spread of its 12-year tier 2 debt was 112.7 basis points, according to Bloomberg BVAL data. As investors piled in, the bank slashed the estimate to 140 basis points. Finally, they priced at 130 basis points above the mid swaps, for a yield of 1.63%. They’ve rallied since then, along with the market, showing a spread of about 118, according to Bloomberg data.

From BNP Paribas’s point of view it was a great result. It saved more than 400,000 euros in payments over the life of the bonds and the deal was nearly four times covered, a stamp of approval in credit markets. While banks aren’t compensated based on a bond’s pricing, they are judged on their ability to drum up demand and get deals away cheaply.

“People are so desperate to get cash invested they’re not likely to punish the cheeky initial talk,” said Gordon Shannon from TwentyFour Asset Management LLP, which oversees 15.3 billion pounds ($20 billion).

Eventually, though, investors will have had enough, says Shannon. “At some point there will be a deal where enough orders drop away on the tightening that it will spoil the deal,” he said. “And the risk of that happening would scare banks from behaving that way again.”

To contact the reporters on this story: Harry Wilson in London at hwilson57@bloomberg.net;Liam Vaughan in London at lvaughan6@bloomberg.net;Donal Griffin in London at dgriffin10@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, James Hertling

©2019 Bloomberg L.P.