Bond Investor Revolt Brews Over Bogus Green Debt Flooding Market

Bond Investor Revolt Brews Over Bogus Green Debt Flooding Market

(Bloomberg) -- In a booming global bond market, there are few segments that are growing quite like the money-minting machine for green bonds. So eager are investors to buy up these notes that they’re willing to pay a premium -- and accept lower interest payments -- for the privilege.

The risk is that in this mad rush they’re letting a feel-good label obscure the reality of their investments. At the forefront of concerns among a small but growing contingent of bond buyers is greenwashing: the possibility that governments and companies are exaggerating or misrepresenting their environmental credentials or sustainability bona fides to tap feverish demand, lower borrowing costs and boost their reputation.

Any signs of deception could undercut efforts to marry making money with making progress in the fight against climate change and inequality at a critical time -- and derail one of Wall Street bankers’ fastest-growing cash cows. So even as sales of green bonds and the related universe of debt tied to broad concepts of improving the world notch record after record, a nascent investor rebellion is finding its voice.

Fund manager Aberdeen Standard blacklisted Indonesia’s green debt from its ESG funds due to deforestation risks. NN Investment Partners dumped its holdings of Poland’s green bond, citing the country’s unclear climate policy. In the corporate market, Actiam passed on a bond to finance eco-conscious renovations at Amsterdam’s airport because plane travel is inherently polluting. And Toyota Motor Corp.’s sale to fund safety research was rejected by Impax Asset Management, which figured that was something carmakers do anyway.

“What greenness you’re getting from those assets can really vary,” said Ashley Hamilton Claxton, head of responsible investment at Royal London Asset Management, which oversees about 148 billion pounds ($204 billion) of assets. “We want to put more money into green assets in the long term, but do it in a smart way.”

It’s a quandary that’s drawing a fresh look from regulators too as the market tops $2 trillion. A new generation of environmentally conscious and socially aware consumers has already embraced clothes made with organic cotton, coffee harvested with fair-trade principles and carbon offsets that promise to wipe away the guilt over jetting off to the beach, even as critics see many of the efforts as ineffective. Investors with the same goals must now parse a whole rainbow of eco-friendly debt, from bonds that fund windfarms to those helping polluters transition to cleaner tech -- even if most simply see these bonds as “green.”

The European Union is working on a set of standards that will require more rigor and accountability from issuers, while the U.S. Securities and Exchange Commission has created a task force focused on rooting out misconduct in so-called ESG investing that considers environmental, social and governance issues.

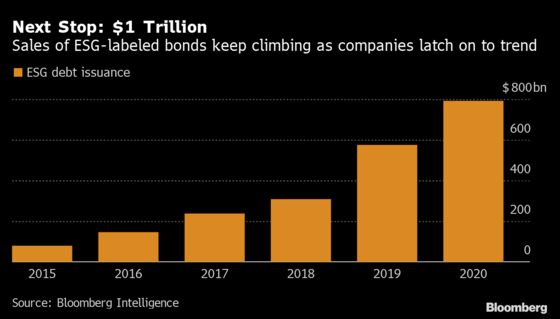

There’s certainly a lot to scrutinize. Offerings of green, social and sustainability debt make up more than one in five sales in Europe this year, up from just 7% at this point in 2020. Latin American borrowers have been even more aggressive -- they’re already 80% of the way toward 2020’s record $10.8 billion of ESG debt deals.

Part of the increase in sales is due to borrowers rushing to issue debt before global interest rates increase any further. But a global explosion of fixed-income exchange-traded funds and mutual funds dedicated to meeting sustainable investing mandates has turbocharged the boom. Retail cash has flooded in, netting fees for portfolio managers, while also often making it cheaper to sell ESG debt instead of conventional bonds.

Estimates for the so-called greenium vary, with Bloomberg Intelligence ESG analyst Simone Andrews finding only a “modest” advantage while Citigroup Inc. sees it as high as a quarter of a percentage point. For Chinese e-commerce giant Alibaba Group Holding Ltd. that translated into paying the same to place 20-year sustainability bonds in February as for conventional debt of half that maturity.

“There are more ESG mandated assets than there are ESG securities,” said Andrew Karp, head of investment grade capital markets at Bank of America Corp., who sees the torrent of demand supporting borrowers’ price advantage.

But if borrowers are going to save money by offering green bonds, buyers increasingly want to be sure they’re getting what they pay for -- namely securities that make the world a better place.

It’s a tall order. James Rich, a senior portfolio manager at Aegon Asset Management, estimates about a third of bonds designated as eco-conscious contain elements of greenwashing, up from as much as 20% a couple of years ago.

When Indonesia sold $1.25 billion of debt in 2018, it was the largest green bond that was compliant with Islamic law. The move was widely lauded, allowing the country to pay less than its initial price guidance to the market.

Yet there were red flags beneath the green surface. The Oslo-based Centre for International Climate and Environmental Research at the time noted a “possibility that some eligible green projects include an element of deforestation.” That was a warning sign that merited further investigation for Aberdeen Standard Investments, which excluded it from its ESG funds in the second half of last year.

“We look for transparency above all,” said Kate McGrath, an ESG analyst at the firm, noting Indonesia didn’t provide investors with a specific list of projects it was seeking to fund.

In Europe, Poland was penalized by NN Investment Partners, which said in September that it sold its green bonds partly because it’s the only EU country that has refused to sign on to the bloc’s 2050 climate neutrality goal at a national level.

A spokesperson for Poland’s finance ministry said it wasn’t aware of any other investors selling its green debt because of similar concerns. Indonesia’s green bond issuance is carried out “very transparently” and was approved by a second-party reviewer, said Luky Alfirman, director general of budget financing and risk management at the finance ministry.

Money manager Tony Trzcinka of Impax Asset Management passed on sustainability bonds from Toyota, whose Prius fueled the mass adoption of hybrid electric cars. The debt was marketed as “Woven Planet” notes. Using proceeds to make cars safer, while a noble goal, pushed the limits of what he considered deserving of a sustainability label.

“It was an odd proposition,” Trzcinka said.

Royal London’s Claxton says there are often cases in which a company she likes issues a green bond whose proceeds offer no added impact relative to regular debt, despite demanding a greenium. One example: Anglian Water Services Financing Plc.

“It’s not necessarily greenwashing by Anglian, but we don’t accept just because it’s got the label that we have to buy it,” she said.

A spokesperson for Anglian said even its non-green bonds benefit from its commitment to improving the environment.

For other investors, the concern isn’t so much about the use of proceeds but the credentials of the issuer itself.

Actiam’s Chris Brils was unpersuaded by green debt from Dutch airport operator Royal Schiphol Group, which includes Amsterdam’s airport, among Europe’s busiest hubs. The company wanted to “greenify” by measures such as improving the energy efficiency of its buildings.

Trouble was, there was no plan to use the bond proceeds to tackle plane emissions amid terminal expansions. “So they will be responsible for more air traffic, not less,” the portfolio manager said.

A Schiphol spokesman said the company financially supports initiatives for cleaner fuels and is aiming for a moderate and controlled expansion. Toyota’s press office said it was important to pursue “a safe mobility society.”

This growing yet ultimately still niche investor skepticism may one day erode the greenium on debt seen to not offer a sufficient impact, but so far it’s hard to find solid evidence that the suspect bonds have been punished in the market. In the meantime, some of the world’s largest investors are going to unusual lengths to avoid being taken for a ride.

Since 2019, Lombard Odier Investment Managers has hired three analysts with training in geospatial analysis, or interpreting large-scale satellite imagery. Taking their cue from charities and campaigners who have highlighted deforestation and other biodiversity threats in the past, Lombard Odier is developing proprietary models for assessing an issuer’s green credentials.

“You don’t want to have greenwashers who are issuing nice green bonds with water biodiversity projects, but then they’re presiding over massive amounts of deforestation elsewhere,” said Christopher Kaminker, who leads Lombard Odier’s sustainable investment team. “We can now count trees from space. We know where deforestation is occurring. We’re engaging with issuers on the topic.”

Even more diligence will be needed as the boom goes parabolic. The EU has announced issuance plans that would transform it into the biggest green debt issuer in the world, while the U.K. hopes to issue the first green gilt. Meanwhile, the U.S. could turn to the securities to fund a proposed $2 trillion infrastructure bill. Corporate issuers won’t be far behind.

The many new flavors of eco-friendly debt could help investors differentiate between these offerings, if enough capital flows in and gold standards emerge. One nascent variant -- sustainability-linked bonds -- could hold issuers’ feet to the fire by penalizing borrowers that fall short of stated environmental targets, but others are shunning labels altogether.

“On green bonds, we only think they have merit to ESG investors if the issuance leads to issuers actually changing their behavior,” said Mark Dowding, BlueBay Asset Management’s chief investment officer. “If this criteria isn’t fulfilled, the green issuance is just cashing in on a trend -- at best -- and could be subject to criticisms of greenwashing at worst.”

©2021 Bloomberg L.P.