Bond Funds Aim to Win Over the Green-Curious, Not Purists

(Bloomberg Opinion) -- It’s not easy being green. Not as a bond issuer, a fixed-income fund manager or as an individual investor.

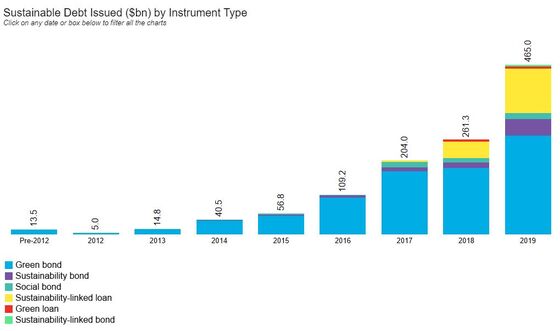

Sure, there are Green Bond Principles for governments and companies, but they’re voluntary guidelines, which helps explain why just $271 billion of the $465 billion in global “sustainable debt” issued last year was defined as green, according to Bloomberg New Energy Finance data. For mutual funds, the Bloomberg Barclays MSCI Global Green Bond Index is one of the best approximations of the market, but it has just 457 members, less than one-fourth the number in the U.S. high-yield index, making it difficult to track and heavily weighted to a few European countries.

To top it off, investors interested in climate-related investing have to wrap their heads around socially responsible investing, or SRI, and how it differs from ESG, which attempts to identify leaders in environmental, social and governance policies. My Bloomberg Opinion colleague Nir Kaissar recently wrote about the two camps. Suffice to say, it can all be enough for the average investor to give up and just go with the highest-returning option, values be damned.

Perhaps that’s why many of the biggest fixed-income funds that are considered some form of “green” choose to simplify matters. Among the five with more than $1 billion of assets, four consider the Bloomberg Barclays U.S. Aggregate Bond Index (or a subset of it) as their benchmark. That pits them against competitors like the $200 billion Vanguard Total Bond Market Index Fund, the $13.2 billion Guggenheim Total Return Bond Fund and the $13 billion DoubleLine Core Fixed Income Fund, among more than 100 others.

“The main misperception of this space is you sacrifice performance,” said Stephen Liberatore, head of Nuveen’s responsible fixed-income strategy team and manager of the $4.7 billion TIAA-CREF Social Choice Bond Fund, the largest such portfolio as measured by Morningstar Inc. Showing that an ESG fund can beat the aggregate index and “a true core fixed-income peer group, not an ESG impact peer group, is what changes people’s minds over time.”

Pacific Investment Management Co.’s Total Return ESG Fund, with $1.5 billion in assets, is handled in much the same way. “There’s no reason for there to be a difference in macro-risk factors in the ESG version” compared with the traditional total return option, said Scott Mather, chief investment officer of U.S. core strategies. “What’s different is how we go about composing the line items, how we populate the portfolio with individual bonds.”

What was evident after speaking with these fund managers is that the investing world is rushing to cater to a population of investors that I’d call the “green-curious.” That is to say, people who want to feel as if they’re making a difference with their money but aren’t willing to accept significantly higher volatility or fees to do so.

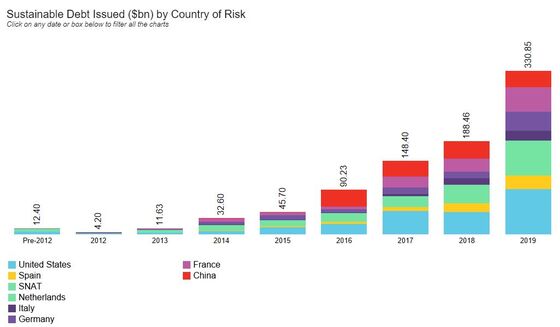

Consider, for example, that some of the biggest single holdings in ESG fixed-income funds are U.S. Treasuries. To green-bond purists, that decision would seem questionable at best, given that President Donald Trump pulled the U.S. out of the Paris accord on climate change, among other things. Debt issued by countries from France to Chile to Korea has been earmarked specifically for sustainable projects. Treasuries, by contrast, are broadly sold to finance the nation’s budget deficit, projected to top $1 trillion this fiscal year.

The counterargument is that without some exposure to the biggest and most-liquid bond market in the world, it would be tougher to track the aggregate benchmark and raise cash when needed. Plus, so far in 2020, Treasuries have been a winner: The Bloomberg Barclays U.S. Treasury Index gained 2.4% in January, beating both investment-grade and high-yield corporate bonds as well as the S&P 500 Index.

This will probably be the norm, at least until the sustainable-bond market in the U.S. matures. It’s true that 2019 marked new entrants, like PepsiCo Inc.’s inaugural $1 billion green-bond deal and Verizon Communications Inc.’s first-ever green bond, also for $1 billion. But that’s hardly enough to tip the scales. America still lags behind the rest of the world in adapting to interest in green investing mandates: Overall, just 9.6% of the green-bond index is from the U.S., compared with 39.4% for the Bloomberg Barclays Global Aggregate index, by far the largest weighting in the $57.8 trillion benchmark.

It’s worth noting that when it comes to climate change, the Federal Reserve has long stayed in its lane while the European Central Bank has swerved. ECB President Christine Lagarde said last month that climate change must be thoroughly debated among monetary policy makers and that even “green quantitative easing” could be an option. There’s a “danger of doing nothing. Failing to try is already failing,” she said.

Fed Chair Jerome Powell, in the question-and-answer segment of his press conference last week, said that the central bank would probably sign on to the Network for Greening the Financial System “at some point.” He said that it falls within the central bank’s purview to make sure the financial system is resilient to any climate risks, “but not the overall response of society to climate change. That’s not us.”

For those U.S. bond investors who want something closer to a pure green fund than the big ESG options, Pimco started its Climate Bond Fund (ticker PCEIX) in December. It considers the dollar-hedged green-bond index its benchmark and has $5 million in assets — a modest sum for a firm that oversees almost $2 trillion. Mather said he expects the fund to grow like others at Pimco, ideally quickly scaling up to the $50 million to $100 million range that he considers optimal for efficiency.

Even in that fund, “green bonds are only a subset of companies addressing the climate issues,” Mather said. “We don’t know exactly how the markets will evolve and how quickly the changes will take place, and we want to basically have a strategy that can take advantage of all those opportunities.”

Mather and Liberatore have both noticed a noticeable shift in buzz around sustainable investing during the past year. Certianly, BlackRock Inc. Chief Executive Officer Larry Fink’s annual letter to America’s CEOs, which declared that the world’s largest money manager would be “making sustainability integral to portfolio construction,” amplified that sentiment.

In a report this week, Moody’s Investors Service said it expects green, social and sustainability bond issuance to hit a record in 2020 because investors “are prioritizing the incorporation of ESG considerations and sustainability into their investment decisions and risk management.” That should support “further growth and innovation” and help diversify the market in terms of industries and regions.

“Historically, the concept of a green bond was really the purview of a supranational,” Liberatore said. Now, they’re getting “investors’ dollars closer and closer to the actual end output and impact. That’s really the most exciting part of the space.”

I can certainly see why it would be exciting for money managers to dig into projects they believe in. But the way funds are set up now reflects a prudent balance between novel opportunities and predictable performance. The sustainable debt market is still very much in its infancy, and investors need to feel comfortable walking before they can run.

This is using Morningstar Inc. criteria, which includes the following types of funds: ESG focus funds:Those that make sustainability factors a featured component of their processes for both security selection and portfolio construction. This group is the largest, and the funds in it tend to be active owners, engaging with companies and supporting — and sometimes sponsoring — ESG-related shareholder resolutions. Impact/thematic funds: Focus on broad sustainability themes, and on delivering social or environmental impact alongside financial returns. Sustainable sector funds: Focus on investment opportunities that contribute to, and aim to benefit from, the transition to a green economy in areas like renewables, energy efficiency, environmental services, water, and green real estate.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.