Bombardier Stumbles Leave CEO Just ‘One Chance’ to Regain Trust

Bombardier Stumbles Leave CEO Just ‘One Chance’ to Regain Trust

(Bloomberg) -- Bombardier Inc. Chief Executive Officer Alain Bellemare has some explaining to do at next month’s investor day.

His drastic cut to Bombardier’s cash-flow forecast on Nov. 8 is sparking Canada’s biggest sell-off in shares and bonds over the last week. It’s also undermining confidence in Bellemare’s five-year turnaround plan, which is more than halfway done and supposed to be entering a “deleveraging phase.”

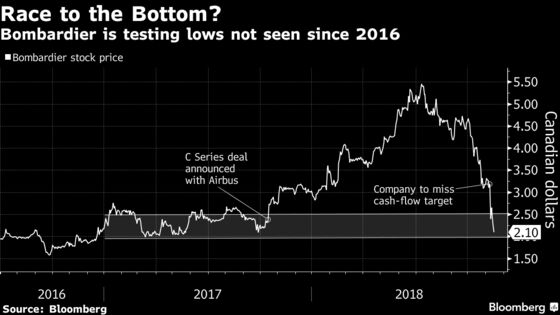

The rout is forcing investors to rethink Bombardier’s prospects -- a jarring turnabout after a year in which analysts had had ratcheted up their view on the shares to the most optimistic since 2011 as Bellemare boosted profits and ceded control of a cash-draining jetliner program to Airbus SE. With Bombardier pivoting away from commercial planes and betting its future on private jets and trains, the pressure is rising on the CEO to map out future growth.

“There is no free pass when you are a highly levered company and interest rates are rising,” said Nick Heymann, an analyst at William Blair & Co. “They have one chance to straighten things out, and that’s at the investor day.”

Bombardier fell 4 percent to C$2.17 at 1:43 p.m. in Toronto after sliding as much as 11 percent. The shares are down more than 30 percent since Nov. 7, the day before Bombardier reported earnings and pared its outlook. That’s the biggest decline on Canada’s benchmark stock index over that time frame.

Bonds Tumble

The company’s $1 billion in bonds due 2024 have dropped 7 percent to 94 cents on the dollar since Nov. 7, the worst performer among U.S. dollar bonds in Canada, according to the Bloomberg Barclays Global Corporate bond index. They fell 1.5 percent Wednesday to the lowest level since they were issued one year ago.

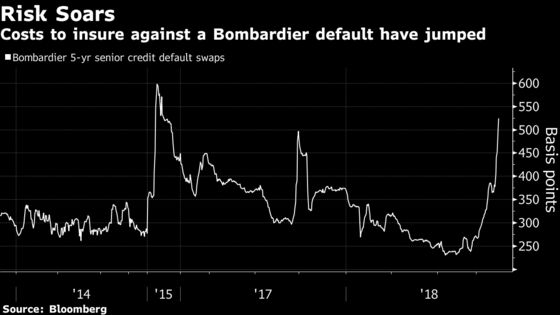

The cost to insure Bombardier debt against default for five years has widened 157 basis points since Nov. 7 to 545 as of Wednesday -- another worst for Canadian issuers. On Wednesday the credit default swaps widened 47 basis points, according to data compiled by Bloomberg.

“The market is starting to question the company’s ability to complete management’s turnaround plan,” said Brian Kennedy, a portfolio manager at Loomis, Sayles & Co in Boston, which has about $267 billion under management and doesn’t own Bombardier bonds. “The company has time to continue its efforts, but the cash burn is an ongoing concern with significant maturities that must be dealt with, starting in 2020.”

Bellemare struck a determined tone Tuesday in his first public appearance since last week’s earnings report and conference call. While defending the company’s 2019 forecast, he pledged to provide a more detailed target in the coming months. He also insisted that the company would attain its goal of generating as much as $1 billion in two years.

Upbeat CEO

“We feel it’s an air pocket but we’re very clearly on a flight path to achieving our 2020 goals,” he said at a Scotiabank conference in Toronto. “If anything, we’re even more confident today than we were a month ago about our ability to deliver on bull’s eye our 2020 targets.”

Bellemare downplayed liquidity concerns, drawing a contrast to the company’s plight when he took the reins in 2015 and “we didn’t have the liquidity.” He also accelerated his push to make Bombardier leaner last week, with 5,000 job cuts and asset sales that are expected to generate $900 million.

Bombardier had about $9.5 billion of adjusted debt as of Sept. 30, with its next major maturity coming in March 2020, when an $850 million bond comes due. The following year, notes for more than $2 billion mature, according to a regulatory filing earlier this year from the Montreal-based company.

“The company has levers to pull,” said George Westervelt, portfolio manager at Aberdeen Standard Investments in Boston, which owns Bombardier bonds as part of its more than $735 billion in assets under management. “It will take some time, but at current valuations, you’re getting paid to wait.”

Bombardier must still find a path through a maze of hurdles in the meantime. The company shocked investors last week by saying it would need to tap $635 million in proceeds from a land sale in Toronto to meet a goal of breaking even on a cash-flow basis this year, plus or minus $150 million.

‘Surprise Factor’

Next year’s goal of break-even cash flow, plus or minus $250 million, includes the impact of two one-time items. One is a $250 million restructuring charge from about the job cuts, and the other is a $250 million contingency for working-capital volatility. Analysts had been expecting free cash flow of $439 million next year, according to the average of analyst estimates compiled by Bloomberg as of Thursday.

“The pace of recovery is weaker than we had forecast,” said Chris Murray, an AltaCorp Capital analyst in Toronto. “The surprise factor which saw shares fall sharply sets the company’s progress back on rebuilding investor confidence.”

Since his appointment in 2015, Bellemare has mostly delivered on his pledges to investors by eliminating thousands jobs and raising more than $5 billion in liquidity. He also canceled a troubled private-jet program, the Lear 85, and cut financial risk by partnering with Airbus on the C Series jet program. That plane, now known as the A220, entered service at least $2 billion over budget.

Bellemare’s “excellent” track record made his latest stumbles all the more surprising, said Cormark Securities analyst David Tyerman.

“No one likes a sudden very large negative surprise,” he said, “especially given the company’s long track record of value destruction.”

To contact the reporters on this story: Frederic Tomesco in Montreal at tomesco@bloomberg.net;Paula Sambo in Toronto at psambo@bloomberg.net

To contact the editors responsible for this story: Brendan Case at bcase4@bloomberg.net, Jacqueline Thorpe

©2018 Bloomberg L.P.