BofA, JPMorgan Fueled by ‘Incredibly Strong’ U.S. Consumer

BofA, JPMorgan Fueled by ‘Incredibly Strong’ U.S. Consumer

(Bloomberg) -- If U.S. consumers are on the brink of a downturn, the nation’s biggest banks aren’t seeing it.

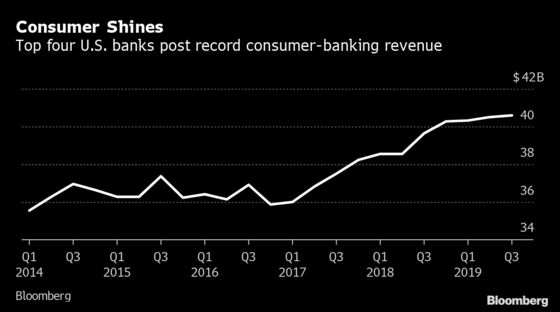

The top four lenders logged their fifth straight quarter of record revenue from businesses serving households, even as some economic indicators suggest a looming dip. The firms pulled in a combined $40.6 billion, with JPMorgan Chase & Co. powering the gains with the most revenue it’s ever generated from the business.

“The U.S. consumer is incredibly strong -- consumer spending is strong, sentiment is strong,” said Jennifer Piepszak, JPMorgan’s chief financial officer. Bank of America Corp. and Citigroup Inc. also saw consumer revenue rise, while it dropped at Wells Fargo & Co., which is constrained by a Federal Reserve growth cap.

Banks have leaned on their consumer businesses in recent years to propel earnings as their markets businesses had more turbulent results. This time around, the firms also got a boost from capital markets and trading revenue, which came in above expectations at JPMorgan, Goldman Sachs Group Inc., Citigroup and Bank of America.

“Consumers continue to show resilience and remain a meaningful source of strength in the U.S. economy,” said Goldman Sachs Chief Executive Officer David Solomon.

Bank of America said it sees no slowdown in consumer spending or any deterioration in household balance sheets. Americans with an account at the bank annually spend close to $3 trillion, the equivalent of about 15% of U.S. economic output, and this year their payments are up 6% compared with last year, CEO Brian Moynihan said.

“When consumers are employed,” said Ally Financial Inc. CFO Jennifer LaClair, “they make their payments. We are not seeing any weakness.”

Still, there were notes of caution. JPMorgan and Wells Fargo expanded loan-loss reserves for the second time in the past seven quarters. And Citigroup increased its reserves by the most in two years.

That preparation for higher future losses came even as the banks collectively shrank their consumer loan books slightly and households kept up with their monthly payments at roughly the same rate as last year, according to delinquency figures on products such as credit cards and auto loans.

Banks are increasingly pursuing individual customers on their screens. All four of the biggest U.S. banks reduced their total number of branches during the quarter in cost-cutting moves.

“One metric that we thought was interesting over the last couple of quarters is an acceleration again in mobile accounts at some of these bigger banks,” said Alison Williams, an analyst at Bloomberg Intelligence.

The gains in retail businesses, including increases in revenue from credit cards and auto lending, fulfilled analysts’ predictions that units catering to households would be a bright spot in banks’ third-quarter earnings.

Mortgage fees, however, aren’t keeping up. Wells Fargo, the country’s biggest home lender, reported its lowest quarterly mortgage revenue in a decade. In previous years, the refinancing boom that a lower-rate environment creates would have meant big gains for the country’s top banks, but competition and complex regulation has reduced the appeal of the mortgage business.

Other dark clouds include a report earlier Wednesday from the Commerce Department, which said U.S. retail sales unexpectedly posted their first decline in seven months in September.

Jamie Dimon, asked about prospects for an economic downturn, repeated his frequent admonition that contractions are inevitable. “Of course there’s a recession ahead,” the JPMorgan chief executive officer said on a call with journalists Tuesday. “Is there going to be a recession soon? We don’t know.”

To contact the reporters on this story: Gwen Everett in New York at geverett10@bloomberg.net;Shahien Nasiripour in New York at snasiripour1@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Steve Dickson

©2019 Bloomberg L.P.