Boeing Not Facing Much Bond-Market Turbulence

Boeing Not Facing Much Bond-Market Turbulence

(Bloomberg Opinion) -- Every once in a while, a highly scrutinized company comes to the debt market to raise some cash and bond traders have a chance as gatekeepers to take a stand and make it pay up. More often than not, though, they give in and look past struggles or scandals in the never-ending search for yield.

Consider Boeing Co.’s bond offering on Tuesday. In the company’s first debt sale since its second 737 Max plane crash, initial price talk called for the longest-dated securities to yield about 30 basis points more than similar outstanding obligations, data compiled by Bloomberg show. At a spread of 135 basis points over Treasuries, the 15-year portion appeared the most punitive of all.

The planemaker probably had reason to suspect it would receive a warm-enough welcome from bond investors. After all, it went ahead and easily sold $700 million of bonds in October on the same day that its 737 Max crashed for the first time in Indonesia, with prospective buyers putting in almost seven times as many orders as the amount of debt it was selling. “It’s kind of a sleepy credit: You buy, you put away, and you hope you don’t have to look at it for a while,” one investor told Bloomberg News’s Jeremy Hill at the time.

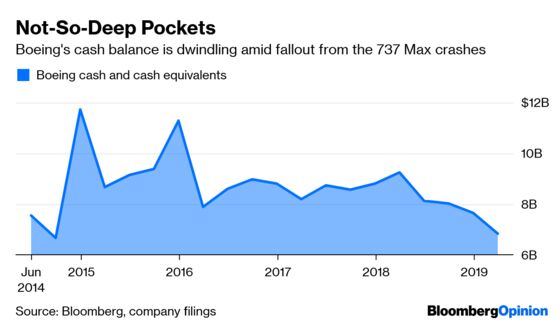

The difference between then and now is the magnitude of the crisis. As my Bloomberg Opinion colleague Brooke Sutherland wrote last week, “No one knows when the 737 Max will return to the skies, least of all Boeing.” The company is halting share repurchases and reducing the number of planes it’ll produce each month to 42 from 52. Suppliers are bracing for the worst. Estimates for free cash flow in the second quarter continue to dwindle. Just this week, Boeing confirmed that a cockpit alert linked to the two fatal accidents wasn’t working as intended on every plane, though said it didn’t deactivate that warning deliberately.

And yet the fallout hasn’t dented Boeing’s credit ratings, which are in somewhat of a sweet spot at single-A. S&P Global Ratings released a report last week calling the 737 Max grounding impact “modest so far, at least compared to the size of the company.” The analysts expect the company won’t start resuming deliveries until the end of the U.S. summer months. “We still believe Boeing has sufficient liquidity and room within the current rating to withstand this issue,” they wrote.

Indeed, Boeing had a manageable debt load of about $15.5 billion at the end of March, with maturities fairly spread out over the next few decades. According to S&P, the company will use proceeds from this deal to repay in part $1.4 billion of securities coming due over the next 12 months. Otherwise, Boeing will probably just bolster its cash reserves to wait out the 737 Max grounding, however long it may last. The company this week also revealed $1.5 billion of short-term financing from three banks.

Fitch Ratings, which affirmed Boeing’s single-A grade and stable outlook, offered a glimpse of the future. “The 737 Max will reduce much of the financial cushion at the current ‘A’ rating, leaving the company more exposed to other unforeseen events or industry downturns,” analysts led by Craig Fraser wrote. Among their “key assumptions” is that the planes return to service in at least some regions by the end of August before reaching full capacity by the end of the year. “Overall, this year will be stressful for Boeing, and Fitch expects most credit metrics will deteriorate,” they wrote.

The ratings company also expects Boeing to tap the bond markets again later this year — yet another reason traders could have sat out this offering. But it’s hard to pass up obviously wide yield spreads. If the planemaker meets or beats expectations in addressing its 737 Max debacle, Boeing should fully expect investors to be even more receptive next time around.

Long-end spreads were a bit above the market level, but that kind of concession is typical for a new bond sale.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.