Blame the Fed, Blame FedEx, Blame Whoever You Want: Taking Stock

Blame the Fed, Blame FedEx, Blame Whoever You Want: Taking Stock

(Bloomberg) -- There appear to be an endless amount of culprits that can be blamed for the latest downturn in the stock market.

You could blame China, you could blame "Tariff Man" (or "President T" if you prefer), you could blame the exponentially swirling chaos in the White House, you could blame the Democrats (S&P 500 is down almost 8% since the Dems took the House), you could blame the Fed (Trump will likely do so today no matter what happens at 2pm), you could blame the quants (Mnuchin did), you could blame the Volcker Rule (Mnuchin strikes again), you could blame crude oil and its incessant freefall (WTI now at $46 vs Oct. peak of $76), or you could find another scapegoat that suits your needs.

You could also blame the companies who are fanning fear at a time when the financial community is collectively getting less bullish, though their rationale may be a bit more legitimate than some of the reasons mentioned above.

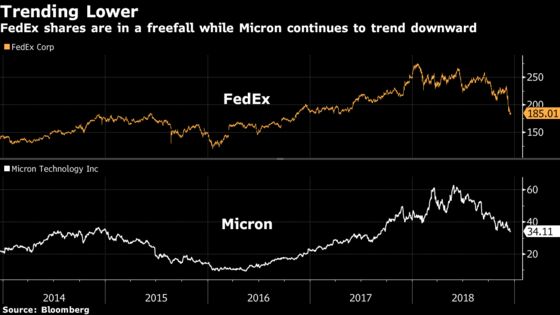

Take Fedex, a strong economic indicator by any standards, and its CEO Fred Smith, who last night blamed global trade frictions when slashing the company’s outlook just three months after boosting it -- the stock tumbled 6 percent in the post-market as a result.

Everyone is pointing to this comment from the press release -- "Global trade has slowed in recent months and leading indicators point to ongoing deceleration in global trade near-term" -- which is even more daunting ahead of the FOMC decision later today, where expectations may be turning from a "dovish hike" to an "uber-dovish hike."

But management rang even more alarms on the earnings conference call that had a lot of Wall Street heads ringing:

- "Our international business, especially in Europe, weakened significantly since we last talked with you during our earnings call in September. In addition, China’s economy has weakened due, in part, to trade disputes."

- "The secular slowdown in Chinese economy has been exacerbated by trade tensions. Spillover effects from these tensions and the fading tech cycle have negatively impacted growth throughout Asia."

- "Continued tariff and trade concerns and uncertainty in Asia are impacting our business there"

Et Tu, Micron?

Micron is less of an economic bellwether than Fedex, though the $38 billion market capper is still a core member of a cyclical sector like the semiconductors. Shares of the largest U.S. maker of computer memory chips are getting walloped by ~8% on a weak top and bottom line forecast in addition to a worrying reduction to its capex forecast.

Management blamed weak near-term industry supply/demand dynamics, but sounded bullish on the long-term trends and on their ability to withstand pressure from the trade war.

"During the last few months, we successfully leveraged our global supply chain to mitigate the impact of the China trade tariffs to less than 50 basis points to our consolidated fiscal first quarter gross margin," management said on last night’s earnings call. "We expect to be able to mitigate approximately 90% of the impact from tariffs starting in January 2019."

While that type of talk should assuage investors more than say, what Fedex was clamoring about, the sellers appear to be far outnumbering the buyers in the early going.

A Rotation Worthy of Attention

But the drubbing for both FedEx and Micron makes sense. Underwhelm the Street by an unforgivable amount and your stock should tank, especially in a time when all rallies are almost immediately faded and any bad news is double or triple punishment for the related security.

A good example of this is the action in Philip Morris yesterday, when a sell-side downgrade sparked sent shares of the megacap tobacco stock down by almost 8% and finishing the day as the worst performer in the S&P 500.

What’s interesting is the multi-day underperformance of the most defensive sectors in the market, for example the utilities and the consumer staples, of which Philip Morris is a towering figure as the fifth-largest weighting in the S5CONS index.

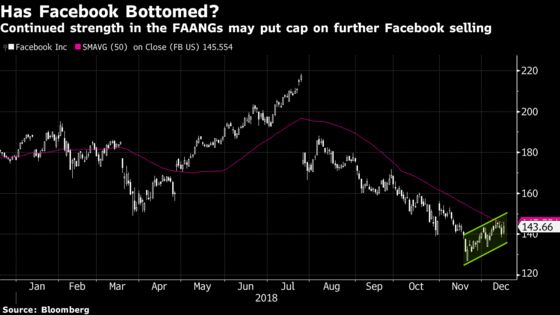

Couple that with Tuesday’s eyebrow-raising rally in the large-cap tech space, notably among the FAANGs (ML FANG index jumped 2.2%), and you have the makings of an intriguing rotation that could dispel the notion that everything is risk-off at the moment.

This morning is already a different story, as yet another bombshell report on Facebook is hitting the stock (shares are already off by 1.3%): The NY Times said Facebook gave Microsoft, Amazon, Netflix, Spotify and other major tech companies more access to users’ personal data than previously disclosed.

Meanwhile, the WSJ has a lengthy article on Apple’s struggles in branching out to India titled "It’s Been a Rout." The piece talks about the tech giant’s falling market share, revenue tracking well below expectations, and top leadership ranks "in turmoil."

But if the FAANGs can shrug all of this off and follow through with a second day rally, I’d expect more calls for a bottom in Facebook (already up 9% from its mid-November low), a floor for momentum stocks (MTUM is holding long-term support at the $100 mark), and a resurging interest in what is no longer the most crowded trade in this market.

Sectors in Focus Today

- Transports, especially UPS, and trade proxies, like Boeing and Caterpillar, may be weak with FedEx selling off ~6% on a cut to its outlook

- Semiconductors, especially semicap names like Applied Materials and Lam Research, will likely fall after Micron sold off on a disappointing forecast in addition to a reduction in its capex view; another cautious sector note from Morgan Stanley (see below for details) won’t help things

- Electronics services names like Sanmina, Celestica and Plexus could outperform after Jabil pops more than 10% on a better-than-expected 2Q forecast

- Recreational vehicle stocks after Winnebago handily beat estimates for earnings and revenue

- Consumer staples, especially in the packaged food space, after General Mills rose ~3.5% on an EPS beat

Notes From the Sell Side

Credit Suisse global strategists, in their outlook for next year, argue that the economic shocks of 2018, namely China and Europe, "are now largely in the price." They make a whole host of sector changes, including upgrading U.S. small caps, raising semiconductors, downgrading U.S. banks, and keeping their overweight standpoint on U.S. growth.

Morgan Stanley yet again is hammering the semiconductors space, recommending investors to remain cautious ahead of 2019 as a bottom is not yet in sight. Notes that every key market except wireless infrastructure has taken a turn for the worse, and "the problem is the trajectory of growth in these markets likely deteriorates further, which we think results in additional inventory drawdown at customers and distributors." The bank is also downgrading Analog Devices to an equal-weight in conjunction with the broader note.

Atlantic Equities is reducing earnings forecasts for the big banks on expectations for less net interest margin expansion, lower loan growth and higher net charge offs. Price targets are now 8%-15% lower and its rating on JPMorgan moves to a neutral from an overweight after its outperformance over the past year; the analysts favor Bank of America and Citi.

Tick-by-Tick Guide to Today’s Actionable Events

- Today -- IPO lockup expiry: AUTL, ECOR

- 7:00am -- GIS, WGO earnings

- 7:30am -- GSK CEO Emma Walmsley on Bloomberg TV

- 8:00am -- AXTA 4Q guidance call

- 8:30am -- Current Account Balance

- 8:30am -- PAYX earnings

- 8:30am -- GIS earnings call

- 9:00am -- LLY 4Q guidance call

- 9:30am -- IPOs to start trading after the open: Aptorum (APM)

- 9:30am -- PAYX earnings call

- 10:00am -- Existing Home Sales

- 10:30am -- DoE oil inventories

- 12:00pm -- Top Live blog on Goldman Sachs’ 1MDB woes

- 2:00pm -- FOMC rate decision

- 2:10pm -- Alan Greenspan on Bloomberg TV

- 2:30pm -- Fed Chair Powell holds press conference

- 4:00pm -- TWST earnings (timing uncertain)

- 4:05pm -- MLHR earnings

- 4:15pm -- NCS, PIR earnings

To contact the reporter on this story: Arie Shapira in New York at ashapira3@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Steven Fromm

©2018 Bloomberg L.P.