Blackstone’s GSO Distressed-Debt Bets Post 30% Quarterly Loss

Blackstone’s GSO Distressed-Debt Bets Post 30% Quarterly Loss

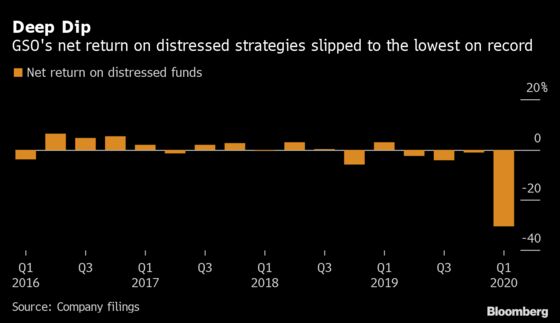

(Bloomberg) -- GSO Capital Partners LP reported its worst performance in at least a decade from distressed-debt investments, even as the pandemic boosted potential targets in March to almost $1 trillion.

The credit arm of Blackstone Group Inc. recorded a negative 30.3% net composite return on distressed assets during the first quarter, the company said in a Thursday statement. The losses were driven in part by energy, which hobbled returns and remains a deeply troubled sector, management said during a quarterly earnings call with investors.

The loss compares with a 3.1% gain in the same quarter a year earlier and negative 1.1% in the fourth quarter of 2019, when energy was also a drag. More recently in April, a supply glut and crashing demand sent oil futures prices into negative territory during April.

“We’re already seeing opportunities appearing” from dislocation in the markets, but “distress takes time to play out,” Chief Operating Officer Jonathan Gray said on the call. The firm is “looking for businesses that are cyclically, not secularly, under pressure,” Gray said. “Strong companies and properties recover and flourish” with time.

Distressed net returns for the last 12-month period were also down 35.3%, according to Blackstone’s presentation. The figure measures profit after taxes, fees and carried interest. By contrast, GSO posted a negative 14.1% net return on its performing credits for the quarter.

Investors in distressed debt struggled to post gains last year because low interest rates and frothy credit markets helped troubled issuers find new backers to bail them out. Now the coronavirus pandemic has created new targets for credit investors to buy at steep discounts, with the total approaching $1 trillion at one point during March, according to data compiled by Bloomebrg.

“It’s a better investment environment than it was before both the leveraged loan and high-yield market sold off,” Gray said on the call. Those markets have recovered some ground, “but there are still plenty of names that are trading at big discounts, so for our distressed arm that creates opportunities.”

The firm deployed roughly $3 billion during the first quarter, management said. The amount of assets specific to distressed-debt investing is around $7.8 billion, about 1% of Blackstone’s total $538 billion pool, according to a company representative.

The entire credit unit managed $128.7 billion as of quarter end, a step down from $132.3 billion in the same period last year. Credit remains the third-largest business unit at Blackstone.

Blackstone’s supply of unused capital available to invest in credits of all types and insurance stood at $27.9 billion, down from $28.7 billion in the prior quarter.

Distressed Leader

GSO is watched closely by investors because it’s one of the largest and most active distressed-debt investors. Returns in the field can vary widely each quarter, with results depending in part on when troubled issuers decide to take corrective actions and when deals are completed as well as court rulings.

GSO’s composite gross return for distressed assets before fees and deductions was down 31.8% for the quarter, better than the 41% drop in the benchmark ICE BofA distressed-debt index. The results trailed both GSO’s 3.7% gain in the first quarter of 2019 and negative 0.8% in the fourth quarter of last year.

In contrast to GSO’s recent performance, a Blackstone-backed hedge fund recorded one of its best-ever months with bets in corporate distress as the coronavirus pandemic started taking hold in Europe. Bybrook Capital’s master fund gained about 17% net of fees in March and 19% for the first quarter, Bloomberg reported.

Read More: Blackstone-Backed Hedge Fund Sees Record Gain on Distressed Bets

©2020 Bloomberg L.P.