Canada’s Housing Market Is Roaring Back With Black-Tie Condo Launches

Canada’s Housing Market Is Roaring Back With Black-Tie Condo Launches

(Bloomberg) --

More than a thousand brokers and agents sipped wine and nibbled ahi tuna hors d’oeuvres at the black-tie sales launch of a luxury condominium in downtown Toronto last month.

The 62-story proposed skyscraper in Yorkville, one of Canada’s most exclusive neighborhoods, features black marble kitchens with built-in wine troughs, an indoor-outdoor infinity pool and a piano lounge. Units range from about C$650,000 to almost C$1.97 million ($1.48 million) for a 1,163 square foot three-bedroom suite. Add in parking for C$169,000.

“They’re selling out like crazy,” said Dawna Borg, a broker at RE/MAX Premier Inc., who spent more than three hours at the sales office one Saturday trying to snag units for her clients. “We had to go back Sunday and just wait for a new allocation to come out, and we still didn’t 100% get what we wanted.”

A spokeswoman for RioCan REIT, which is developing the building with Metropia and Capital Developments, said more than 70% of the units have been sold since the mid-September launch.

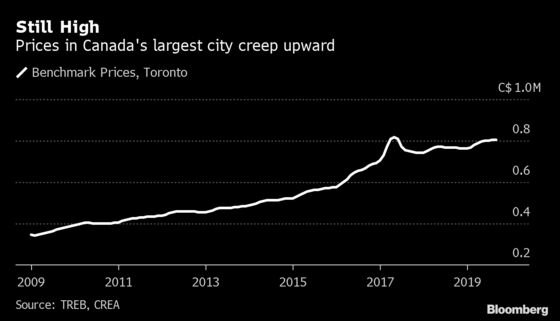

Canada’s housing market is back with a roar this fall. Benchmark prices in Toronto jumped 5.2% to C$805,500 in September from a year earlier, only about $10,000 below their peak two years ago. While prices in Vancouver continue to fall, sales rebounded 46%, the third month in a row of year-on-year gains. Montreal and Ottawa continue to chug along and even in beleaguered Calgary, the energy capital of Canada, sales rose 8.2% in September from last year.

In contrast, the housing market is sobering up in Manhattan, as resale prices for condos and co-ops dropped 8% in the third quarter from a year earlier, the biggest drop since 2012. Sales have also declined over the past two years.

New regulations in Canada, including stricter mortgage criteria and tax increases to cool foreign purchases, helped stem runaway price gains through 2018. Those appear to have been largely absorbed -- aided by the global drop in borrowing rates, record immigration and a strong labor market. That’s put housing affordability front and center in the federal election campaign.

“I worked 90 hours in one week,” said Simeon Papailias, co-founder of the Real Estate Center, a real-estate management company. He sold 30 condos in one weekend. “The pre-sale market is on fire again but resale has picked up too: We’re having the best back-to-back month since 2017.”

Supply Puzzle

Canada’s population rose 531,497 to 37.6 million in July, the biggest year-over-year increase in records going back to the 1970s, according to the federal statistics agency. Many are ending up in Toronto’s booming tech and financial-services sector or attending the city’s many universities and colleges.

Supply is lagging demand with even the International Monetary Fund this week urging Canada to ease a thicket of red tape constraining construction such as permitting and zoning delays. Government-related fees on new Toronto homes are among the highest in North America, according to an industry group, which can add almost C$223,000 to the cost of a new detached home.

“The demand side of the equation is incredibly strong and the supply side is a puzzle that has not been figured out by anybody,” said Sasha Cucuz, a partner at Greybrook Capital, a private-equity firm with a North American real estate portfolio valued at more than C$15 billion, including projects underway. “When you couple those together, that’s an indisputable upward pressure on pricing, flat out, whether it’s rental or housing.”

Election Outcome

Both the Liberal and Conservative parties are promising to make home buying more affordable on the campaign trail. Prime Minister Justin Trudeau is pledging to boost the cap on homes eligible for a 10% government-equity stake to almost C$800,000 in costly markets like Vancouver and Toronto. The Conservatives plan to extend mortgage amortizations and review the mortgage stress test for first-time buyers and remove it from mortgage renewals.

Though the fall housing market has kicked off with several big condo launches, the buying period before the election will still be a bit iffy, Borg, the RE/MAX broker, said.

“No one really knows what to expect: Who’s going to be in power? Are there going to be new rules? Because they really need to revisit that stress test -- it’s causing people a lot of stress,” Borg said.

Prices in Calgary and Vancouver are still below recent records, down 5.9% and 7% respectively, according to Teranet-National Bank Home Price Indexes.

Rental Pain

Lofty home prices have pushed many prospective buyers into the rental market, where vacancy rates are at historically low levels and rents continue to rise.

“Despite purpose-built apartment construction rising four-fold since 2014, rental supply is unlikely to come close to demand in the coming years,” Robert Hogue, senior economist at Royal Bank of Canada, said in a report last month. “A deliberate policy to boost rental supply is needed—with specific targets and incentives to achieve them.”

The bank estimates that the number of renter households will jump by an average of 22,200 per year in Toronto. To restore equilibrium over a two-year time frame, Toronto would have to add an average of 26,800 units per year.

The federal government housing agency has ramped up incentives for new rental development, including a rental-financing initiative, but projected rental supply falls short of what’s needed and needs to at least double, Hogue said.

--With assistance from Erik Hertzberg.

To contact the reporter on this story: Natalie Wong in Toronto at nwong133@bloomberg.net

To contact the editors responsible for this story: David Scanlan at dscanlan@bloomberg.net, Jacqueline Thorpe

©2019 Bloomberg L.P.