Bitcoin Futures ETF Mania Cools as Wall Street Hits Pause Button

Bitcoin Futures ETF Mania Cools as Wall Street Hits Pause Button

(Bloomberg) -- What was expected to be a wave of U.S. exchange-traded funds tied to Bitcoin futures has all but dried up -- for now -- after off-the-charts demand for the first one rattled Wall Street’s all-important middlemen.

Wall Street analysts expected as many as four Bitcoin futures ETFs to begin trading in October following the Securities and Exchange Commission’s tacit approval of the structure; instead only two products, from ProShares and Valkyrie Investments, debuted. While optimism still abounds that several funds could begin trading in the coming weeks, a similar ETF from VanEck is in a holding pattern even though the 75-day window for regulators to reject or delay it has “long passed.”

The delay is due in part to reticence among futures commission merchants, which act as an intermediary between derivatives-backed funds such as the ProShares Bitcoin Strategy ETF (ticker BITO) and the exchanges where those contracts trade. Known as FCMs, these firms -- typically banks -- handle buy and sell orders for futures contacts on behalf of their clients and then settle those trades with exchanges such as the Chicago Mercantile Exchange.

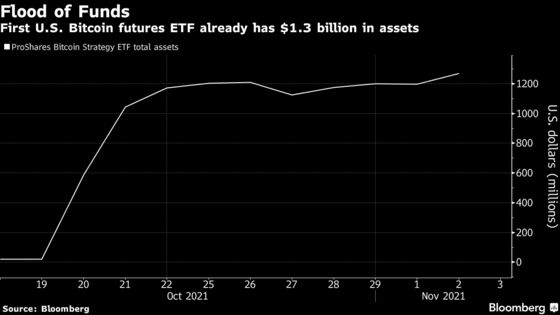

In normal circumstances, it’s a fairly mechanical, out-of-the-spotlight relationship. However, the stunning appetite seen for BITO -- which last month accumulated more than $1 billion in assets in just two days, among the biggest launches ever -- has FCMs thinking twice. The cash influx quickly ate up the balance sheet of the firm acting as an FCM for BITO at its launch, putting regulatory capital limitations against the Bitcoin futures exposure in sight, according to a person familiar with the matter.

While Valkyrie’s ETF managed to debut two days after BITO -- and with somewhat less fanfare -- the dizzying demand for the first fund has created a crunch for next-in-line issuers such as VanEck. It has yet to launch its pending Bitcoin Strategy ETF (ticker XBTF) despite being ‘post-effective’ -- essentially, cleared to begin trading by the Securities and Exchange Commission -- because of the difficulty of lining up FCMs, according to a person familiar with the matter who asked not to be named. Beyond VanEck, there are a handful of applications for similar futures-based products filed with the SEC.

Exacerbating the issue is the fact that the futures world has been slowly hollowed out for years. Coming into 2020, a wave of workforce cuts and consolidation buffeted the industry, including firms that facilitate trading, like FCMs. That’s created a form of “concentration risk” for FCMs, given how the industry has shrunk over the past decade.

And so even as cryptocurrencies and their signature volatility have emerged as a profitable new asset class -- allowing smaller, non-bank players such as ED&F Man and StoneX to gain a foothold -- their size creates limitations.

“If you have one customer that’s bringing a lot of risk to your book, that’s an additional capital hit,” said Craig Pirrong, a finance professor at the University of Houston’s Bauer College of Business. “If you look at volatility, if you look at concentration risk, if you look at size, it’s all conceivable that those would raise -- that that would cause issues with FCM capital issues.”

ED&F Man and ProShares declined to comment. VanEck did not respond to multiple requests for comment.

“You have some of the smaller FCMs that may be more retail-ish, so they have retail-type clients. And then you have some of the very large banks and some of them have an appetite for these new products, some don’t. You have only a few well-capitalized, non-bank FCMs that I think are potentially a good fit for this type of business,” Vincent Angelico, StoneX’s head of clearing and execution services, said in a phone interview. “We are excited for the opportunity to provide access to the markets for some of the well-capitalized ETFs.”

The inflows into BITO have also forced the fund to push out purchases into further-out futures to avoid breaching front-month position limits. The ETF has already purchased December contracts just one trading day into November, Bloomberg Intelligence analysts noted Tuesday.

The logjam is a product of pent-up demand for Bitcoin exposure in an ETF wrapper, something that had been out of reach in the U.S. despite a nearly decade-long effort. Cameron and Tyler Winklevoss filed the first application for a Bitcoin ETF in 2013, but the SEC demurred for years, citing concerns over everything from price manipulation to illiquidity. The landscape changed in August, when SEC head Gary Gensler signaled he’d be more open to a futures-backed fund than one that physically held Bitcoin.

While Gensler’s reasoning lies in the fact that futures trade on the regulated CME, Bitcoin derivatives require more margin. For example, commodity futures typically carry about 10-to-1 leverage ratio, meaning that for every $100 million of exposure, a $10 million deposit is required. For $100 million of Bitcoin futures exposure, however, about $40 million must be put up, according to Bloomberg Intelligence analyst Mike McGlone.

The bottleneck will ease as larger FCMs and other participants grow more comfortable with the Bitcoin futures market, according to Jesse Proudman, co-founder and chief executive at Makara, a crypto advisory firm.

“It’s going to take time for all of the participants to gain comfort with how this works,” Proudman said. “Large providers are in wait-and-see mode, while the smaller providers are hungry and ready to adapt.”

©2021 Bloomberg L.P.