Billionaire’s Light-Touch Approach at Sotheby’s Faces First Test

Billionaire’s Light-Touch Approach at Sotheby’s Faces First Test

(Bloomberg) --

The morning French billionaire Patrick Drahi took control of Sotheby’s he emailed staff at the 275-year-old auction house with a message of stability.

“With my family, we are very honored and proud to assume the long-term ownership of Sotheby’s,” he said in the Oct. 3 note. “You have my full commitment and competence as we look to enhance Sotheby’s for the next 275 years and beyond.”

The day before, he had told a packed employee town hall in the seventh-floor auction room at the company’s New York headquarters that significant cost cuts were on the way. However, job losses were not, according to two people who attended the meeting.

The mood of continuity was also evident in his pitch to financiers for his purchase of the auction house, as they were told that his plan is “to maintain the current, well-performing strategy of the business.”

This doesn’t sound quite like the Patrick Drahi who earned his fortune from debt-fueled takeovers of at-risk communications companies, imposing deep cost cuts, layoffs, asset sales and complicated borrowing structures, all while filling key roles with trusted lieutenants. The announcement Monday that Charles Stewart would become chief executive officer of Sotheby’s is a prime example of the last tactic, given his role as chief financial officer at Altice USA Inc., a telecom company controlled by Drahi.

As Sotheby’s prepares to kick off its November auctions with an Impressionist and modern art sale that will feature Claude Monet’s “Charing Cross Bridge,” its new owner faces an important test. The company expects the month’s sales to bring in about a quarter less than a year ago. That may require some belt-tightening. But for the business to thrive over the long term, Drahi may need to stand by his pledge to workers, and pursue a different playbook than the one he’s used to build his business empire.

“It’s obvious that you don’t manage an auction house the way you manage a telecom carrier,” said Frederic Ichay, a telecom and technology M&A lawyer based in Paris. For example, halving staff would be unthinkable, he said. “Auction houses typically take years to establish long-lasting bonds with families that have art works to sell and families that could be buyers. That’s the heart of the business.”

Spokesmen for Sotheby’s and Drahi declined to comment.

Diversified Fortune

Though the French-Israeli tycoon turned a $9,000 student loan into $12 billion over the course of his career, he had never made much of a mark on the art world, so his run at Sotheby’s caught the community by surprise. Apart from offering a way to ensure his legacy, the purchase will help diversify Drahi’s fortune away from the communications assets that dominate his holdings.

The 56-year-old has certainly made an impression on that industry. He bought French carrier SFR for more than 17 billion euros ($19 billion) in 2014 and pledged to preserve jobs. About a third of the workforce has been cut. Revenue is now growing, though the parent company is burdened by a mountain of debt. Drahi has also made clear his views on salaries. After he bought Cablevision Systems Corp. in a $17.7 billion deal the same year, he said he prefers to shell out “as little as I can.”

Drahi could avoid deep cuts at Sotheby’s and still have some wiggle room to reduce pay.

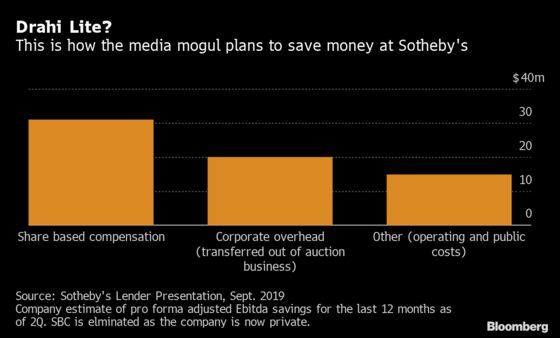

According to a presentation given to potential buyers of bonds to finance the acquisition that was seen by Bloomberg, Drahi plans to achieve $66 million in cost savings at the auction house, amounting to about 43% of adjusted earnings before interest, taxation, depreciation and amortization in the second quarter. A big portion of that -- some $31 million -- reflects the end of share-based compensation.

Eliminating stock payments is to be expected, given the company’s new private status. However, it remains to be seen how much, if any, of these funds resurface as another form of compensation.

The question of whether the broader planned cost cuts materialize plays into investors’ and credit rating companies’ concerns about leverage. These worries stem from Drahi’s approach to financing the acquisition and his move to introduce complexity into Sotheby’s structure, both of which are typical of his modus operandi.

Sotheby’s now carries an extra $1.1 billion of debt raised through a loan and a bond to pay for the purchase. S&P Global Ratings said the additional borrowing will help drive leverage to 6.6 times Ebitda after the acquisition from 4 times previously, informing its one notch cut in the company’s grade to B+. S&P notes that leverage can fall as costs get eliminated. Similarly, Moody’s Investors Service said that risks connected to “high” leverage are offset in part by an expectation that costs will fall -- including the end of share-based compensation.

Drahi’s decision to reorganize Sotheby’s into three separate entities raised concerns for some potential investors by heightening some of the risks of the debt, according to people familiar with the debt marketing who asked not to be named. The auction house would be in one entity, which would be the issuer of the loan and bond. The company’s real estate, including buildings in London and New York, would be located in a new PropCo division, and the auction company would lease back the property.

Auction Estimates

The asset separation means that were the auction business to run into difficulties, creditors may struggle to stake a claim on proceeds from any property sales. This is something would-be lenders had to consider seriously, given signs of cooling global growth. And the business may already be slowing. Sotheby’s low estimate for its busy November auction season is $522.3 million, 24% less than last year. Rival Christie’s projects a 27% drop.

To assuage investors’ concerns, Drahi had to offer improved pricing on the loan, tighter covenants, a requirement for a quarterly investor call, and a limit on payments like dividends that could disadvantage debt holders. He still must confront the need to reduce leverage in a trickier environment.

“In this high end art market, where customers often have wealth largely tied to the stock market, things can drop off very quickly,” said Cameron Bybee, an analyst at S&P. “Sotheby’s does have a good brand name and its market position shields the business a little, but the company would still need to show a deleveraging trend” to achieve a rating upgrade.

The backdrop for sales will certainly test Drahi’s decision to fill key positions with some of his trusted top executives. It’s not just the CEO who will have no experience running an auction house (though neither did outgoing Chief Executive Tad Smith -- he had been CEO at Madison Square Garden Co. and a president at Cablevision before taking the top job in 2015, when Dan Loeb’s Third Point LLC was Sotheby’s biggest shareholder). Jean-Luc Berrebi, who ran Drahi’s family office and is a former chief financial officer of HOT, an Israeli carrier that’s part of Drahi’s telecom empire, will be the new CFO. Dennis Okhuijsen, an adviser at Altice Europe, is listed as a key person in the lender presentation.

“It’s a bit like going to the circus at this point,” said Todd Levin, a New York-based art adviser. “I don’t know what act will appear next under the big tent. It was the Dan Loeb act, and then it was the Tad Smith act, and now it’s the Drahi act. As Drahi paid a high premium for the stock, everyone is just waiting to see how the company will perform under his control.”

--With assistance from Laura Benitez.

To contact the reporters on this story: Sally Bakewell in New York at sbakewell1@bloomberg.net;Angelina Rascouet in London at arascouet1@bloomberg.net;Katya Kazakina in New York at kkazakina@bloomberg.net

To contact the editors responsible for this story: Rebecca Penty at rpenty@bloomberg.net, Jennifer Ryan

©2019 Bloomberg L.P.