Biggest U.S. Banks Seen Adding to Reserves for Pain Yet to Come

U.S. banks aren’t taking any chances.

(Bloomberg) -- When it comes to loan losses sparked by the Covid-19 pandemic, U.S. banks aren’t taking any chances.

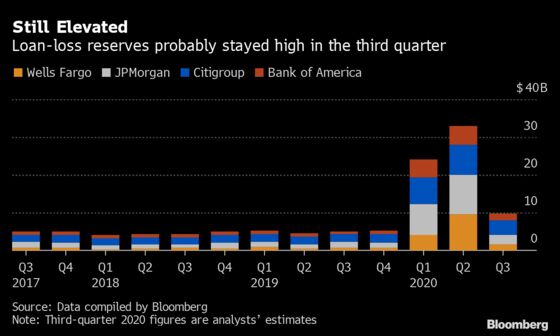

The nation’s four biggest lenders probably set aside about another $10 billion for bad loans in the third quarter, according to analysts’ estimates compiled by Bloomberg, even though stimulus moves by the government and Federal Reserve have so far staved off a spike in missed payments.

While the third quarter’s tally is well below the pace of the first half, it means that the banks will not only have covered the losses they’ve seen since the start of the pandemic, but also added almost $50 billion to reserves for future pain. Investors’ big question will be whether that comes from typical caution, or if the banks are seeing worrying signs as forbearance programs wind down and stimulus efforts get bogged down in a partisan fight.

“There is still an enormous amount of uncertainty about how this will ultimately unfold, particularly for the consumer,” JPMorgan Chief Financial Officer Jennifer Piepszak said last month. But she added that “things are looking better than we would have thought.”

As giant lenders including JPMorgan Chase & Co., Bank of America Corp., and Wells Fargo & Co. report third-quarter results this week, analysts expect a slight uptick in net charge-offs as some loans sour. That will still be outstripped by banks’ provisions as they prepare for losses from industries hurt by lockdowns and consumers who are unemployed. Already in the first half, JPMorgan added $6.6 billion to its reserve for credit-card losses, while Wells Fargo boosted its commercial-loan reserve $6 billion.

Piepszak said the bank’s provisions are based on economic assumptions that are more severe than what its economists expect to happen, and the company wasn’t predicting a meaningful reserve build or release in the third quarter.

Bank of America Chief Executive Officer Brian Moynihan said last month that reserves and charge-offs would probably be “modest.” And Citigroup CFO Mark Mason said the bank expected additional reserve increases would be “meaningfully lower” than earlier in the year.

Betsy Graseck, an analyst at Morgan Stanley, estimated that loan-loss provisions declined about 61% from the second quarter. “It’s hard to know how low provisions will go, as reserve builds should be close to complete,” Graseck said, adding that the most recent unemployment rate of 7.9% is well below the roughly 9% year-end estimate that most banks used to build reserves.

Banks may be setting aside more than they need for loan losses to take advantage of strong trading revenue and the fact that they can’t return excess capital to shareholders. The Fed this month extended through the rest of the year its unprecedented constraints on dividend payments and share buybacks for the biggest U.S. lenders.

Here are some other key indicators to watch when JPMorgan and Citigroup kick off earnings week on Tuesday:

Trading Revenue

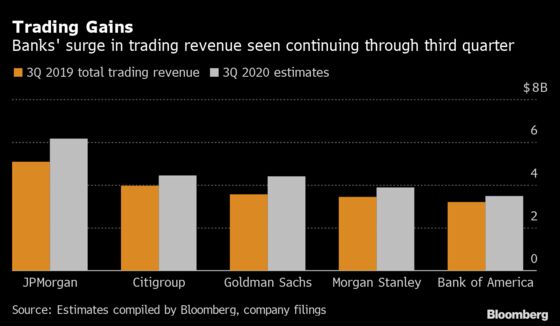

Trading will probably again drive big revenue gains for banks, as volatility sparked by the pandemic boosts demand from investors moving in and out of stock and bond holdings. Firms recorded a surge in the business last quarter, with the five largest U.S. banks hauling in a total of $33 billion.

JPMorgan’s revenue from trading probably jumped 20% from a year earlier, Piepszak said last month. Moynihan at Bank of America estimated an increase of 5% to 10%, and Mason said Citigroup’s figure probably climbed by a percentage in the low double digits.

Trading activity remained elevated through the third quarter, James Mitchell, an analyst at Seaport Global Securities, said in a note. Mitchell cited “particular strength in global equities volumes” last month.

Revenue at the five banks is expected to jump 16% from last year to $22.3 billion, according to analysts’ estimates compiled by Bloomberg. JPMorgan probably posted the biggest haul, at $6.2 billion, followed by Citigroup and Goldman Sachs.

Net Interest Income

Net interest income -- the difference between what banks charge borrowers and what they pay depositors -- is expected to have continued falling in the third quarter as near-zero interest rates hurt margins.

Lower short-term rates will crimp banks’ income from lending more than it will lower their deposit costs, analysts at Goldman said in a report last week. Net interest income will decline by about 3% for the largest banks from the previous quarter, according to Goldman.

Even though the yield curve has steepened, meaning the spread between short-term and long-term rates increased, that does little to help banks’ margins because most loans are priced at spreads to Libor or similar short-term benchmarks. Banks are hard-pressed to narrow those spreads when interest rates are low, creating a slow grind on interest income over time.

The average net interest margin for U.S. banks dropped to an all-time low of 2.89% in the second quarter, according to Federal Reserve data going back to 1984. The average for the biggest four lenders was 2.2% in the period. It will probably drop to 2% in the third quarter, according to Goldman estimates.

Headcount

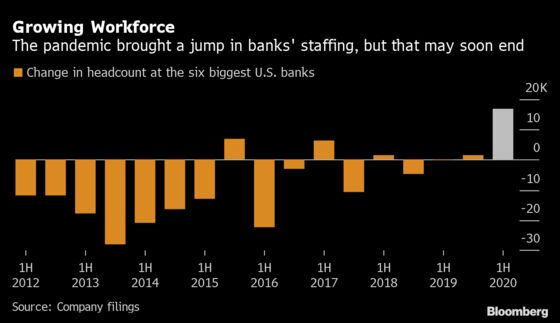

Wells Fargo just eliminated more than 700 commercial-banking jobs, pursuing a plan of workforce reductions that could eventually number in the tens of thousands, people with knowledge of the matter said last week.

The bank is the industry’s biggest employer, but more widespread job cuts are coming as banks abandon their no-layoff policies put in place as the pandemic began to intensify earlier this year. Wells Fargo, Citigroup, JPMorgan and Goldman Sachs are all trimming staff. Bank of America is standing by its pledge through the end of the year, Moynihan said earlier this month.

With firing freezes in place and new employees still joining, headcount at the six biggest banks rose by almost 17,000 in the first half. That was the biggest increase since the mergers of the financial crisis.

Credit Cards

With banks sitting on a mountain of deposits, investors have been eager to see how they’ll be deployed. There’s at least one area firms have already shown an appetite for: credit cards.

Assets tied to credit-card loans and other revolving forms of credit were down about 6.3% in August, which is better than the 34% decline banks reported for the end of the second quarter, according to data compiled by the Fed.

And more improvement could be on the horizon. Lenders mailed out 150 million card offers to consumers in August, a 56% surge from the previous month as “industrywide volume has continued to bounce back from the low in June,” Moshe Orenbuch, an analyst at Credit Suisse Group AG, said in a note to investors.

©2020 Bloomberg L.P.