Biggest Private Coal Miner Goes Bust as Trump Rescue Fails

Biggest Private Coal Miner Goes Bust After Trump Rescue Fails

(Bloomberg) -- Robert E. Murray, the U.S. coal baron who pressed the Trump administration to help save America’s struggling miners, placed his company into bankruptcy as demand for the fossil fuel continues to weaken.

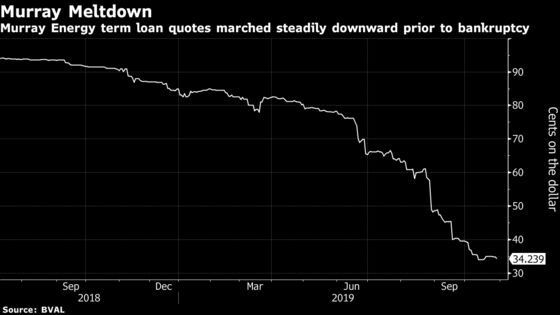

Murray Energy Holdings Co. filed for Chapter 11 protection in the U.S. Bankruptcy Court in Columbus, Ohio, to restructure more than $2.7 billion of debt. The miner -- the largest privately owned U.S. coal company -- reached a restructuring support agreement with lenders who hold more than 60% of a $1.7 billion loan, the company said in a statement. The deal provides a new $350 million loan to keep operations going during the reorganization.

The bankruptcy comes more than a year after the Trump administration’s efforts to subsidize struggling nuclear and coal-fired power plants failed, shot down by Trump’s own appointed energy regulators. Some of those plants were Murray Energy’s customers. Robert Murray, a big donor to Trump’s campaign, was instrumental in setting his energy agenda and has hosted multiple fundraisers.

The company said Tuesday that it named Robert D. Moore, Robert Murray’s nephew and former chief operating officer, as president and chief executive officer of Murray Energy. Under the restructuring agreement, the lender group will form a new entity -- called Murray NewCo -- that would seek to acquire the company’s assets, with Murray as chairman and Moore as CEO.

Waning Demand

The company’s collapse underscores how deeply cheap natural gas and renewable energy resources have cut into coal’s share of the U.S. power market. Cloud Peak Energy Inc., Cambrian Coal Co., Blackjewel LLC and Blackhawk Mining LLC have all filed for bankruptcy this year. Their downfall mirrors waning demand for fuel that as recently as 2003 accounted for more than half of all U.S. power generation.

Murray warned in 2017 that the shifts in the industry could push it into bankruptcy. The company initially chose to avoid that route and persuaded creditors to ease its debt load somewhat. But analysts said this left the company at a disadvantage with rivals because it remained saddled with high costs and interest expenses.

Murray shuttered some of its West Virginia mining operations in September, citing weak market conditions.

Workers Bracing

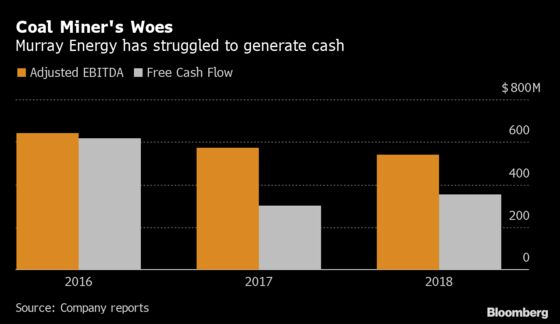

The bankruptcy provided a rare peek at the privately held miner’s financial performance, with documents posted on the company’s website showing adjusted earnings before interest, taxes, depreciation and amortization (Ebitda) of $542 million in 2018, down from $574 million the prior year and $643 million in 2016. Revenue from coal was $2.5 billion in 2018, up from $2.2 billion in a year earlier.

The lender agreement calls for the reorganized company to reject any existing collective bargaining agreement between the company and employees, the disclosures show. Murray, which has more than 5,000 employees -- 2,400 of whom are active union members -- said it faces more than $8 billion in liabilities for various pensions and benefit plans.

“We have high-powered legal, financial and communications teams in place that will fight to protect our members’ interests in the bankruptcy court,” United Mine Workers of America International President Cecil E. Roberts said in an emailed statement. “I want our active members to know that this filing changes nothing as far as the current terms and conditions of employment.”

Union Roots

Robert Murray, who began working in coal mines at 16 to support his family, has had deep union ties. Before starting his St. Clairsville, Ohio-based company in 1988, he spent 31 years at North American Coal Corp., eventually becoming CEO.

In his telling, he was fired in October 1987 after refusing to get behind the company’s plan to reincorporate in Delaware and shed obligations to some 1,800 retirees whom Murray had spent years working alongside. North American Coal said at the time that it changed CEOs as part of a broader strategy to diversify into non-coal operations.

As his own company struggled in recent years, Murray continued to be one of the industry’s biggest cheerleaders.

He led the fight against President Barack Obama’s clean-air rules, filing numerous legal challenges and calling the Democrat “the greatest enemy I’ve ever had in my life.” His company donated $1 million to a political action committee backing Trump’s agenda in the 2018 election.

Murray listed almost 100 affiliates that were also filing for Chapter 11. Foresight Energy LP, a struggling St. Louis-based coal miner in which Murray bought a controlling stake, wasn’t part of the proceedings, Murray said in a statement. Foresight skipped an interest payment this month and is evaluating its options as a 30-day grace period expires this week. Moore, Murray’s new CEO, is also Foresight’s CEO.

Kirkland & Ellis LLP is providing legal advice to Murray Energy. Evercore is Murray’s investment banker, and Alvarez & Marsal is its financial adviser.

The case is Murray Energy Holdings Co., 19-bk-56885, U.S. Bankruptcy Court Southern District of Ohio (Columbus).

(Michael R. Bloomberg, the founder and majority stakeholder of Bloomberg LP, the parent company of Bloomberg News, has committed $500 million to launch Beyond Carbon, a campaign aimed at closing the remaining coal-powered plants in the U.S. by 2030 and slowing the construction of new gas plants.)

To contact the reporters on this story: Jeremy Hill in New York at jhill273@bloomberg.net;Will Wade in New York at wwade4@bloomberg.net;Steven Church in Wilmington, Delaware at schurch3@bloomberg.net

To contact the editors responsible for this story: Rick Green at rgreen18@bloomberg.net, ;Lynn Doan at ldoan6@bloomberg.net, Shannon D. Harrington

©2019 Bloomberg L.P.