Biggest CLO Buyer Plots Return, Joining BofA and Pimco in Market

Biggest CLO Buyer Plots Return, Joining BofA and Pimco in Market

(Bloomberg) -- Many of the biggest whales in collateralized loan obligations are returning to the $900 billion market after spending much of last year on the sidelines, a shift that could make one of Wall Street’s biggest credit machines run even hotter.

Japan’s Norinchukin Bank, formerly the biggest buyer in the CLO market, has begun looking at deals again, according to people with knowledge of the matter. Wells Fargo & Co., absent for much of 2020, is back. Fidelity Investments has already upped its holdings in pursuit of higher yields. And Bank of America Corp., previously just an occasional buyer in the market, has purchased billions of dollars of the bonds and plans to add more.

The return of big players is an important step in the resurgence of the CLO market, which had been in the doldrums for much of last year. Investor demand for these securities translates to more money flowing into leveraged loans, the raw material that is packaged into CLOs. That inflow can help private equity firms finance more -- and potentially riskier -- leveraged buyouts. It helps business owners borrow to extract dividends from their companies. It can also fuel the kind of excess in corporate lending that regulators have been warning about for years.

But CLOs came out of the pandemic without the mass downgrades that investors had feared, a performance that has helped fuel a resurgence in demand for them and their relatively high yields. Bank of America has set up a program to steadily purchase top-rated CLOs, according to people with knowledge of the matter who aren’t authorized to speak publicly. According to Morgan Stanley research, Bank of America had just $80 million of CLOs at the end of last year.

Norinchukin Bank, often referred to as Nochu, held $73 billion of CLOs at its peak, multiples of what any other institution had. But the bank has been largely absent from buying new CLOs since 2019, when Japanese authorities clamped down on purchases of the instruments. The bank’s holdings have been dropping since late that year. That trend accelerated this year because many CLOs refinanced or reset their liabilities, and Nochu was often replaced as an investor in the process, according to people with knowledge of the matter. A representative for the bank declined to comment.

JPMorgan Chase & Co. and Wells Fargo -- which have long been among the largest buyers of CLOs -- have also increased their holdings this year, according to other people with knowledge of the matter. (JPMorgan had $29 billion of the securities at the end of last year, while Wells Fargo had $25 billion, according to Morgan Stanley.) Smaller banks including PNC Financial Services Group Inc. and Toronto-Dominion Bank also heightened their investments.

“The pendulum has swung dramatically,” said Lauren Basmadjian, head of the U.S. loans and structured credit business at Carlyle Group Inc. “A lot of investors who were absent back in 2020 returned in size.”

Pacific Investment Management Co., Blackstone Group Inc. and Fidelity have been buying more of the instruments, according to people with knowledge of the matter. Pimco is adding on risk, shifting from the shorter-dated AAA bonds that accounted for most of its purchases in 2019 to 2020 to buying securities with a range of ratings, according to one of the people. State Street Corp. has also begun to purchase European CLOs.

Deploying Deposits

Asset managers sold more than $108 billion of U.S. CLOs in the first quarter, counting refinancings, resets, and reissues, setting a new quarterly record. Until now, many of the buyers kicking up their allocations have been from the U.S.

For banks, demand is being driven by the massive amount of deposits they’ve received during the pandemic as low interest rates have expanded the money supply. Lenders in the U.S. banking system had $17.8 trillion of deposits as of the end of December, a surge of more than $3 trillion from the same period a year earlier, according to data from the Federal Deposit Insurance Corp.

Much of this money isn’t being lent out, forcing banks to invest in securities instead. A Morgan Stanley research team led by Charlie Wu expects reserves held at the U.S. central bank to expand by another $2 trillion this year.

“The big news is that the U.S. banks have stepped up and some have returned,” said Dagmara Michalczuk, a portfolio manager at Tetragon Credit Partners. “It’s been the marginal, incremental buying from new and returning investors stepping in that is making the difference.”

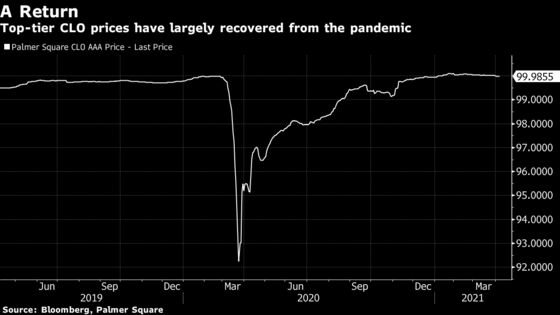

Many investors are coming back to the CLO market after sitting out for much of 2020, when money managers feared that the pandemic would trigger a wave of ratings downgrades for loans, decimating the value of riskier parts of collateralized loan obligations. Those rating cuts never really came, and now the economy is in recovery mode, resulting in more CLO upgrades than downgrades.

Supply Indigestion

The sheer volume of securities that CLO managers are producing now, both from new sales and from refinancing existing transactions, appears to have overwhelmed the increased appetite of investors. Risk premiums on AAA rated portions of CLOs, known as the discount margins, have edged higher, averaging around 1.08 percentage point as of Wednesday compared with 1.03 percentage point in mid-February, according to Palmer Square CLO data compiled by Bloomberg.

“The fact that spreads are marginally wider and not significantly wider really speaks to the all the demand brought on by the Fed’s keeping rates low,” said Dave Preston, head of structured credit research at AGL Credit Management.

Most market participants see that slowdown as a blip, and there is a swelling pipeline of upcoming deals.

“It’s fairly common to take a pause and reevaluate at the end of the first quarter,” said David Moffitt, co-head of Investcorp’s US credit management business. “I don’t see this as a rotation out of the CLO asset class. I see this more as a pause in the pipeline.”

CLOs continue to offer more yield relative to investment-grade corporate bonds. A company bond rated in the A tier, or four to six levels above junk, averages a risk premium of around 0.7 percentage point, according to Bloomberg Barclays index data, or about 0.38 percentage point less than a AAA rated CLO. And CLOs tend to carry floating rates, meaning their yields will rise as the Federal Reserve hikes.

Strong CLO issuance has translated to greater sales of leveraged loans. Companies priced more than $145 billion of leveraged loans in the first three months of 2021, including new loans and refinancings, the highest quarterly level since at least 2013.

In addition to Nochu’s planned return to CLOs, Japanese firms including Japan Post and Mizuho Financial Group Inc. are also continuing to invest, or increasing their investments. Sumitomo Life Insurance Co. has begun buying European CLOs recently, after previously focusing mainly on the U.S. market for the securities. The return of the nation’s investors to the market is a key variable for how strong demand will be in the future.

“If Japanese banks come back into the fray it will be a game changer for AAA spreads,” said Nikunj Gupta, head of European new issue CLOs at Deutsche Bank in London.

©2021 Bloomberg L.P.