Big Bond Funds Seen Primed for Global Interest-Rate Lift-Off

Big Bond Funds Seen Primed for Global Interest-Rate Lift-Off

(Bloomberg) -- For bond investors who have doubled down on bets against ultra-low sovereign yields in the U.S. and northern Europe, vindication may have finally arrived.

Money managers from the likes of Goldman Sachs Asset Management, Franklin Templeton and Aviva Investors are among those who recently extended short positions on longer-dated government debt -- wagers with the potential to pay off handsomely as a rout engulfs the global bond market.

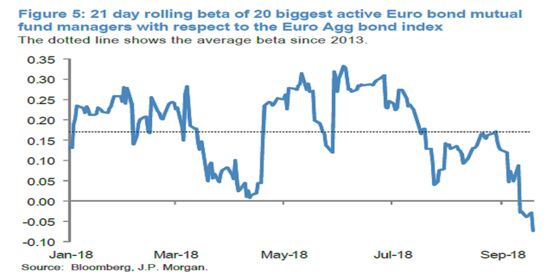

The largest 20 euro mutual funds are similarly primed to benefit, according to research from JPMorgan Chase & Co. Real-money managers shifted aggressively to a short-duration stance last month, suggesting they are relatively well-positioned for the perfect storm gripping interest-rate markets.

Stellar U.S. economic data on Wednesday, hawkish monetary expectations and stronger commodity prices have pushed 10-year and 30-year Treasuries to a breakout range, while ebbing fears over Italy’s fiscal trajectory have helped to punish German bond prices.

It all suggests large investors rooting for a normalization in the heart of the global bond market may at last catch a lucky break.

“We have a structural short duration position in the U.S. because we expect the Federal Reserve will continue normalizing policy and that inflation will increase as jobs growth and wage pressure builds,” James McAlevey, portfolio manager of the Aviva Investors Multi-Strategy Fixed Income Fund, said in an interview.

“Market participants are at a point where they can start to have a conversation about shorting the European bond market,” he said. McAlevey’s team has initiated tactical short-trades via long-dated swaps.

Goldman, Templeton

Other large investors have redoubled their bearish convictions in recent months.

Goldman went underweight European rates in its $3.4 billion Strategic Income Fund over the summer, adding to the fund’s overall negative duration stance, according to filings. The move was spurred by expectations the European Central Bank will begin raising interest rates by the fourth quarter of next year, the filing said.

The Goldman and Templeton funds have both outperformed the majority of peers in the past month.

Hard Year

DWS Group, an asset manager majority owned by Deutsche Bank AG, has also reduced European interest-rate risk in its $130 billion multi-asset portfolios. “The risk of being wrong on the long-duration side in Europe is much higher than in the U.S.,” money manager Christian Hille said in an interview with Bloomberg TV on Tuesday.

He expects the growth and inflation trajectory in the euro area will stay on course, allowing the ECB to normalize policy next year -- spurring bund yields along the way.

The past year has proven that it’s a difficult trade to get right, with many U.S. money managers, most notably Franklin Templeton, underperforming as they waited for yields to climb. Investors have also pulled more than $3 billion out of the Templeton fund in the year until the end of June, according to filings.

Overseas demand, muted inflation and subdued growth have firmed up longer-maturity sovereign-bond prices since the crisis, while any resurgence in Italian political risk could rekindle haven demand for government debt in Europe.

“I think some investors became very complacent on the outlook for long terms yields in the U.S. over the summer,” said Charles St-Arnaud, an investment strategist at Lombard Odier Asset Management in London. “We already started to recommend being underweight government bonds and reduce duration risk.”

To contact the reporters on this story: Natasha Doff in Moscow at ndoff@bloomberg.net;Cecile Gutscher in London at cgutscher@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2018 Bloomberg L.P.