Big Banks’ Mortgage Operations Lose Cash-Cow Status on New Rules

The nation’s biggest banks on Tuesday reported underwhelming results in their mortgage businesses.

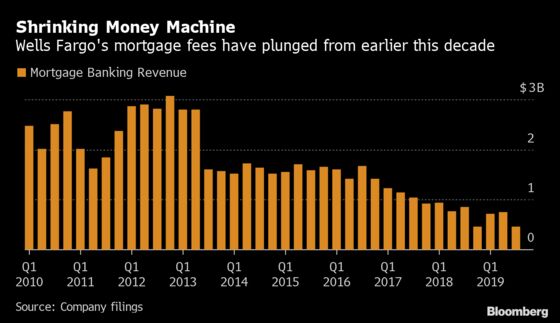

(Bloomberg) -- For the biggest U.S. banks, a mortgage refinancing boom once would’ve meant a dependable stream of profits that could swing a quarter. Those days appear to be over.

At Wells Fargo & Co., the nation’s biggest home lender, gains from underwriting an extra $12 billion in mortgages were more than offset by writing down the value of rights to fees from collecting mortgage payments. At JPMorgan Chase & Co., a one-time gain from selling home loans didn’t have Chief Executive Officer Jamie Dimon celebrating; it had him doubling down on calls for reform.

Mortgages still account for the biggest share of consumer debt, but they’re no longer the cash cow it once was for major banks. Competition from new players is part of the story; bankers also blame new rules and complex regulations for pushing them away from the market.

Citigroup Inc.’s originations almost doubled in the quarter, but its revenue from selling and servicing home loans increased by a paltry $900,000. Bank of America Corp., which reports third-quarter results Wednesday, last year relegated its once-giant mortgage business to be part of “other income.”

The nation’s biggest banks on Tuesday reported underwhelming results in their mortgage businesses at a time when home loans were more affordable and more borrowers probably would have qualified for them. During the year’s third quarter, borrowers seeking the typical 30-year mortgage saw rates advertised around 3.66%. The Mortgage Bankers Association’s refinancing index climbed to the highest level in more than three years. Last year, similar new loans averaged around 4.57%.

Credit scores, long viewed as the barometer of borrowers’ ability to make their monthly payments, have been rising for about a decade, according to Fair Isaac Corp. The average FICO score in the U.S., Fair Issac recently reported, hit a new high of 706.

JPMorgan’s card and auto lending business has generated more than four times the revenue as its home lending unit this year. That’s partly because the bank has cut the amount of home loans it holds on its balance sheet by 16%. While mortgage sales produced a $350 million gain this quarter, Dimon said banks selling loans just to buy a related security that’s treated better by capital rules isn’t the sign of a healthy market.

“I was a bit surprised by the magnitude of the sale,” said Jim Shanahan, an analyst at Edward Jones. “The size of the mortgage portfolio had declined pretty significantly.”

Dimon wrote in his annual letter to shareholders this year that the bank likely would have to change its mortgage strategy because of issues with regulatory requirements.

“That’s why I think you need some fixes in the mortgage market around securitizations,” Dimon said on a call with analysts Tuesday. Capital rules make it so “there are points in time where putting mortgages on your balance sheet just gives you a very low return.”

--With assistance from Michelle F. Davis and Gwen Everett.

To contact the reporter on this story: Shahien Nasiripour in New York at snasiripour1@bloomberg.net

To contact the editors responsible for this story: Kevin Whitelaw at kwhitelaw@bloomberg.net, Michael J. Moore, Dan Reichl

©2019 Bloomberg L.P.