Big-Bank Earnings Eyed for What They Say About Rates, Mortgages

Big-Bank Earnings Eyed for What They Say About Rates, Mortgages

(Bloomberg) -- When JPMorgan Chase & Co., Citigroup Inc. and Wells Fargo & Co. report third-quarter earnings on Friday morning, all eyes may be on qualms about rocky markets and higher interest rates, particularly with the KBW Bank Index dropping to its lowest levels since December.

"Management comments will be key," KBW equity strategist Fred Cannon told Bloomberg via email. "Credit metrics all remain excellent and credit spreads were narrow" throughout the quarter.

Watch the banks’ loan growth outlooks, “a critical revenue variable,” for clues about the fourth quarter and 2019, Bloomberg Intelligence’s Alison Williams says. Deposit pricing and curve flattening will be among risks for investors to assess, with the early-October jump in the 10-year Treasury yield raising questions around the mortgage outlook in particular. Global trade is a key concern for capital markets revenue. There may be less to worry about in the third-quarter metrics, as Williams expects "solid execution on cost goals," and still-strong credit.

The third-quarter "is an example of ancient history," as reports won’t reflect the impact of higher rates on banks’ businesses, veteran bank analyst Richard Bove told Bloomberg. Bove will be looking at metrics including accumulated other comprehensive income (AOCI) and net interest margins (NIM). He’s skeptical NIMs are getting a boost from higher rates, as banks’ actual operating environment is different from a "theoretician’s view."

When JPMorgan reports, Credit Suisse will be focused on the macro outlook, expectations for GDP growth and implications for interest rates, loan demand and credit quality migration, analyst Susan Roth Katzke wrote in a note. She’s also tracking the capital markets environment, and the health of the investment banking pipeline, with an eye toward whether the third quarter’s slowing was "simply a timing issue." Other things to watch: Asset management net flows; competition for loans and deposit pricing, fee waivers and market share shifts; Sapphire Banking and You Invest; and, "regulatory dynamics -- with new CCAR/capital requirements and CECL in focus."

For Citigroup, Katzke’s also watching macro and regulatory issues, along with updates on card NIM/net revenue margin, and growth in North America retail banking, including an early read on the national digital bank, and growth prospects in Mexico and Asia. Capital markets health and market share, in equities in particular, is also important, as is operating leverage and credit quality.

"Stability would be a positive" for Wells Fargo, Katzke writes. Credit Suisse assumes the bank’s efficiency ratio drops to 62.5%, including above-the-norm operating losses, and expects a "far more modest loan loss reserve release" this quarter. Katzke also expects re-affirmation of expense targets (including a $53.5 billion to $54.5 billion expense target for 2018), along with updates about government investigations, litigation, and the Fed’s consent order.

Even though investors may hunger for comments about recent moves, bank leaders may not have had enough time to extrapolate yet, Mark Howard, senior multi-asset strategist at BNP Paribas, said in an interview. "A hiccup in the market is probably not going to change the outlooks," Howard says, adding that JPMorgan CEO Jamie Dimon has "seen these hiccups dozens of times. A couple of days of volatility" probably doesn’t change much.

Howard added that "letting air out of the balloon" may turn out to be good for banks, as a reset can generate activity. "A sharp 3 percent correction can be a wake-up call to action," bringing business forward as companies move more quickly with deals and in capital markets. Volatility may be lucrative for markets-oriented businesses as well.

Bank shares could use a little help these days. They peaked back in February -- lifted by tax cuts, forecasts for faster economic growth, and deregulation -- and have under-performed the broader market since May as those factors faded.

Analysts in recent weeks had hoped that banks gloomy mid-September trading updates and lighter lending expectations had set the bar low enough for a post-earnings rally.

Bernstein analyst John McDonald joined others looking for bank gains with earnings after recent underperformance. “We’re expecting solid results,” he wrote. That followed KBW saying stock prices are even lower than what tempered expectations for quarterly profits would imply, which may mean that the group is poised to rally. Earlier, Goldman said big-bank stocks were at an attractive entry point after underperforming, and as four of seven covered banks were due to beat estimates.

Investors may also have been relieved that the Democrats’ chances of capturing the Senate seem to have waned amid the controversy surrounding Supreme Court judge Brett Kavanaugh. A potential "blue wave" had spurred concerns about taxes and tighter regulation.

Others were less optimistic. On Wednesday, Portales analyst Charles Peabody cut his rating on JPMorgan to sell as the bank is likely at peak profitability, and as the stock may be overvalued, with at least 10% downside risk in the short-term. Mortgage hopes have shriveled as well, with Wedbush’s Henry Coffey noting expectations about future mortgage volumes are headed "much lower" than initially forecast by Fannie Mae, Freddie Mac, and the MBA, and will likely be flat-to-down in 2019 and 2020.

JPMORGAN ESTIMATES

- Earnings release expected Friday 6:45am New York time

- 3Q adjusted EPS est. $2.26 (range $2.18 to $2.34)

- 3Q adjusted rev. est. $27.44b (range $26.88b to $28.04b)

- 3Q total trading rev. est. $4.38b

- Equities $1.42b

- FICC $2.96b

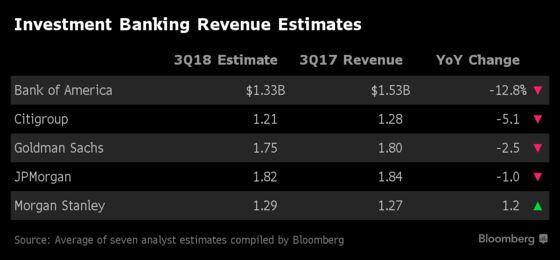

- I-banking rev. est. $1.82b

- 3Q net yield on interest-earning assets est. 2.5%

- 3Q provision for credit losses est. $1.46b

- Call 8:30am, 866-541-2724

- See Bloomberg Intelligence’s 3Q preview from October 9: JPMorgan Outlook Key Amid U.S. Strength, Global Risk

CITIGROUP

- Earnings release expected Friday at 8am

- 3Q adj. EPS est. $1.68 (range $1.61 to $1.77)

- 3Q adj. rev. est. $18.46b (range $17.96b to $18.83b)

- 3Q total trading rev. est. $3.76b

- Equities $821.6m

- FICC $2.95b

- I-banking rev. est. $1.21b

- Call 11:30am, 866-516-9582 pw 83786410

- BI 3Q preview from October 10: Citi Costs, Cards Key in Quarter, Global Risk Beyond

WELLS FARGO

- Earnings release expected Friday at 8am

- 3Q EPS est. $1.18 (range $1.12 to $1.23)

- 3Q net interest margin est. 2.94%

- 3Q net charge-offs est. $666.5m

- 3Q provision for credit losses est. $613.7m

- Call 10am, 866-872-5161

- BI 3Q preview from October 10: Wells Fargo Costs, Rate Risks Key Amid Revenue Drop

BANK OF AMERICA

- Earnings release expected Monday at 6:45am

- 3Q adj. EPS est. 62c (range 60c to 64c)

- 3Q rev. net of interest expense est. $22.63b (range $22.38b to $22.91b)

- 3Q total trading rev. est. $3.15b

- Equities $1.06b

- FICC $2.08b

- I-banking rev. est. $1.33b

- 3Q net interest yield est. 2.41%

- 3Q provision for credit losses est. $969.1m

- Call 8:30am, 877-200-4456 pw 79795

- BI 3Q preview from October 11: Loan Growth, Rate Questions Central to BofA Earnings

GOLDMAN SACHS

- Earnings release expected Tuesday at 7:30am

- 3Q adj. EPS est. $5.39 (range $4.95 to $6.23)

- 3Q net revenue est. $8.36b (range $7.73b to $8.79b)

- 3Q total trading revenue est. $3.12b

- Equities $1.73b

- FICC $1.45b

- I-banking rev. est. $1.75b

- Call 9:30am, 888-281-7154

- BI 3Q Preview from October 11: Market Moves Central to Outlook as Goldman Reports

MORGAN STANLEY

- Earnings release expected Wednesday at 7am

- 3Q EPS est. $1.01 (range 96c to $1.14)

- 3Q net rev. est. $9.56b (range $9.27b to $9.91b)

- 3Q total trading rev. est. $1.98b

- Equities $1.98b

- FICC $1.17b

- I-banking rev. est. $1.29b

- Call 8:30am, 877-895-9527 pw 6395985

Follow bank earnings calls on Bloomberg’s Top Live blogs

--With assistance from Claire Ballentine.

To contact the reporters on this story: Felice Maranz in New York at fmaranz@bloomberg.net;Kriti Gupta in New York at kgupta129@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Joanna Ossinger, Dan Reichl

©2018 Bloomberg L.P.