Beyond Meat Soars, JPMorgan Touts `Extraordinary' Potential

Beyond Meat Analysts See Big Potential, But Fret Lofty Valuation

(Bloomberg) -- Beyond Meat Inc. has massive growth potential, but this may already be reflected in a stock that has more than tripled since going public earlier this month, according to analysts who started coverage on company.

The firms were unanimously bullish on plant-based protein products, and see Beyond as occupying a central place in this rapidly growing food category. However, the stock’s performance has resulted in a valuation that is widely seen as elevated, and analysts also see potential risks from competition. While JPMorgan was emphatic in its praise -- seeing an “extraordinary” opportunity -- a more typical analysis came from Jefferies, which noted that expectations were “very high,” and said much would have to go right for shares to continue receiving support.

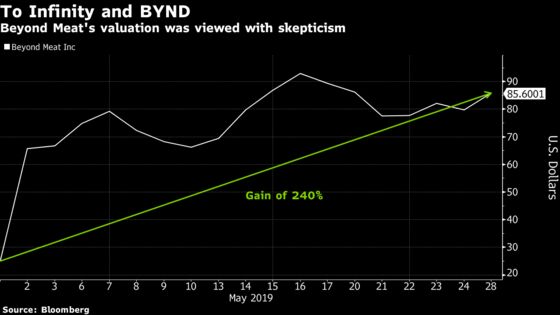

The stock has risen more than 240% since it went public earlier this month. Shares gained as much as 9.3% on Tuesday.

Here’s what analysts are saying about the company:

JPMorgan, Ken Goldman

“We view Beyond’s growth opportunity as extraordinary,” given the potential of the plant-based meat category.

The company “is a true disruptor with a differentiated product and a commitment to innovation,” and its margin upside potential is “underappreciated.”

“Strongly favorable” on the stock. Overweight rating, Street-high $97 price target.

Goldman Sachs, Adam Samuelson

The company is a “key early-mover” in its rapidly growing sector. It “is achieving notable scale on manufacturing, brand awareness, product innovation, and distribution.”

However, its sales momentum is “already more-than-fairly discounted,” and there is “considerable risk” to its longer-term ability to expand its production supply and remain differentiated from competitors.

Neutral rating, $67 price target.

BofAML, Bryan Spillane

“Optimistic about the prospects for BYND given the size of the addressable market, product quality, and positioning against consumer interests in health & wellness and sustainability.”

Hold rating, $85 target. Sees potential risks from competition and its supply chain being unable to handle rising demand. Also notes that the stock has surged since going public.

Jefferies, Kevin Grundy

The company is positioned well “for rapid and sustainable growth,” given its strong leadership and favorable trends for the plant-based protein category.

However, “expectations are very high and likely require bull case developments” for the stock to be supported. There is a “high probability” that McDonald’s will add a plant-based protein item to its menu, which would be a tailwind for the stock, though this possibility is already partially discounted.

Hold rating, $85 price target.

Credit Suisse, Robert Moskow

“Strong conviction” that the company will maintain its leadership position. However, “the stock’s valuation factors in a best-case for growth over the next six years without taking into account typical near-term execution risk for early-stage start-up companies.”

Neutral rating, $70 price target.

To contact the reporter on this story: Ryan Vlastelica in New York at rvlastelica1@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm, Jennifer Bissell-Linsk

©2019 Bloomberg L.P.