(Bloomberg Opinion) -- To Iberia, the site of Elliott Management Corp.’s latest, and suitably quixotic, activist campaign. Armed with a 3 percent interest in Portuguese utility Energias de Portugal SA, the hedge fund has written to the board to oppose the 9.1 billion euro ($10.3 billion) takeover proposal from China Three Gorges Corp. Elliott has outlined a defense strategy that would have been better coming from EDP itself, and other shareholders can be grateful.

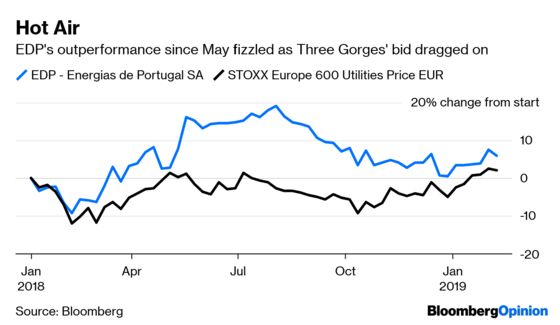

Three Gorges made an low offer in May in the hope of taking its 23 percent stake over 50 percent, saying it wanted to take control and inject some of its own assets while keeping EDP listed in Lisbon. The target rightly said the premium, just 5 percent, was too low and raised questions about how the combination would work. Since then it’s gone eerily quiet. Whether the delay is caused by slow regulators or a hesitant Three Gorges, the specter of a takeover makes it hard for life to be business as usual.

Elliott is attacking the Three Gorges offer, the standalone strategy and the capital structure – all easy targets.

The bid price is plainly cheeky. In addition, Elliott argues that staying invested under Three Gorges control would be unattractive regardless, as the Beijing-based owner would have to sell good assets to secure an array of regulatory approvals. U.S. CFIUS clearance is a particular obstacle.

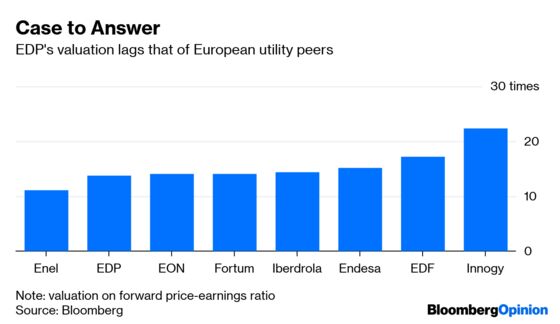

As for EDP’s existing strategy, it lacks focus. Hence EDP stock suffers a conglomerate discount. High debts constrain incremental investment in renewable power generation.

Elliott’s proposed remedy is elegantly simple: sell sub-scale or non-renewable generation assets to cut debt. Use the proceeds for further expansion in renewables, creating a more stable earnings profile. In turn, that would justify paying out a higher share of profits in dividends.

EDP could argue that it is already committed to transforming its portfolio along these lines. But the Elliott plan is clearly more energetic, and the fund isn’t alone in its thinking. Analysts at UBS set out a similar approach back in December.

Criticism of management is conspicuously absent from Elliott’s letter. Nevertheless, EDP’s unwieldy governance looks culpable for the company’s undervaluation and vulnerability to cheap bids. The board has 21 members, nine of whom have been there seven years or more. Chief Executive Officer Antonio Mexia has been there nearly 13 years. This doesn’t appear conducive to rapid change. The board now needs to explain why it isn’t already implementing Elliott’s ideas.

Elliott’s arguments sound persuasive. But the reality is that Three Gorges’s sizeable holding means China holds sway. Maybe Elliott is agitating in the hope of pressurizing Three Gorges to make a higher bid. But it would normally ask directly for that. Its best hope is that China judges that there are just too many obstacles to regulatory approval and decides to become a silent supporter of the activist assault. It’s possible – but a long shot.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.