Treasury Bears Bank on Stimulus Deal, Strengthening Recovery

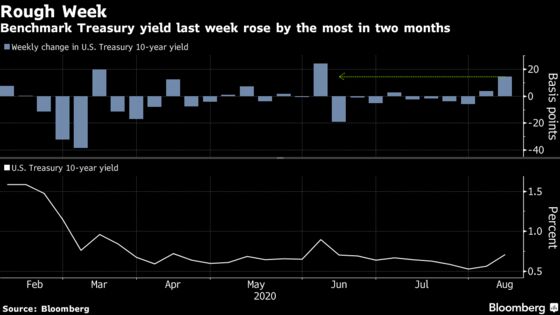

The Treasury’s $112 billion sale of notes and bonds during the week helped propel long-end bond yields to the highest levels.

(Bloomberg) -- Hefty bets against the U.S. government bond market paid off last week. Whether it’s a short-term win or the trade of the year depends on what happens next in Washington.

The Treasury’s $112 billion sale of notes and bonds during the week helped propel long-end bond yields to the highest levels in more than a month. That move benefited a recent surge of wagers on rates rising at the long end of the curve, and they may have more room to climb in the lead-up to Wednesday’s $25 billion offering of 20-year notes.

Even at the current record pace of issuance, it will take more than just supply to derail the historic bond rally that’s kept yields close to unprecedented lows. Instead, Wall Street is leaning into recent unexpected gains in U.S. economic data -- coupled with anticipation that the government can eventually pass a new stimulus spending package of more than $1 trillion -- to support growing conviction toward higher yields and a steeper curve.

“Real-time economic data in the third quarter has been pretty good, in spite of the fact that virus cases picked up since mid-June,” said Morgan Stanley’s head of U.S. rates strategy Guneet Dhingra. “This move higher in rates could have a second leg after the fiscal stimulus is announced.”

Dhingra is keeping a close eye on the Federal Reserve Bank of New York’s high-frequency growth data, and Morgan Stanley’s forecast for the next round of fiscal stimulus is on the high side among its peers at $1.5 trillion to $2 trillion.

The fate of that package still hangs in the balance, with lawmakers unable to bridge the gap between Republican proposals and Democrats’ plan, which includes aid to state governments.

The market’s apparent lack of concern over the sudden drop in fiscal support that’s taking place in the absence of fresh stimulus is curious. It’s widely recognized that the so-called V-shaped recovery apparent in some economic data, including Friday’s retail sales, has been supported in large part by the extra $600 a week that was being paid to unemployed workers while the pandemic kept businesses shuttered. A continued stalemate -- that leaves laid-off workers facing reduced support and raises the threat of evictions -- could lead to nastier data surprises and hit equities.

Calling Time

After the latest selloff, some Wall Street banks have begun to call time on bearish Treasury trades given the risks around the fiscal outlook. Goldman Sachs took profit on short positions in the 10-year bond while Citigroup closed bearish expressions that were held using options.

Some money managers are showing similar angst. Guggenheim Partners co-founder Scott Minerd told Bloomberg Television on Friday he still sees the 10-year capped at 1%, and headed to negative-0.5% over the next 18 months, since it “looks like we’ve done some real permanent damage to the economy.”

The U.S. benchmark 10-year yield ended last week at 0.71%, up from 0.56% the prior week, and was at 0.69% in New York trading Monday.

As for the Treasury’s borrowing surge, Mike Swell at Goldman Sachs Asset Management doesn’t have much faith in its power to reset the trajectory of the market.

“Ultimately, supply doesn’t drive pricing in markets,” he said in a Bloomberg TV interview, adding that the longer-term implication of a ballooning U.S. deficit is to suppress growth and inflation.

That topic -- inflation -- has become a little more pointed lately, following a sharper-than-anticipated gain in core consumer prices in July and as the Fed wraps up a review of its strategy to better meet its 2% target.

Investors may get a glimpse of the central bank’s thinking on inflation from the minutes of its last meeting, which will be released Wednesday. The Fed is widely thought to be leaning in favor of looser policy for longer to reflate the economy, and the minutes will provide clues about the central bank’s next steps at a time when the market may well be looking for even more support.

What to Watch

- Market watchers will parse the Fed minutes for some indication of progress on its strategic review, and PMIs may well dominate the data slate

- The economic calendar:

- Aug 17: Empire manufacturing gauge; NAHB housing market index; Treasury International Capital flows

- Aug 18: Building permits; housing starts

- Aug 19: MBA mortgage applications

- Aug 20: Philadelphia Fed business outlook; weekly jobless claims; Bloomberg economic expectations; Bloomberg consumer comfort index; leading index

- Aug 21: Markit U.S. PMIs; existing home sales

- The Fed calendar:

- Aug 17: Atlanta Fed’s Raphael Bostic discusses inclusive innovation

- Aug 19: FOMC minutes

- Aug 20: San Francisco Fed’s Mary Daly on the New Future of Work

- The Treasury auction calendar includes:

- Aug 17: 13-, 26-week bills

- Aug 18: 119-, 42-day cash management bills

- Aug 19: 20-year bonds

- Aug 20: 4-, 8-week bills; 30-year Treasury inflation-protected securities

©2020 Bloomberg L.P.