(Bloomberg Opinion) -- In the classic John Huston film “Treasure of the Sierra Madre,” a group of gold prospectors strike it rich before squandering their good fortune in a tangle of greed, distrust, murder and paranoia.

Something similar is happening to Barrick Gold Corp. and Newmont Mining Corp. in Nevada. Disagreements about how to manage and develop what’s arguably the world’s best-endowed area of gold deposits look set to ensure that both companies continue in an awkward and bad-tempered cohabitation, rather than growing rich together.

Every parent who’s dealt with siblings yelling “Mine!” at each other knows the way to end this sort of squabble: Take away the toys. As it happens, that might be a way to solve this fight.

The tussle has deep roots, as we’ve written. The companies have been circling each other for three decades, and the last major attempt to combine broke down in 2014. While you might have hoped that the arrival of Mark Bristow as Barrick’s chief executive officer in January would lead to a ceasefire, Monday’s round of fusillades suggests old enmities have resurfaced with a vengeance.

The problem ultimately comes down to disagreements about how to operate and develop the range of assets the two companies have in Nevada. On paper, these 12 mines should probably be combined into three or four mega-complexes. The question is how to divide the spoils.

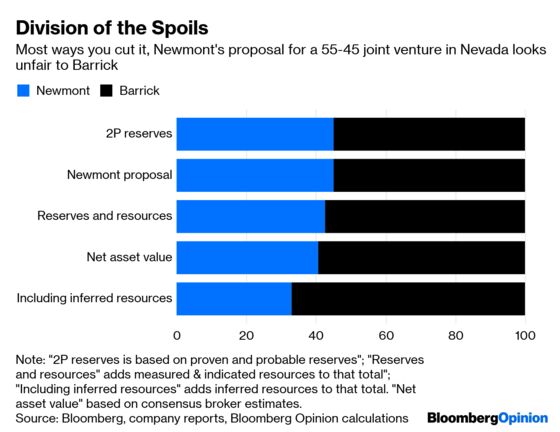

Newmont on Monday revealed a proposal to give it a 45 percent share of the assets and a 50-50 operational split. It’s not hard to see why Barrick rejected that.

The figure is a pretty accurate representation of their respective economic reserves in the state: Barrick has about 26.5 million troy ounces, while Newmont has 21.8 million, a rough 55-45 split. But Barrick has a far larger base when you factor in resources, the share of deposits that lack the cost estimation that would be needed to upgrade them to reserves:

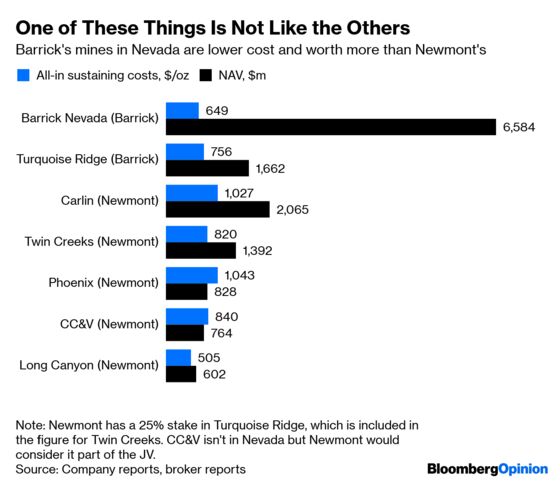

More pertinently, a strict division along mineral-reserve lines ignores the fact that Barrick’s mines are markedly lower-cost. Were gold to suddenly fall to $1,000 an ounce, the vast majority of what Newmont produces in the state would be unprofitable. In net asset value terms, a 60-40 split would be far more equitable.

Of course, arguing about which percentage each party should get is a longstanding and ultimately futile parlor game. Neither side respects the other as a mine operator, and the sorts of delays experienced at sites like Kalgoorlie in Australia – where they operate in a 50-50 joint venture – suggests that attempting to share management control rather than give it to one company is a recipe for inaction and, ultimately, value destruction.

On top of that, the deep distrust that’s been built up over the decades and the vast wealth still lying under the Nevada sand suggests this dysfunction isn’t going to go away anytime soon. Should a joint venture be spending more money developing a brownfield site like Newmont-owned Carlin, or should it focus on Barrick’s greenfield Goldrush complex to the south? That judgment call might ultimately decide which partner would make money at the expense of the other. As a result, an unproductive stalemate seems the most likely outcome.

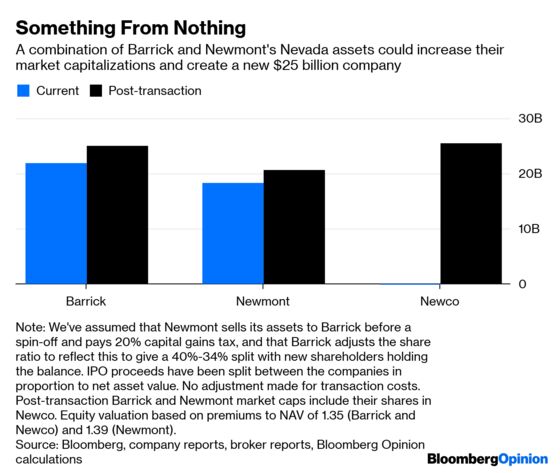

Here’s an alternative. If the problem is that neither Newmont nor Barrick trust the other to operate their Nevada assets, the answer is to ensure neither does: Combine the troublesome U.S. mines and give them a separate listing and management.

Assume the two companies were to spin off their Nevada mines, with third-party shareholders putting in an extra $5 billion via an initial public offering. Based on current consensus net asset valuations and some adjustments to equalize their differing tax liabilities, that could result in a company where Barrick had about 40 percent of the shares and Newmont 34 percent. The balance of power would rest in the hands of independent shareholders, while the cash from the share sale could go to reduce Barrick’s still-substantial debt pile and pay Newmont’s capital gains tax from the transaction.

Could such a deal work? It’s quite possible the bad blood that’s poisoned so many previous alliances would find a way of fixating on who gets which share of the equity, and the tax, and the IPO proceeds. On top of that, the ego and pride so pointedly on display in the current sniping might fuel resistance to a deal that stripped both companies of their respective crown jewels. It’s not clear, either, that investors have a lot of appetite for gold IPOs.

Still, the current situation is clearly working for no one. Should Barrick fail to disrupt Newmont’s planned marriage with Goldcorp Inc., the stalemate looks set to continue. Both companies would do well to heed the brutal lesson Humphrey Bogart learned in the Sierra Madre: By trying to get your hands on everything, you risk ending up with nothing.

We've excluded Cripple Creek & Victor, a deposit two states away in Colorado that Newmont insists should be considered part of a Nevada joint venture but doesn't intuitively seem to have much to do with the other mines.

As the smaller partner, it would make more sense for Newmont to sell its mines into the business before its formal spinoff, since an asset sale attracts a tax liability but a spinoff doesn't.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.