U.S. Banks Win $21 Billion Trump Tax Windfall Then Cut Staff, Loaned Less

U.S. Banks Win $21 Billion Trump Tax Windfall Then Cut Staff, Loaned Less

(Bloomberg) -- Major U.S. banks shaved about $21 billion from their tax bills last year -- almost double the IRS’s annual budget -- as the industry benefited more than many others from the Republican tax overhaul.

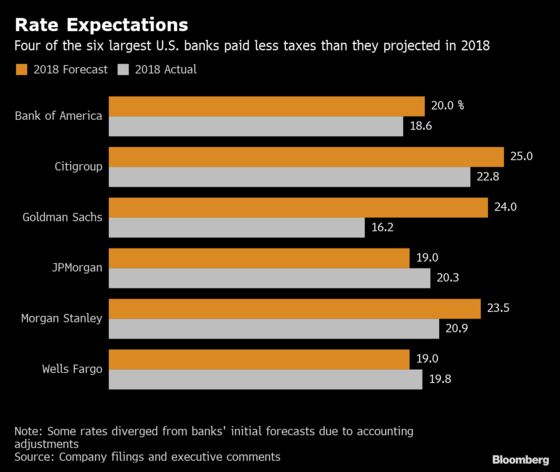

By year-end, most of the nation’s largest lenders met or exceeded their initial predictions for tax savings. On average, the banks saw their effective tax rates fall below 19 percent from the roughly 28 percent they paid in 2016. And while the breaks set off a gusher of payouts to shareholders, firms cut thousands of jobs and saw their lending growth slow.

The tally is based on a review of financial results and commentary from the 23 U.S. banks the Federal Reserve deems most important to the nation’s economy in annual stress tests. Banks stood to benefit more from lower tax rates because their effective rates were typically higher than those paid by non-financial companies. In other words, their bills had more room to fall. They’re also among the first industries to post annual results.

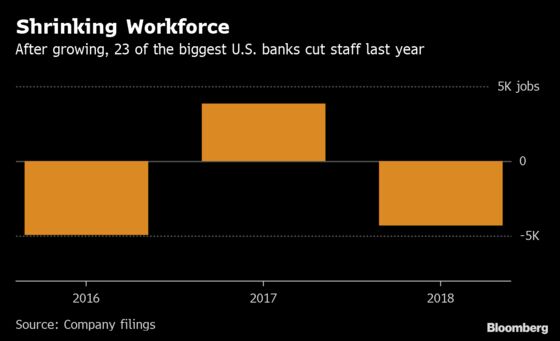

While banks vowed to use a portion of their savings to reward employees, help needy communities and support small businesses, the magnitude of their break and how the money was divvied is likely to fuel debate over whether the law was an effective way to stoke the economy. The 23 firms boosted dividends and stock buybacks 23 percent, and they eliminated almost 4,300 jobs. A few have signaled plans to cut thousands more.

The size of the tax savings is especially striking amid the heated debate in Washington over the national budget. The amount saved by banks is greater than NASA’s request for fiscal 2019, which would cover deep space exploration, orbital operations and other research. It’s more than double what the Federal Bureau of Investigation expects to spend fighting crime.

To estimate tax savings, Bloomberg applied tax rates that banks paid in 2016 to their pretax earnings last year. That’s because their rates in 2017 were skewed by billions of dollars in accounting adjustments as the new law took effect. Some banks fined-tuned the adjustments last year, potentially shifting the $21 billion figure by hundreds of millions of dollars.

Here’s a breakdown of how banks’ key constituencies fared after the tax break.

Employees

The picture is mixed for staff. As tax cuts took effect, many firms vowed to share a portion of their savings with workers. Bank of America Corp., for example, announced $1,000 bonuses for about 145,000 employees last year. Wells Fargo & Co. was among lenders that boosted their minimum wage to $15 an hour.

Yet headcount at Bank of America dropped by almost 4,900 last year, and at Wells Fargo by about 4,000. The only bank that eliminated more was Citigroup Inc., with 5,000 gone. Banks rarely provide regional breakdowns, but press reports show at least some cuts occurred outside the U.S.

The impact of those reductions on the larger group’s combined workforce was blunted as others hired.

Now, additional cuts are on the horizon: State Street Corp., which added employees last year, announced in January it will dismiss 1,500 people while automating operations. And Citigroup has indicated it may cut thousands of its technology and operations staff in the years ahead.

Tax cuts or not, the financial industry is shifting customers to mobile platforms and embracing new technologies to handle tasks. While lower taxes can ease the pressure to pare personnel costs, a number of firms have noted they’re spending more on automation.

For people who remain, lower taxes may help pad paychecks. Personnel expenses at the 23 banks climbed an average of 3.6 percent last year, a sign that employees got raises. And Bank of America expanded its bonus program this year. Still, the ratio of personnel costs to revenue declined as banks gave workers a smaller slice of the money they brought in.

Customers

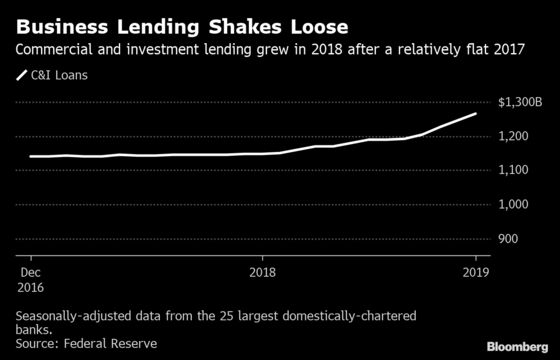

At best, corporate tax cuts had a muted impact on lending, the banks’ primary contribution to the economy. While the group of banks increased their total loan books 2.3 percent last year, that was slower than 3.6 percent a year earlier.

To be sure, lending is driven by demand from qualifying customers. Rising interest rates discouraged home sales and potentially other activities. Corporate clients also got a tax break, leaving them more money to fund expansion without borrowing.

Commercial and industrial lending -- which helps fuel job creation -- was stagnant heading into the year before picking up in the final months. That’s a sign that tax reform helped sustain economic growth, said Peter Winter, who covers regional banks for Wedbush Securities Inc. “The credit quality is still very strong for the banks,” he said.

Banks have said the tax law will help them finance worthy causes. For example, as part of a $20 billion package of initiatives, JPMorgan Chase & Co. vowed to boost small-business lending and philanthropic investments. Wells Fargo promised to give $400 million to community groups and nonprofits last year and said it will divert some future profits to philanthropy, such as support for small businesses that can’t get traditional loans.

The American Bankers Association stressed that the implications of tax reform are manifold and that it’s too early to evaluate the full stimulative effect.

“One year is simply not enough time to assess the full economic impact of major business tax reform on the banking sector, much less the entire U.S. economy,” Jeff Sigmund, a spokesman for the industry group, said in a statement. “The tax bill created positive incentives for businesses across the country to expand, but the timing and full economic impact will take many years to observe.”

Shareholders

The biggest winners were shareholders. Tax savings contributed to a banner year for banks, with the six largest surpassing $120 billion in combined profits for the first time. Dividends and stock buybacks at the 23 lenders surged by an additional $28 billion from 2017 -- even more than their tax savings.

Many banks won Fed permission in June stress tests to boost future payouts, which means investors haven’t yet received the full benefit. (Most companies disclosed how much they paid out last year, and for those that didn’t, Bloomberg calculated it based on their shares outstanding, their stated dividends, and for two banks, their commentary on buybacks.)

Still, the KBW Bank Index of the nation’s largest lenders tumbled 20 percent last year. The surge in payouts underscored that banks have limited opportunities to keep expanding their businesses profitably. So, they’re pumping out cash. The bank index has rebounded 13 percent this year, helped by the payouts and record results.

Companies “don’t go and distribute cash to their shareholders in the form of buybacks or dividends if they have good investments to make of a long-term capital nature,” said Dan Alpert, a managing partner at Westwood Capital and senior fellow in financial macroeconomics at Cornell Law School.

The debate over payouts reignited this week after U.S. Senators Bernie Sanders and Chuck Schumer wrote in a New York Times op-ed that companies should spend more money on their workforce and expansion. Wall Street leaders including JPMorgan Chief Executive Officer Jamie Dimon have said shareholders steer the cash to other ventures that can use it better.

By midweek, former Goldman Sachs Group Inc. CEO Lloyd Blankfein was arguing with Sanders on Twitter.

“The money doesn’t vanish,” Blankfein wrote. “It gets reinvested in higher growth businesses that boost the economy and jobs. Is that bad?”

To contact the reporter on this story: Ben Foldy in New York at bfoldy@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, David Scheer, Dan Reichl

©2019 Bloomberg L.P.