Banks Need Conviction If We Are Going Anywhere: Taking Stock

Banks Need Conviction If We Are Going Anywhere: Taking Stock

(Bloomberg) -- We’re middling around flat (this feels familiar) following the surge Friday, and this holiday-shortened week is not likely to help conviction in the S&P.

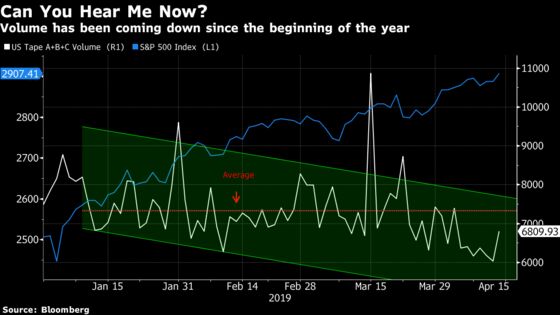

It’s hard for the bulls to be critical this early in the second quarter, as there’s been just one down day thus far in more than two weeks, but within that time span it’s not like the interest and support from a volumes perspective was there.

The trend has been decidedly lower, and even with the major sentiment boost that came Friday, volumes failed to reach their average on the year. Maybe it’s partially attributed to Spring Break season for portfolio manager’s families and the upcoming Easter breaks, or new capital is just not willing to be put to work here when we’re about a 1% from all-time highs.

The narrative will need to change for investors to re-rate equities beyond current valuations, and earnings will need to deliver. Futures are unchanged despite encouraging data from Asia overnight, a sign we’re in wait-and-see mode. The two biggest names on the docket today could be just the ticket, as their "drought" of earnings misses, though not as dramatic as Tiger Woods’ time between major tournament wins, still bodes well. Goldman Sachs has missed on EPS expectations just twice in the past 29 quarters, while Citi has gone 20 straight quarters without a miss, according to data compiled by Bloomberg.

Pick a Card, Any Card

The card deck has been shuffled in S&P, as the second-worst-performing segment in the first quarter, financials, has put on a showing in the first two weeks of this quarter. It now leads most groups, up nearly 5.5% ahead of the majority of banking earnings season which continues today with Goldman Sachs and Citi shortly. An otherwise good start to the season with JPMorgan was soured as Wells Fargo threw a wrench into the mix with its net interest income forecasts (WFC is getting a cascade of ratings downgrades this morning, for what its worth). Even with the outperformance recent weeks, the sector still rates attractive on many criteria.

Bloomberg Intelligence’s Chief Equity Strategist, Gina Martin Adams, last week wrote as much, noting by "most measures," the sector was among the deepest discounts in the benchmark. But despite this fact, she writes that “until a catalyst” emerges to drive better growth, the sector may remain “unloved.” So despite the trading environment that JPMorgan saw as less bad than it previously expected, growth will be a factor. Strongest income growth is expected from SVB Financial, People’s United Financial and Assurant, with the weakest from Goldman Sachs, Franklin Resources and CBOE Global Markets, according to data compiled by Bloomberg Intelligence.

Your 63-Hour ICYMI

ECB President Draghi alluded to concerns about the U.S. Fed’s independence; Kevin Durant and Patrick Beverley were ejected in Game 1 of their playoff series; Barron’s profiled Brown Advisory Sustainable Growth Fund managers who demonstrated they could beat benchmarks using ESG (and favored BLL, DHR rather than names like FB); more airlines cancelled flights due to the Boeing 737 Max grounding and weather-related issues related to the Midwest storms; Orioles star Chris Davis broke his record hitless streak (was 0-33) with a three-hit game; Writer’s Guild of America has begun firing agents in a fee dispute; Alcon, HBAN, KEY, VLO and KSS were all mentioned positively in Barron’s; Trump alleged that the market would be 5,000 to 10,000 points higher if the “Fed had done its job properly”; an economist in Turkey was detained was detailed by Istanbul police after allegedly insulting President Erdogan; Bryson DeChambeau, after narrowly missing a hole in one earlier in the Masters Tournament and admitting to have never achieved the feat in his career, hit a hole in one in the final round of the golf major ultimately won by Tiger Woods -- breaking the latter’s more than 10-year drought without a major win.

Sectors in Focus Today

- Large banking names as key reports await after Wells Fargo and JPMorgan came Friday, with others due shortly (C, GS; MS later this week)

- Electric vehicle makers (TSLA, NIO) after Volkswagen unveiled its EV SUV concept

- Video game makers (ATVI, EA) as Apple spends hundreds of millions on an Arcade Game Service, according to the FT

- Waste services names (RSG, WCN, BIN CN) after Waste Management confirmed it was to buy Advanced Disposal for $33.15/share in cash

- Advertisers (OMC, IPG) after Publicis’ deal for Alliance Data’s Epsilon unit

- Miners and some shippers (CLF, LIF CN, EGLE, CMC) as the iron ore shortage boosts prices

- E&P’s and integrated oil names after CVX’s deal for APC on Friday lifted E&P names. Watch for elevated volatility

Notes From the Sell Side

The quiet period for jeans-maker Levi Strauss is over today, and the Street thus far is generally bullish, with 4 ratings at the equivalent of a buy, and two at neutral. Of the buy ratings, Dana Telsey of the Telsey group has the Street-high price target at $28, writing that the company has a "proven track record" of growth in the past 7 years, while owning the "highest brand awareness" in denim bottoms. She sees the company set up for future profitable growth with an increasingly diversified business model. Neutral-rated Morgan Stanley analysts led by Kimberly Greenberger are generally supportive of the company, but express caution given the current market valuation. They expect gross margins to continue to expand and are "constructive" on the name, but highlight the “market appears equally enthusiastic.”

Chemicals names were broadly raised at Nomura, with DOW, EMN, HUN, LYB all receiving new buy ratings (upgraded from neutral) from analysts led by Aleksey Yefremov. Two other names, WLK and OLN, were raised to neutral from reduce. The thesis mostly revolves around the expectation that commodity cash margins will improve "modestly" and return to historical averages and that China macro data and commodity trends are supportive of the segment. Valuations, the analysts write, were also below their cycle averages from the EV/EBITDA perspective.

Tick-By-Tick to Today’s Actionable Events

- LEVI quiet period expires

- U.S. and Japan hold first round of trade talks

- CFTC’s Global Markets Advisory Cmte meets in D.C.; topics to include trading on electronic trading platforms

- 7:30am -- Goldman earnings

- 8:00am -- Citigroup earnings

- 8:30am -- April Empire Manufacturing

- 9:00am -- GS earnings call

- 9:30am -- SEC’s Fixed Income Market Structure Advisory Committee Meeting

- 10:00am -- C earnings call

- 1:00pm -- Fed’s Evans on economy and monetary policy

- 4:00pm -- Feb. Net Long-Term TIC Flows; Total Net TIC Flows

- After the close -- Rio Tinto results

- 8:00pm -- Fed’s Rosengren speaks at Davidson College in North Carolina

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.