Banks’ Last Hurrah From Fed Likely Means 2019 Has Already Peaked

Banks’ Last Hurrah From Fed Likely Means 2019 Has Already Peaked

(Bloomberg) -- The first quarter may be as good as it gets for banks in 2019, almost four years and nine rate hikes into the Federal Reserve’s tightening cycle.

Results for the period are probably the last for now to get a boost from monetary policy, after Fed Chairman Jerome Powell said benign inflation data mean interest rates could be on hold for “some time.”

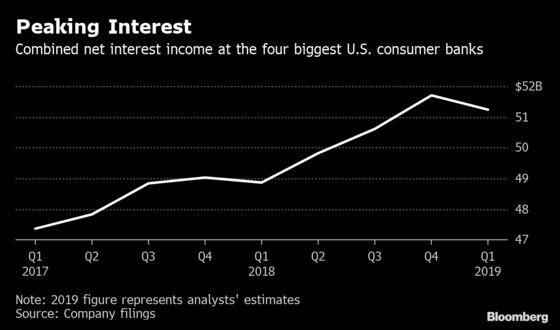

For banks, that means net interest income -- the money lenders make from customers’ loan payments minus what they pay depositors -- could stop climbing as well. NII has been a key driver for revenue in recent quarters. The figure jumped 10 percent to a record $14.4 billion at JPMorgan Chase & Co. in the fourth quarter, though the company has warned it expects little change for the first quarter.

“I think you’re looking at peak year-over-year momentum here in the first quarter,” Charles Peabody, an analyst at Portales Partners, said in an interview. “This is the last quarter that benefits from the rate rise.”

JPMorgan and Wells Fargo & Co. will give investors their first look at how Fed policy affected the nation’s biggest banks at the start of the year. They release first-quarter results on Friday followed by the rest of the biggest U.S. banks next week. The last hurrah for rising rates could help counter an expected drop in trading revenue that analysts are predicting, along with weaker investment-banking results.

Bank shares fell in March when the Fed’s intentions became clearer. Still, for the year, the KBW Bank Index has climbed 14 percent, compared with about 16 percent for the broader S&P 500 Index.

Here’s what to watch for as earnings season gets under way:

Trading Revenue

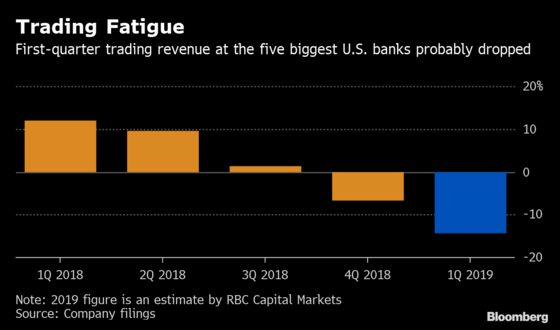

Fresh off December’s extreme market volatility, investors were greeted with a 35-day U.S. government shutdown. The combination made the first quarter a “sluggish environment for trading and investment banking,” James Mitchell, an analyst at Buckingham Research Group, said in a note last week. Revenue from trading at the biggest banks is projected to be down 14 percent, according to Gerard Cassidy, an analyst at RBC Capital Markets.

Executives including JPMorgan Co-President Daniel Pinto and Morgan Stanley Chief Financial Officer Jonathan Pruzan have already warned investors that this year is getting off to a slower start.

“Our forecast for the full first quarter on a reported basis will be down on the high-teens,” Pinto said at the bank’s investor day in February, citing “a very tough comparison” to the year-earlier quarter in the currency and emerging-markets businesses. “We had a slow start in the equities business, and overall, we see lower, weaker client activity.”

On the bright side, Buckingham’s Mitchell said he’s expecting positive comments from bank executives about underwriting pipelines. Jefferies Financial Group Inc., which reported results for its fiscal first quarter in March, said investment-banking activity had rebounded last month.

Loan Growth

Commercial and industrial lending “has again led the charge for the larger banks,” David Long, an analyst at Raymond James & Associates Inc., wrote in a note last week. Analysts are expecting strength across the industry, with business loans growing about 10 percent, according to Atlantic Equities analyst John Heagerty.

On the consumer side, mortgage rates fell in the first quarter, offering a reprieve for home lenders who have been burdened by the end of the refinancing boom and heightened competition from non-banks. Wells Fargo Chief Financial Officer John Shrewsberry said in February that competition is starting to ease in the business with the exit of some mortgage originators.

“There has been a notable uptick in mortgage refinancing since the start of 2019,” Heagerty at Atlantic Equities wrote in a note to clients last month. “Consumer loan growth appears to have rebounded.”

Risks

This quarter will be “less about the results than about the revenue outlook,” Saul Martinez, an analyst at UBS Group AG, wrote in a note to clients.

To contact the reporter on this story: Hannah Levitt in New York at hlevitt@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Steve Dickson, Daniel Taub

©2019 Bloomberg L.P.