Banks Head Into Darkest Phase of Nordic Negative-Rate Cycle

Banks Head Into Darkest Phase of the Nordic Negative-Rate Cycle

(Bloomberg) --

If you want to know what long-term negative interest rates are doing to banks, watch Denmark in the coming months.

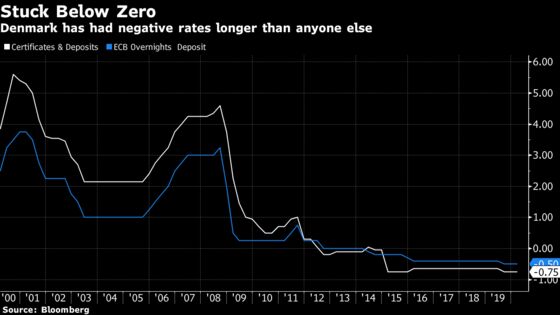

Danes have lived with subzero rates longer than anyone else, after the central bank resorted to the policy in 2012 to defend its currency peg. But according to the country’s financial watchdog, it’s only now that the real cost of the regime will make itself felt.

In fact, the Danish Financial Supervisory Authority says the worst is yet to come.

Kristian Vie Madsen, deputy director general at the FSA in Copenhagen, says, “Now is the time that you, to a larger extent, will be able to see the problem in the profits of the banks.”

Negative rates have made a mockery of some of the basic tenets of banking, namely: holding deposits and lending money at a profit. Across Europe, lenders are stepping up calls for an end to a regime that was originally intended as a short-term fix to an economic crisis. Some, such as Deutsche Bank AG CEO Christian Sewing, are worried Europe has “missed the exit.”

In Denmark, banks have so far relied on “a lot of one-offs” to offset losses, Madsen says. He points to historically low loan impairments, high bond-portfolio valuations and record rates of mortgage refinancing.

But those effects are petering out, Madsen said in an interview. “There are not that many one-offs that can save the results for the next year,” he said.

The FSA is speaking out as Danish banks prepare to report their annual results, which may be the last time they benefit from the one-offs Madsen lists. Danske Bank A/S, the country’s biggest financial group, will release its numbers on Feb. 5.

Emergency Rates

An extreme policy used to fight sudden pressure on the Danish krone has now shaped a whole decade, with most economists predicting years more of the regime in Denmark.

The bankers’ association says negative rates pose a serious threat. It estimates that life below zero cost the industry around 2.5 billion kroner ($371 million) last year alone; if rates were positive, banks would probably have made around 3 billion kroner. (Negative rates also add to banks’ cost of holding bonds in order to meet liquidity requirements.)

Meanwhile, the monetary policy is giving deposits -- once a coveted form of stable funding -- a bad name. Danish banks have started imposing fees on retail clients with large deposits, in an effort to get rid of surpluses.

Lars Rohde, the governor of the Danish central bank, has suggested that banks have little to complain about. He says the industry is chasing unnecessarily high returns on equity, and notes that investors should be happy with less, given how well capitalized (i.e. safe) banks now are.

Still, the central bank last month suggested that some banks should have more capital, after stress tests showed shortcomings.

Read More: Arrival of ECB Tiering Hands Banks Only Limited Rate Pain Relief

Madsen says the FSA is now on the lookout for banks that try to cope with the tougher climate by overselling their loans.

Banks “should be careful” about padding profits by “increasing your top line by selling a lot more,” he said. “If the demand isn’t there for credit, you’ll just compete very hard for the few customers there are, and maybe take on some customers with too high risk.”

He also says the industry needs to be more disciplined in dealing with costs. “There is an issue,” he said. “And you have to handle it and you cannot handle it with growth.”

“In a stress test, there are two things that can take the losses: one is your earnings and the other is your capital level,” Madsen said. “When earnings are low, then capital will have to handle losses. Banks would have to have a higher capital level to get you securely through a stress test.”

So far, the challenges facing banks haven’t given rise to broader concerns about the stability of Denmark’s financial system. For now, that worry is more focused on the risk of inflated asset prices, Madsen said.

“If the search for yield is going too far....you would see high asset prices, and if the banks then borrow against the asset prices more than making sure that their customers are able to pay back the loans, then it’s becoming risky,” he said.

To contact the reporter on this story: Frances Schwartzkopff in Copenhagen at fschwartzko1@bloomberg.net

To contact the editors responsible for this story: Tasneem Hanfi Brögger at tbrogger@bloomberg.net;Christian Wienberg at cwienberg@bloomberg.net

©2020 Bloomberg L.P.