Banks Fire Up Their Mortgage Machine for a Refinancing Boom

Banks Fire Up Their Mortgage Machine for a New Refinancing Boom

(Bloomberg) -- Lenders thought it was time to shrink their mortgage businesses. Now they’re finding they were wrong.

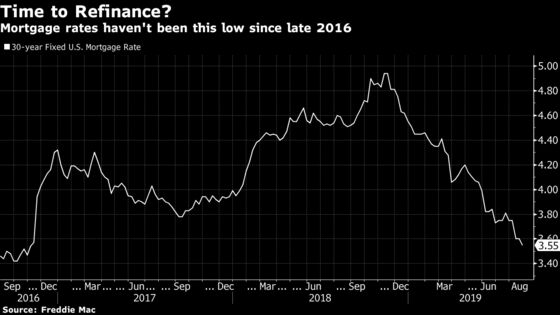

With rates for home loans sinking to their lowest levels since late 2016, Wells Fargo & Co., the biggest mortgage lender in the U.S., has boosted staffing for the business by about 10% this year and plans to keep hiring. Bank of America Corp. is hiring in areas including sales, processing, and underwriting.

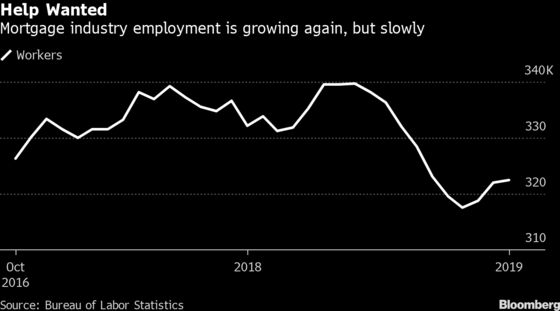

The mortgage industry has added almost 5,000 employees since March, a 1.5% gain, according to the Bureau of Labor Statistics. It’s a stark reversal from a year ago, when the Federal Reserve was hiking interest rates and banks were cutting thousands of jobs.

Employment in the mortgage lending business has been shrinking for more than a decade, thanks first to the housing crunch and then to rising rates. In 2006, there were more than half a million workers in mortgages, compared with about 323,000 in June.

Now demand for the loans is rising high enough and fast enough that lenders seem to be doing something. The volume of applications for refinancing mortgages has more than tripled since December, according to a barometer from the Mortgage Bankers Association.

“It does put stress on the entire industry, whether it’s the appraisers, title companies, mortgage companies,” said John Schleck, head of centralized and online consumer lending at Bank of America. The bank is taking about 60 days to process applications, up a little more than a week, as it tries to keep up with the rising volume, according to bank spokeswoman Kris Yamamoto.

On Thursday, data from the National Association of Realtors showed contract signings to purchase previously owned U.S. homes fell in July by the most since early 2018, indicating a pause in buyer interest. The index of pending home sales decreased 2.5% from the previous month. The median forecast in Bloomberg’s survey called for no change.

Indeed, lenders are adding staff slowly, to avoid having to rapidly lay people off if the market turns, and they’re investing in systems to make their employees more productive. Quicken Loans, the nation’s biggest nonbank home lender, has been focusing on investing in technology and related jobs all year, according to Chief Executive Officer Jay Farner. He said in an interview that he’s seen heightened competition in hiring lenders and underwriters in recent months, but that Quicken’s hiring plans haven’t changed this year despite lower rates.

“It’s real tough on your business to always be hiring and removing,” Farner said. “We’ve been on this hiring climb to continue to build out the technology that our clients are looking for.”

High Profitability

If banks and finance companies were hiring more, mortgage rates would likely be lower: The gap between how much lenders charge for the loans and how much they pay to borrow money to fund mortgages, a measure of profitability known as the “primary/secondary spread,” is at the highest level since mid-2012.

That suggests lenders have ample room to cut rates and win more business, if they had more people to process applications. Banks in particular are reluctant to grow too fast, fearing a business that spurred the last downturn and can be highly cyclical.

Last year, finance companies outside the banking system accounted for about 60% of the most common types of mortgages, those sold to government-backed buyers like Fannie Mae and Freddie Mac, according to Inside Mortgage Finance. That’s up from 47% in 2014.

Alex Echeandia, a broker at Eagle Creek Mortgage in Gaithersburg, Maryland, said he works with more than 30 lenders when considering mortgages for his clients. But the biggest banks aren’t among them, in part because they may only offer a few types of loans and move slower than smaller lenders.

“All of our lenders are mortgage lenders -- they’re not brick and mortar banks,” Echeandia said. “I like the flexibility. We’re able to shop it around and talk to different lenders to get our clients the best.”

At Wells Fargo, refinancings are taking about 10 days longer than they did a year ago, even with more staff on board. Jerald Banwart, the bank’s head of retail fulfillment, said in an interview that Wells Fargo plans to keep increasing headcount in mortgage processing, underwriting and closing by around an additional 5%.

Even though the labor market is tighter than in previous refinancing rallies, “the industry has been downsizing in the past couple years, so there’s definitely talent out there,” Banwart said.

--With assistance from Vince Golle.

To contact the reporters on this story: Hannah Levitt in New York at hlevitt@bloomberg.net;Claire Boston in New York at cboston6@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins, Steve Dickson

©2019 Bloomberg L.P.