Banks See Consumer Loan Costs Drop Despite Rising Rates

Banks See Consumer Loan Costs Drop Despite Rising Rates

(Bloomberg) -- When interest rates tick higher, consumers carrying too much debt start to default. It’s the natural assumption, but Americans keep meeting their obligations.

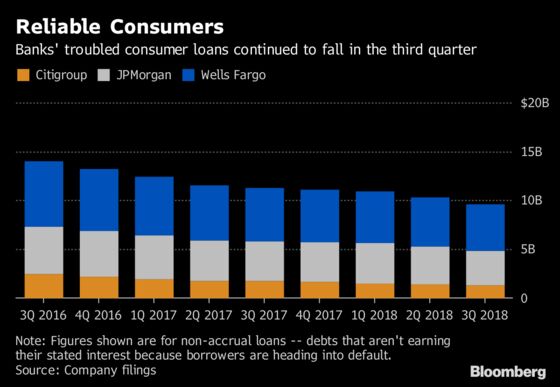

Three of the largest U.S. banks -- JPMorgan Chase & Co., Wells Fargo & Co. and Citigroup Inc. -- announced Friday that their costs for bad loans are falling. The same strong economy pushing the Federal Reserve to raise rates is helping households keep current on their growing mound of debt.

JPMorgan’s provision for bad loans was half-a-billion dollars less than analysts estimated as one measure of trouble in its consumer portfolio fell to the lowest level in more than a decade. Wells Fargo and Citigroup both cut the amounts they set aside for consumer loan losses by at least 13 percent.

“Most of the consumer credit written since the great recession has been pretty damn good, and our book is extremely good,” JPMorgan Chief Executive Officer Jamie Dimon told journalists on a conference call. “Of course, one day there’ll be a cycle, one day credit losses will be going up.”

A year ago, many observers thought the tide already was turning as four of the largest consumer lenders boosted provisions. Analysts and investors worried that mom and pop would struggle to keep up with bills accruing higher interest, or that they would default on car loans as resale values slumped. But restraint in lending, improvement in the labor market and tax cuts held those scenarios at bay.

“It’s a combination of people being more disciplined and banks better managing their balance sheets,” said Mark Doctoroff, co-head of Mitsubishi UFJ Financial Group Inc.’s financial institutions group. “It’s much harder now to get a consumer loan.”

The boon in credit quality is perhaps the most direct way banks are benefiting from the latest stages of the economic recovery. Industrywide loan growth hasn’t been as strong as expected in the wake of corporate tax cuts, and higher interest rates have been a mixed bag as a flattening yield curve -- narrowing the difference between short- and long-term interest rates -- limited the boost to margins.

Some analysts still see credit costs creeping up next year. Goldman Sachs Group Inc., which jumped into the consumer space with online personal loans, recently tapped the brakes on that fast-growing business on concern that delinquencies would rise.

Cracks in Card

And to be sure, banks said that within retail businesses, they’re bracing for more defaults on credit cards.

JPMorgan’s allowance for consumer loan losses, meant to cover write-offs over coming quarters, dropped to $9.1 billion, less than half what it was six years ago. Within that, the bank increased the amount set aside for credit cards to $5.03 billion, the highest since 2012.

Citigroup’s net credit losses in its branded card business increased 5 percent to $644 million, or 2.9 percent of the portfolio. The bank has warned that metric could climb to 3.25 percent over the medium-term as new customers begin to default. Still, it’s a far cry from 2009, when the company wrote off more than 10 percent of its portfolio.

Shares of Visa Inc. and Mastercard Inc., which both collect fees for handling transactions, were up more than 3 percent as of 12:40 p.m. in New York. Analysts pointed to spending levels, with KBW’s Sanjay Sakhrani telling clients in a note that volume trends from the three banks were in-line to better than expected for the card networks.

Holiday Season

The question now is whether Americans will keep shopping responsibly and paying their bills.

“The consumer has to be watched, but I think we are going to go into a very good retail season in the holidays,” with banks benefiting, Doctoroff said. “Hopefully this will correct some about the consumer being stressed.”

--With assistance from Hannah Levitt.

To contact the reporters on this story: Jenny Surane in New York at jsurane4@bloomberg.net;Claire Ballentine in New York at cballentine@bloomberg.net;Michelle F. Davis in New York at mdavis194@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, David Scheer, Dan Reichl

©2018 Bloomberg L.P.