Decades of Betting on Commercial Real Estate Made U.K. Banks Nothing

Decades of Betting on Commercial Real Estate Made U.K. Banks Nothing

(Bloomberg) -- For at least half a century, banks in the U.K. bet on offices, stores and warehouses -- and lost money.

The losses suffered on loans when the commercial real-estate market turns sour have, time and again, dwarfed profits made earlier in the cycle, according to a report analyzing data from the Bank of England and academics. The authors say they’re sounding the alarm to improve lending standards in an industry that almost brought Britain’s financial system crashing down a decade ago.

The problem, the report says, is that bankers tend to follow the herd and plow money into commercial property just as markets peak. While lenders today have learned some lessons from the 2008 crash, they can do more, for example by using valuations based on long-term averages, spending more time assessing macro-economic risks and finding ways to manage the peer pressure caused by rivals continuing to advance loans, the report says.

“Although the lending market is in better shape now, most lenders still haven’t got an end-of-cycle strategy,” Rupert Clarke, a market veteran who wrote the Property Industry Alliance report, said in an interview. Without it, “you are going to have the same problems again.”

It’s a decade ago this month that the government stepped in to rescue some of the U.K.’s biggest banks, which were teetering due in large part to bad real estate loans. Commercial property values fell more than 40 percent from their 2007 highs, prompting a wave of defaults by debt-fueled investors which had often borrowed as much as four-fifths of a building’s purchase price.

The report shows how lending volumes increased massively in the final stages of the last three U.K. real estate cycles, just as prices mounted. In the long bull run before the global financial crisis, U.K. commercial property lenders made about 7 billion pounds ($9.1 billion) in profits, but were forced to write off about 19.3 billion pounds in the collapse that followed.

‘Irrational Exuberance’

About 165 billion pounds of new commercial real estate loans were issued in 2006 and 2007, just as values climbed toward their high point. That’s more than five times the size of the entire outstanding loan book at the trough of the cycle, illustrating how years of profitable lending can be undone by “irrational exuberance,” the report said. In the three years leading up to the crash of 1974, loan advances increased by 92 percent a year, the study found.

“Commercial real estate lending has been central to almost all the financial crises of the last half-century,” Adair Turner, a U.K. peer and think-tank chairman who led the now-abolished Financial Services Authority, said by email. The report shows “the huge financial impact of irrationally exuberant late-cycle lending, which destroys value in the industry and in the wider economy.”

The “profitability black hole” of commercial real estate lending in Britain probably happened in other countries as well, the authors said. The report uses data from the BOE and from surveys of real estate lenders by De Montfort University and Cass Business School.

Ten years on from the global crisis, there’s been some improvement in lending standards, but there are still dangers to be avoided.

Regulation has limited banks’ capacity for commercial real estate lending and helped to bring loan-to-value exposures down to below 60 percent on average, the report said. Yet valuations are well above historical trends, with yields on prime properties much lower, leaving them exposed to an interest-rate rise or a failure of confidence, possibly due to Brexit, Clarke wrote.

Credit providers have stopped expanding their commercial property loan books, but lenders are taking additional risk by advancing more credit for development, according to the Cass U.K. Commercial Lending Report, published in April.

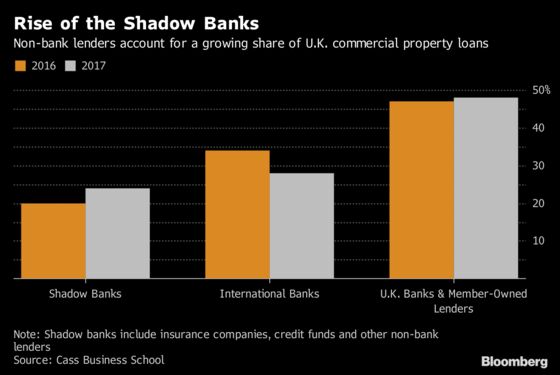

The increasing role of less-regulated non-bank lenders is also a danger, Clarke argues. And banks have failed to come up with ways to deal with the cyclical nature of real estate, which heightens the risk of bankers lending more when prices are near historic highs, he said.

The situation is better than in 2008, Clarke wrote, “however, memories fade, and when they do, history tends to repeat itself.”

--With assistance from Neil Callanan.

To contact the reporter on this story: Jack Sidders in London at jsidders@bloomberg.net

To contact the editors responsible for this story: Sree Vidya Bhaktavatsalam at sbhaktavatsa@bloomberg.net, Paul Armstrong, Elisa Martinuzzi

©2018 Bloomberg L.P.