Europe’s Weakened Banks See a Road Around New Capital Rules

Europe’s Weakened Banks See a Road Around New Capital Rules

(Bloomberg) --

European banks have found a silver lining to their recent troubles: they can make a case that they’re too weak to abide by new regulations being set by Brussels.

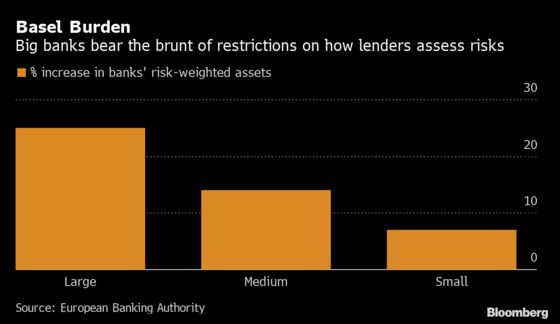

After years fighting a rearguard battle against tighter requirements set by global regulators, some bankers in Europe now say they sense an opportunity to persuade local policy makers to go easier on them. Banks would need about 135 billion euros ($149 billion) to comply with the standards as first drafted by the Basel Committee on Banking Supervision, according to an estimate this year by European Union regulators.

James von Moltke, Deutsche Bank AG’s chief financial officer, told analysts recently that he sensed a “shift in tone” among politicians and is optimistic that the final rules could be “less onerous” for the industry once they’re put on the books in Europe. That is particularly important for Deutsche Bank, which Citigroup Inc. analysts have said faces the prospect of raising more capital to meet the standards.

“It is simply bad medicine considering the current signs of economic slowdown in Europe,” Ulrik Nodgaard, chief executive of banking association Finance Denmark, said in an email.

Withstanding Earthquakes

The European Commission, the EU’s executive arm in Brussels, is holding a conference on Tuesday on the latest standards, which were agreed to by the Basel Committee in December 2017. The rules must be enacted into local law by the EU and individual countries around the world, giving politicians the opportunity to shift course. The standards determine how banks calculate the risk of mortgages, corporate loans and other assets and, as a result, the capital they need to cover the risk.

The Commission could propose legislation to implement the Basel rules in the second quarter of next year, Valdis Dombrovskis, the EU commissioner in charge of financial services, said in remarks prepared for the conference.

“There will clearly be a focus on European specificities, where increases in capital requirements might have a disproportionately negative impact on some specific sectors, business models or activities,” Dombrovskis said.

But banks shouldn’t necessarily get their way, according to Andrea Enria, chair of the supervisory board at the European Central Bank, who called on lawmakers to implement Basel faithfully.

“European legislators must stand up to national interests and the lobbying of some banks,” he said in his conference speech. “When you are building something that is supposed to withstand earthquakes, you should not opt for cheaper materials in the final stages of your construction work just because your budget is getting tighter.”

Firms including Banco Santander SA, Deutsche Bank and Intesa Sanpaolo SpA are slated to attend Tuesday’s conference, where one of the panels is titled “Basel III: Are we done now?” Here are four of the key battlegrounds that the EU still faces before the rules are put in place.

Model Limit

A major gripe of European banks is the so-called output floor, which limits how much banks can reduce their capital needs by using internal risk models instead of the standard formulas devised by regulators.

Major international banks say this restriction should apply only to their company in its entirety, rather than to each subsidiary, allowing them to deploy resources more flexibly across their operations. The European Banking Authority, the bloc’s main regulator, has said such an approach would be inconsistent with how capital requirements currently work in the EU. However, the Commission hasn’t rejected the idea outright and is seeking more information on the issue.

Minimum Application

Capital requirements in the EU come in two parts: a legal minimum level for all banks and add-ons that supervisors can set for particular banks. Lenders want the curbs on risk models to apply only to the first part to avoid being penalized too much by supervisors, the European Banking Federation has said.

The EBA has dismissed this idea, recommending the new framework applies to “all the capital layers,” as this would make the output floor “most straightforward to calculate and disclose.” Impact assessments have shown that applying the new standards in this way would be more expensive for banks.

Corporate Lending

Businesses rely heavily on bank loans for financing in Europe, since the capital markets for issuing debt are less developed than in the U.S. Banks argue the Basel standards penalize business loans by considering them risky, particularly when the borrower has not obtained a credit rating from one of the major agencies. However, European regulators are resisting their calls to water down the rules.

Real Estate

Banks want more flexibility under the rules in how they can assess the riskiness of mortgage borrowers as well as the amount of capital they need to guard against defaults. Denmark, Sweden and Finland have argued for years that their mortgages are lower risk than those in other countries, such as Italy and the U.S., and that the rules would unnecessarily hit lenders in their home markets.

The European Banking Federation, which represents national industry lobbies from across the bloc, wants lawmakers to allow for lower risk weights for mortgages. European regulators say that would undermine the credibility of the EU banking sector. The EBA says that the standards already allow for key EU mortgage-lending practices.

--With assistance from Nicholas Comfort.

To contact the reporters on this story: Silla Brush in London at sbrush@bloomberg.net;Alexander Weber in Brussels at aweber45@bloomberg.net

To contact the editors responsible for this story: Ambereen Choudhury at achoudhury@bloomberg.net, Marion Dakers, Keith Campbell

©2019 Bloomberg L.P.