Bankers Get Creative to Offload CLO Risk in U.S. and Europe

Bankers Get Creative to Offload CLO Risk in U.S. and Europe

(Bloomberg) -- Arrangers of collateralized loan obligations are innovating their way through a tough market as they try to shift a stockpile of warehoused assets from their balance sheets.

The year’s first batch of new CLO issues to price in the U.S. includes two transactions with short maturities and one static deal, where the underlying pool of loans remains the same throughout its lifetime. These non-typical features are offered to draw in investors some of who have grown more cautious after leveraged-loan prices dropped and CLO funding costs rose at the end of last year.

Investors say similar structures are being touted in Europe as well. And it’s not the first time that more creative structures have appeared: short-dated deals emerged in 2015 and 2016 when market conditions deteriorated during the oil and gas crisis and liability spreads ballooned.

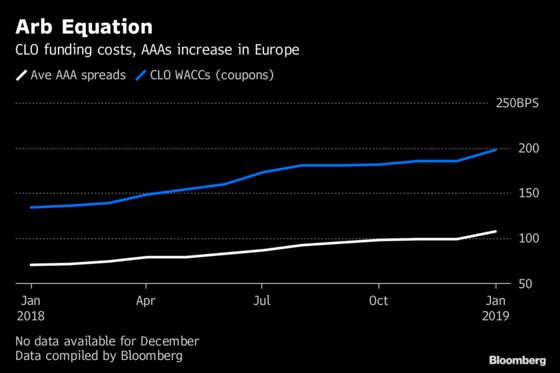

Issuance of CLOs -- bonds whose cashflows are provided by an underlying pool of loans -- soared last year as investors wanted exposure to higher-yielding, floating-rate debt. The market stalled toward year end amid the broader market volatility and weaker sentiment. CLO managers are now trying to navigate the slow recovery in the market.

Credit cycle

This year’s crop of deals may be driven by several motivations. In some cases a manager may be trying to time the maturing credit cycle leaving the door open for a refinancing in a year’s time and before defaults start to rise.

For others, the shorter maturity may be the final lifeline to converting an older warehouse into a CLO. That could help them avoid the worst-case scenario of having to liquidate the structure, while allowing the arranger to unclog some of these older facilities from its balance sheet and move ahead with its pipeline of new deals.

The U.S. is more advanced in its credit cycle than Europe, and some managers and investors there are keen to build in the option to refinance a deal before the cycle turns and defaults pick up.

The logic behind short-dated deals is that they will be able to refinance in one year’s time, according to a U.S.-based equity investor. Any investor opting for a deal with a one year call period must believe there’ll be positive market conditions in 12 months’ time, but beyond that point it’s looking less certain and they don’t want to risk the two year call, he said.

All Pockets

In their efforts to get deals away, arrangers are exploring all potential pockets of cash, and these more innovative deals can open up different sources of liquidity for the debt tranches.

There’s a larger universe of AAA-rated investors with an appetite for shorter duration, said the U.S. manager. That may have to do with their view of the credit cycle, or it may just be that the liabilities they are using to fund their investment are shorter and they are just matching that duration, he added.

A let up in the volume of CLO refinancings reaching the market might bolster demand for shorter dated new issue paper given there is a group of investors who typically support the refinancing trade.

Older warehouses

For managers sitting on older warehouse facilities -- those open for six months or more -- the shorter deal could offer a different solution. These facilities contain loans gathered last year at lower spreads and they may now be marked as loss making following a slump in secondary prices in 2018.

Moreover, widening liability spreads mean the arbitrage has disappeared, hampering sales of the equity tranche. Even if manager fees are rolled into the equity pot, the day-one returns may not be enough to draw interest for the subordinated notes.

A shorter maturity deal might help improve the chances of a take out because of cheaper liabilities and also more leverage with a shorter reinvestment period, according to one U.S.-based CLO manager. That in turn can improve both the arbitrage between assets and liabilities and the equity returns.

And just with the maturing cycle motivated deals, the shorter non-call period gives the manager and equity investors the option to refinance the transaction earlier. That will allow them to reduce funding costs if liability spreads have decreased or to call the CLO earlier.

Regulation, Volatility Sparks Late-Year CLO Warehouse Rush

Investors meanwhile want to be sure that “short means short” and avoid scenarios where managers can still buy new assets after the reinvestment period or where they can extend those periods by just a vote from investors in the AAA-rated tranche.

European appetite

So far the European market hasn’t seen a shorter dated deal price this year, but investors say arrangers have been testing appetite, and that it could be an option for older warehouses should liability spreads stay wide. Either they have to wait or they may have to go for a shorter deal, said an investor.

In the U.S. this year there have also been some more innovative structures appearing on refinancing transactions, and some investors expect this trend to follow through in Europe.

BofA Cuts U.S. CLO Refi, Reset Forecast After Surprise Rout

Priced U.S. Deals

| Deal | Manager | AAA COUPON/DM | BOOKRUNNER | SIZE ($M) | REINVESTMENT | NON-CALL |

|---|---|---|---|---|---|---|

| DRSLF 2019-75A | PGIM | 118CPN | Jefferies | 428.775 | 1/15/20 | 7/15/19 |

| APRES 2019-1 | ArrowMark Colorado Holdings | 117CPN | JPM | 399.925 | 0 | 3/7/20 |

| GLM 2019-4 | GoldenTree Loan Management | 130CPN | MS/BofA/Wells | 807.75 | 4/24/24 | 4/24/21 |

| CBAM 2019-9A | CBAM CLO Management | 128CPN/128DM | Barclays | 601.05 | 2/12/22 | 2/12/20 |

| KKR 24 | KKR Financial Advisors II | 136CPN/136DM | Citi | 402 | 4/2024 | 4/2021 |

| ASRNT 2019-1A | Assurant | 135CPN/135DM | BofA | 454 | 4/20/22 | 4/20/20 |

| ARES 2019-51A | Ares | 130CPN/130DM | BNP | 507.05 | 4/2024 | 3/2021 |

| NEUB 2019-32A | Neuberger Berman Loan Advisers | 133CPN/133DM | Wells | 602.005 | 4.87Y | 2Y |

| SNDPT 2019-1A | Sount Point | 137CPN | BofA | 508.8 | 1/20/24 | 1/20/21 |

| PPMC 2019-2A | PPM Loan Management Company | 150CPN/150DM | GS | 405.6 | 4/2024 | Class A: 3Y, 2Y All Others |

| CGMS 2015-5 (Reset) | Carlyle | 132CPN/132DM | Citi | 486.125 | 1/2024 | 1/2021 |

| OCT21 2014-1 (Reset) | Octagon Credit Investors | 130CPN/130DM | Nomura | 791.5 | 2/14/24 | 2/14/21 |

| FCO 2016-7A (Middle Mkt Refi) | FCO VII CLO CM LLC | 160CPN/160DM | Natixis | 488.5 | 12/15/20 | 3/15/20 |

To contact the reporters on this story: Sarah Husband in London at shusband@bloomberg.net;Charles Williams in New York at cwilliams204@bloomberg.net

To contact the editors responsible for this story: Tom Freke at tfreke@bloomberg.net, Charles Daly

©2019 Bloomberg L.P.