Bank of England Quizzes Shadow Lenders on Downturn Risk

Bank of England Said to Quiz Shadow Lenders on Downturn Risk

(Bloomberg) --

The Bank of England has been meeting with direct lenders to gauge the industry’s resilience to slowing growth, according to two people familiar with the matter.

At least two of the biggest U.K. private credit funds met separately with members of the central bank’s financial stability unit in the past month, said the people, who asked not to be identified because the talks were private. The meetings were part of the BOE’s efforts to gauge potential sources of stress in an economic downturn, they said.

A representative for the Bank of England declined to comment on the matter.

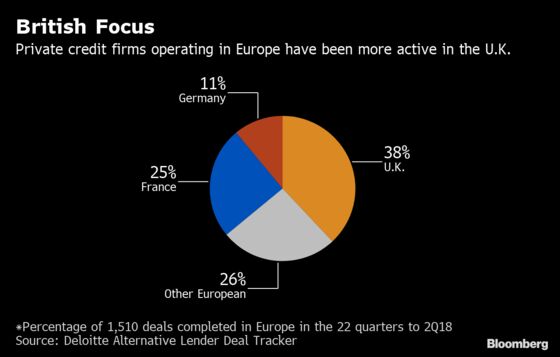

Direct lenders are starting to supplant traditional institutions in a slew of financing deals in Britain, the European epicenter of the market. Earlier this year, a single fund granted a borrower 1 billion pounds ($1.3 billion) in one of the region’s biggest private debt transactions on record. That kind of muscle is prompting regulators to examine potential spillovers to the broader economy if troubles emerges during a slowdown.

“Regulators are tracking this development closely to make sure that they understand the underlying risk of direct lending and threat of contagion,” said Floris Hovingh, a partner and head of alternative capital solutions at Deloitte LLP in London.

In its November report, the BOE’s Financial Policy Committee said it “will work to enhance the monitoring of the potential liquidity demands and losses generated by non-bank leverage” and would consider further actions if “it is found that risks reach systemic levels.”

The number of funds offering private credit mushroomed over the past decade as more traditional banks pulled back from riskier lending and regulators sought to prevent a rerun of the financial crisis. Shadow lenders, which aren’t subject to the same regulatory scrutiny, now control almost $770 billion globally as of June, up from $275 billion in 2009, according to a report from Preqin Ltd.

As capital floods into the industry and competition intensifies, more leverage has crept into deals. Recipients of “unitranche” loans tracked by Fitch Ratings carried a median ratio of 7 times debt to Ebitda as of February, compared with 6.4 times a year earlier. By comparison, peers in the syndicated loan bank market had debt of 5 times ebitda.

Standards have also become more lax. A recent study by law firm Proskauer Rose LLP showed that, of 68 private-credit transactions in Europe it worked on last year, 62 percent contained only a single covenant test. In 2017 the figure was 24 percent.

But as risks mount, it’s the funds and investors that are most vulnerable, not the wider economy, according to Edward Eyerman.

“The portfolios are made up on small borrowers who in our view would be less well-equipped to manage a long restructuring,” the head of European leveraged finance at Fitch Ratings said. “But would there be any contagion? I don’t see how a couple of direct-lending deals going bad -- or even a lot of deals going bad -- would impact on anyone other than their own investors.”

Nevertheless, the opaque nature of the funds, alongside their high-risk loans and explosive growth, have prompted U.K. officials tasked with ensuring financial stability to increase their scrutiny of the industry.

“I am not surprised the BOE is looking at private debt,” said Sebastien Galy, senior macro strategist at Nordea Investment Funds. “I too am looking for things that can go seriously wrong and one typical canary in the coal mine is credit. As one says, in times of peace, prepare for war.”

--With assistance from Lucy Meakin and Brian Swint.

To contact the reporters on this story: Cecile Gutscher in London at cgutscher@bloomberg.net;Marianna Aragao in London at mduartedeara@bloomberg.net;Rachel McGovern in Dublin at rmcgovern17@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2019 Bloomberg L.P.