Bank Crisis Is EU History Lesson in Race for Virus Bailouts

Bank Crisis Is EU History Lesson in Race for Covid-19 Bailouts

(Bloomberg) -- As the European Union lurches toward one of the worst slumps since the South Sea Bubble burst in 1720, EU regulators have adapted their playbook from more recent history to help salvage companies from the ravages of Covid-19.

Just over a decade ago, Brussels competition watchdogs had to oversee massive state bailouts doled out to a banking system on the brink of collapse.

With a credit crunch threatening to topple global economies, the EU stepped in to ensure loans started flowing but with strict conditions to prevent competition from being left in tatters by government aid paid for by taxpayers.

Back then “everybody knew bankers were overpaid,” said Karel Lannoo, chief executive officer of the Centre for European Policy Studies in Brussels. This time around, he said, the EU knows it has to be softer as businesses across a large part of the bloc’s wider economy cling on with “probably one or two months’ cash to survive.”

EU Competition Commissioner Margrethe Vestager unveiled amended rules late last week making it easier for governments to buy large stakes in companies hit by lockdowns that brought previously flourishing industries to their knees. To encourage businesses to repay the state, the rules mimic banking bailouts with no dividends, no share buybacks, a pay freeze and a bonus ban for top executives for companies still under state-ownership.

But they’ve set a soft deadline of six years for governments to scale down stakes in listed companies and will hold back -- but not entirely block -- companies from M&A. This is a break from a total takeover ban for bailed-out banks and looser time limits for repaying the state.

The rules would apply to a potential stake Germany could take in Deutsche Lufthansa AG and other recapitalizations governments are planning to save prized firms.

It is “very striking” that the virus-aid rules make no reference to credit ratings for firms that get help and a “huge difference with what happened 10 years ago” when the cost of state loans and guarantees was linked to credit ratings, said Georges Siotis, associate professor of economics at the Universidad Carlos III de Madrid. “That basically opens the door to very significant state support on equal conditions to undertakings that are fundamentally in a different position.”

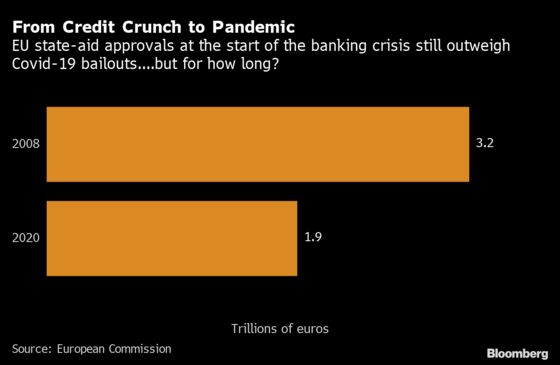

Covid-19 has forced the EU to bend rules that often prevent generous state subsidies to ensure firms in one part of Europe don’t get unfair help from their governments. More than 1.9 trillion euros ($2.1 trillion) in European government funding for companies has been approved since March with billion-euro bailouts for Lufthansa and others still to come. Vestager says she recognizes many businesses need capital but it must come with strings attached to make sure taxpayers make some return.

The rush by nation governments to save businesses reverses decades of stepping away from energy, telecommunications and transport. Under EU pressure, governments loosened regulation and allow rivals to challenge so-called incumbent firms, in the hope that more competition would lead to more innovative products and lower prices. Airlines were one of Europe’s great deregulation success stories with Irish carrier Ryanair Holdings Plc stealing market share from flag carriers such as Air France-KLM and Alitalia SpA.

Vestager said she has to uphold “the need for a level playing field to be able to bounce back strongly from this crisis.” At the same time, she’s had to meet government demands to let them shower money on their companies, and quickly.

Concerns that richer European states like Germany can outspend debt-burdened nations such as Italy have led to the EU weighing ways to take equity stakes in countries that need capital and won’t get it from their own governments.

In contrast with the banking-crisis response, new EU rules warn bailed-out companies to shun “aggressive commercial expansion” and “excessive risks.” This is less harsh than a so-called price-leadership ban that prevented bailed-out Dutch banks from undercutting rivals in the Netherlands, potentially allowing Dutch mortgage rates to climb.

Emergency rescues can become long-term burdens. Germany still hasn’t managed to sell off a 15% stake in Commerzbank AG a decade after bailing it out and would now need the share price to quadruple to break even. Royal Bank of Scotland Group Plc is still in U.K. government hands and Ireland still has large stakes in the country’s biggest banks.

Fixed time limits for a state sell-off may not work when “the expected duration of the pandemic and the associated crisis is not yet known and where the path to recovery is highly uncertain,” said Nicole Robins, an economist at Oxera.

She said the EU has instead opted for “some more flexible, yet important, conditions regarding state exit, such as imposing the adoption of a restructuring plan if exit is in doubt after six years for listed companies or seven years for other companies.”

Possibly more alarming for managers, until at least 75% of the state stake has been paid back, their pay “must not go beyond the fixed part of his/her remuneration on Dec. 31.” And “under no circumstances” should bonuses or other variable or comparable remuneration elements be paid, the EU rules say.

M&A activity is also curbed. Until at least 75% of a recap is repaid, large companies can’t acquire more than 10% of rivals, suppliers or customers in their industry. Only in “exceptional circumstances” could companies get more than a 10% stake in other firms in their industry and only if the takeover is necessary to keep the target alive.

Still, even relatively softer terms for state recapitalizations may not entice many European businesses that shy away from listing on stock exchanges and don’t have access to the commercial paper markets that help fund American companies, said Lannoo.

“Most in Europe want to maintain full control. And that is a problem,” he said, citing many family-owned firms in the region. “It is very disturbing for them to even contemplate handing over any control or risk.”

©2020 Bloomberg L.P.