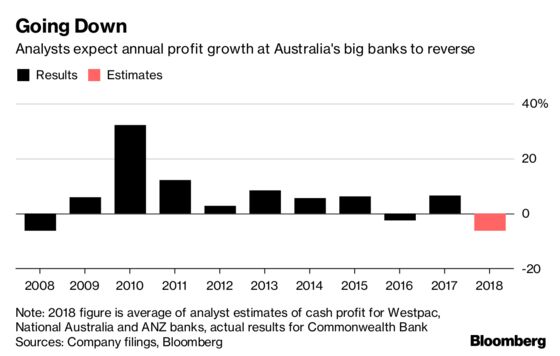

Australian Bank Earnings Expected to Be the Worst in a Decade

Australian Bank Earnings Expected to Be the Worst in a Decade

(Bloomberg) -- Australia’s big banks are set for their worst earnings season since the global financial crisis.

A softening housing market, margin pressure from rising funding costs, and the ballooning cost of dealing with the fallout from an inquiry into misconduct in the financial industry, are all squeezing profits.

Australia & New Zealand Banking Group Ltd. and National Australia Bank Ltd. are expected to report their first declines in full-year cash profit since 2016, while Westpac Banking Corp. earnings may rise just 1 percent as the banks take charges of more than A$800 million ($565 million) for the cost of wrongdoing, including compensating customers.

The inquiry into financial industry misconduct, known as a Royal Commission, found wrongdoing by the banks stemmed from greed, or the “pursuit of short-term profit at the expense of basic standards of honesty.” This led to scandals such as continuing to extract fees from the accounts of people who had died, to charging fees for no service, then lying to the regulator about the practice.

Investors are bracing for tougher regulation after the inquiry’s interim report also lambasted the securities and prudential watchdogs for being too soft on wrongdoers.

Sustained Pressure

“We see little likelihood of earnings to positively surprise given the Royal Commission and the intense political scrutiny,” UBS analysts led by Jonathan Mott write in an Oct. 23 note. “The banking sector is facing a period of substantial and sustained earnings pressure which is likely to last several years.”

The banks have also tightened lending standards amid a regulatory crackdown on risky loans, and a yearlong drop in housing prices.

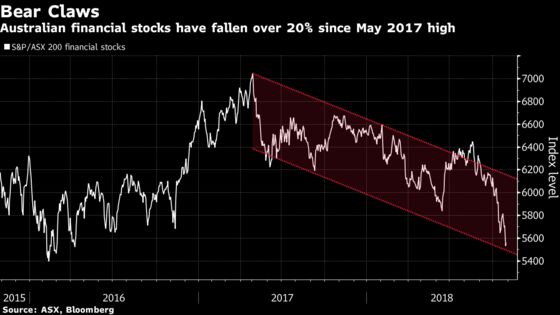

The turbulent year for the industry has come at a price, with a gauge of Australian financial stocks entering a bear market last week after falling more than 20 percent from its May 2017.

ANZ Bank (Due Oct. 31)

- Latest earnings estimates

- Morgan Stanley (Oct. 10): Looking for guidance on margins, expense growth with focus on lower absolute costs rather than targeting jaws; Unlikely to see dividend growth until FY20

- Bell Potter (Oct. 12): Sees FY profit down ~9% allowing for charges tied to customer repayments, costs; Lower mortgage broker volumes, fees and commissions also seen weighing on result

- Citi (Oct. 22): A noisy result expected with one-time items seen driving profit down in FY18; Underlying earnings likely higher amid lower bad and doubtful debts, decline in costs excluding inquiry charges; Expect capital returns A$6b out to FY20, has scope for higher 2H dividend

- UBS (Oct. 23): Result expected to be messy as ANZ continues to simplify operations; Will be hit by remediation charges, which are expected to carry over into FY19; Rev. weakness likely a factor as bank continues to de-risk; Unlikely to see benefits of mortgage repricing until 1H FY19

- Ord Minnett (Oct. 24): 2H profit seen down 13% h/h; excluding one-offs may be up 2.3% h/h on strong cost performance, rebound in trading income; Higher short-term funding costs to see NIM lower; Expected to commit to more buybacks in FY19

- Morgans (Oct. 25): Facing company-specific revenue pressure in slower housing loan growth, higher out of cycle rate increase than peers and restructuring charges; Expect Institutional unit NIM under pressure in 2H, looking for amount of cost cuts to boost RoE; Unlikely to reach institutional RoE target anytime soon; ANZ results likely to be messiest of those being reported

- Credit Suisse (Oct. 26): Expect subdued result crimped by margin and expense pressures; Expect additional charges tied to govt inquiry in FY19 to cut cash earnings 3%

National Australia Bank (Due Nov. 1)

- Latest earnings estimates

- Morgan Stanley (Oct. 10): May cut dividend in FY19 as underlying payout rate above 80% too high; Expect to see lower EPS, RoE to settle at less than 13% amid decision to increase investment; See revenue growth 2%-3%/yr next 3 years amid peak in retail margins, modest business banking growth prospects; May need extra DRP participants to get CET1 ratio above 10.5%

- Bell Potter (Oct. 12): Dividend payout ratio seen topping 90%

- Citi (Oct. 22): Business banking likely a bright spot in report; NIM likely to perform well on tailwinds via New Zealand, business banking unit; NAB expected to reprice mortgages by end 1H FY19 in line with peers amid competition; Payout level manageable with increased prospects of a raising

- UBS (Oct. 23): Strong growth in SME lending likely to support NIM, add to volume growth; SME lending may help drive rev. gain, in contrast to peers; Won’t know potential credit loss impact for another 12-24 mos; Legal, compliance costs may grow beyond UBS forecast

- Ord Minnett (Oct. 24): Rising expenses and seasonally weaker trading income to offset modest NIM growth; See CET1 ratio weaker than peers, may consider DRP discount; Focus on SME lending strength and dividend sustainability

- Morgans (Oct. 25): Currently offering highest dividend yield of major banks; Not expecting payout cuts although may see discounted DRP to help boost CET1; Leading share in SME lending to become a more important positive differentiator; Looking at NAB on three-year basis amid investment, restructure plan

- Credit Suisse (Oct. 26): Expect more subdued loan growth amid tighter lending standards; scope for dividend to be rebased; To see margin impact from increased competition, wider spreads

Macquarie Group (Due Nov. 2)

- Latest earnings estimates

- Bell Potter (Oct. 12): Remains top sector pick with scope to invest in cash and growth story; Profit seen marginally ahead of yr ago

- Citi (Oct. 22): Result likely to be broadly in line amid good core growth, GFX/tax tailwinds; Trade sale or IPO of Pexa may be a catalyst for stock; FY results seen up ~15% amid Quadrant, result on Pexa

Westpac Banking Corp. (Due Nov. 5)

- Latest earnings estimates

- Morgan Stanley (Oct. 10): Westpac has most exposure to investor, interest only loans, will need to re-balance portfolio; Strategy based on home loan, deposit re-pricing looks hard to sustain; May see higher cost growth amid investment in platforms, processes, compliance

- Citi (Oct. 22): Expect weak NIM from 3Q to continue into year end; 2H NIM may fall 11 bps to 2.06%; Govt inquiry likely to see cost growth exceed 2%-3% target; Cost growth seen outpacing rev. growth, although improved asset quality likely to see earnings slightly higher

- UBS (Oct. 23): Expected to report sharp drop in NIM in 1H; Underlying cost growth seen at high end of 2%-3% range; Asset quality remains strong; CET1 ratio may drop in 2H, return to “unquestionably strong levels" in 1H FY19

- Ord Minnett (Oct. 24): Underlying cash profit, revenue seen down h/h amid sharp drop in NIM and weaker trading income; Focus on retail banking challenges, outlook for cost savings

Commonwealth Bank (Due Nov. 7)

- Morgan Stanley (Oct. 10): Expect to see margin decline in 1Q, with expenses down ~7% excluding regulatory costs; Looking for detail on timing of wealth mgmt demerger, extra details on remediation; Looking for guidance on housing loan growth; May face declining gap on peers on RoE

- Bell Potter (Oct. 12): Sees 1Q profit down on yr ago; FY19-FY22 cash profit ests cut 3%-4% on govt bank inquiry, with cost of equity seen rising to 11.5%

- Citi (Oct. 22): FY19 earnings guidance cut 4% on remediation charge

- UBS (Oct. 23): Run rate of 1H FY implies NPAT A$2.4b, bad debts ~A$290m; Rev. likely subdued, credit growth slowing but asset quality remaining strong

--With assistance from Emily Cadman and Matthew Burgess.

To contact the reporter on this story: Tim Smith in Sydney at tsmith58@bloomberg.net

To contact the editors responsible for this story: Divya Balji at dbalji1@bloomberg.net, Peter Vercoe, Rebecca Jones

©2018 Bloomberg L.P.