Asian Investors Seek Harbor in Gulf Arab Bonds

Asian Investors Seek Harbor in Gulf Arab Bonds

(Bloomberg) -- Highly rated dollar bonds from the Middle East are emerging as a refuge for Asian bond investors as they brace for the impact of U.S. sanctions in other regions and the trade row with China.

UOB Asset Management Ltd. and Bank of Singapore Ltd. have turned overweight on Gulf debt over the past year, arguing that the region is less exposed to international trade risks. Investors had sold off Gulf bonds because of falling oil prices, tension between Qatar and a Saudi-led coalition, and Saudi Arabia’s domestic crackdown and foreign policy.

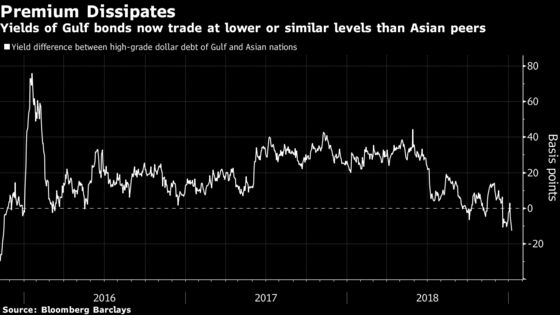

The yield on investment-grade Gulf Cooperation Council nations’ dollar debt with an average rating of A+ has fallen since reaching a 2010-high in November and now trades at a rate that’s similar to Asian securities with an average debt score of A-, according to Bloomberg Barclays indexes. Increasing awareness of better credit quality in the Middle East region, coupled with the fact that Saudi Arabia was the biggest issuer of dollar bonds among emerging markets in 2018 and 2017, have lured investors back.

Read more: Saudis Lure Investors to $7.5 Billion Bond Sale After Khashoggi

“The GCC’s relative immunity from trade tensions, high credit rating and strong local bid make the region a preferred destination in an uncertain global backdrop,” Patrick Wacker, fund manager for emerging-markets fixed income at UOB Asset in Singapore, which oversees the equivalent of $24 billion, said in an interview. “Asian fund managers have increasingly participated in the Middle East space.”

The expected inclusion in JPMorgan Chase & Co.’s emerging-market bond indexes of the debt of Saudi Arabia, Qatar, United Arab Emirates, Bahrain and Kuwait starting this month is also rekindling appetite.

High-grade sovereigns in the Gulf region are trading at cheaper or similar levels to Asian countries despite having better debt scores. The 2026 dollar bonds of Qatar, rated Aa3 by Moody’s Investors Service, have a yield of 3.746 percent compared with similar-maturity Malaysian notes, which offer 3.651 percent even though the latter is ranked three levels lower at A3, data compiled by Bloomberg show.

Other key insights from investor and analysts below:

Todd Schubert, head of fixed-income research at Bank of Singapore:

- The company turned overweight on the Gulf region given that it offered relative political stability and less headline-induced volatility after market swings in Turkey and Russia in 2018

- Asia is dominated by China, which accounts for roughly half of all the region’s outstanding emerging market corporate bond stock. The trade war between China and the U.S. has the potential to metastasize into a larger economic cold war

- The bank sees opportunities in a number of corporate bonds in Dubai, Abu Dhabi, Saudi Arabia and Kuwait as well as in select Saudi Arabian sovereign notes across the curve; it has a neutral stance on Bahrain and Oman

Wacker at UOB Asset:

- His fund turned overweight on GCC investment-grade bonds when the trifecta of higher U.S. interest rates, a stronger dollar and broad-based risk aversion came together during April of last year. He then added modestly to the fund’s overweight position as U.S.-China trade tensions took center stage

- Within GCC, he lowered his fund’s Saudi Arabia overweight as the Khashoggi saga came to light in October and rebalanced the weight to other GCC issuers

- The impact of lower crude prices may feed through sentiment for sovereign oil producers on the lower end of the ratings spectrum such as Oman. High-grades such as Abu Dhabi and Qatar have sizable external assets that will help them sustain their strong credit profiles even with lower oil prices

Christopher Langner, investment strategist at First Abu Dhabi Bank:

- The bank has seen anecdotal evidence of increased interest from investors, ranging from wealthy Chinese individuals to Taiwanese insurers and Malaysian and Indonesian institutions. The latter firms also find the Middle East appealing given the availability of sharia-compliant debt that offers decent returns for the ratings they carry and have higher liquidity than some Asian issues

- Saudi Arabia has been the obvious pick among its investors, considering the liquidity of its sovereign curve and its commitment to global capital markets

Leo Hu, senior portfolio manager for hard-currency emerging markets debt at NN Investment Partners:

- His fund favors GCC sovereign credits because the valuation is compelling and the fundamental is more or less stable

- Domestic support for the bonds is strong and the inclusion in the JPMorgan bond indexes will boost demand. Not only the locals are buying the bonds, but also international investors are acquiring them because they are relatively cheap versus other regions

--With assistance from Arif Sharif, Netty Ismail and Dana El Baltaji.

To contact the reporter on this story: Lilian Karunungan in Singapore at lkarunungan@bloomberg.net

To contact the editors responsible for this story: Tomoko Yamazaki at tyamazaki@bloomberg.net, ;Andrew Monahan at amonahan@bloomberg.net, Ken McCallum

©2019 Bloomberg L.P.