Asia's Richest Delight Banks by Abandoning Their Trading Egos

For private bankers in Asia, there’s a silver lining to the stock market meltdown that engulfed the world in late 2018.

(Bloomberg) -- For private bankers in Asia, there’s a silver lining to the stock market meltdown that engulfed the world in late 2018.

With Asia’s swelling ranks of millionaires chastened by portfolio losses, firms from Julius Baer Group Ltd. to UBS Group AG say they’re finding rich clients more open to giving them discretionary mandates, where they hand over lump sums and let the bank manage the money for a fee. For private banks, that’s a far more lucrative proposition than having customers pay per trade.

“Wealthy individuals here in Asia, over time, realize that they can’t beat the market in such a fantastic way as their egos might tell them,” said Steven Fong, head of mandate solutions for Singapore at Credit Suisse Group AG’s Asia Pacific private bank. “More clients tend to give discretionary mandates a chance after every market crisis.”

UBS and its rivals are counting on the richest folks in the world’s fastest-growing region to boost profitability. Fortunes in Asia’s $22 trillion wealth market are younger than those in Europe or the U.S., so most individuals retain control over their money, giving professional managers more room to acquire clients.

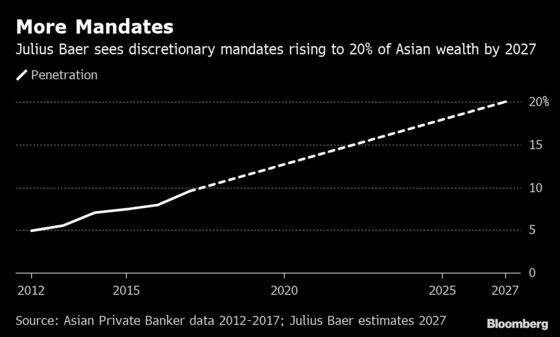

Across the industry, one third of portfolios in Europe are discretionary, said Bhaskar Laxminarayan, Julius Baer’s chief investment officer for Asia. He estimated that the overall figure for Asia is no higher than 8 percent.

Assets managed under Credit Suisse’s bespoke mandate business, which customizes investments for clients, have been growing by about 20 percent a year in Asia since 2014, though the firm declined to provide more details. The increase came amid heightened volatility on the S&P 500 Index and in the Eurozone last year, while investors are this year concerned about the impact of Brexit and slowing economic growth amid the U.S.-China trade war.

The so-called mandate business, which also includes services where the client takes the final decision on whether to execute the trade, is growing at a similar pace for UBS, according to Stefan Lecher, head of global mandates investment solutions for Asia Pacific. The firm aims to increase the proportion of Asian client assets in mandate accounts to 18 percent by 2021 from 13 percent now, he said. At JPMorgan Chase & Co., roughly 20 percent of regional client assets are managed by the bank.

Discretionary accounts provide banks with recurring income, unlike traditional clients who only pay per transaction. Thanks to the regular fees and factors including economies of scale, gross margins from mandate-based offerings can be about 0.4 percent wider, according to a UBS presentation in October. Lecher said the clients benefit, too: 85 percent of discretionary accounts at UBS outperform self-directed accounts.

“From a profitability perspective, the trend towards the discretionary mandate more broadly is very essential for UBS,” said Lecher. “Asia is very much a young market that is growing quickly.”

Delegating investment responsibility also allows a clearer demarcation between business and wealth, which is often a stumbling block when Asia’s family-owned empires prepare their succession plans. More Asian entrepreneurs want to focus their time on running their business, said Geir Espeskog, head of iShares distribution for Asia Pacific at BlackRock Inc. The trend is especially visible among new economy clients in China, according to Christopher Blum, head of investments at JPMorgan’s Asia private bank.

Julius Baer has seen its discretionary portfolio double over the last two years in Asia, aided by market volatility as clients outsource managing their money to professional investors, said Laxminarayan.

“Once you start making mistakes, especially based on your personal judgment, it really weighs on you,” he said. “It’s not fun anymore.”

--With assistance from Chanyaporn Chanjaroen.

To contact the reporter on this story: Alfred Liu in Hong Kong at aliu226@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, Jeanette Rodrigues

©2019 Bloomberg L.P.