JPMorgan Leads Banks’ Flight from Poor Neighborhoods

JPMorgan Leads Banks' Flight from Poor Neighborhoods

(Bloomberg) -- Aberdeen, Washington, is a far Northwest outpost of JPMorgan Chase & Co., with one lonely branch perched near the Pacific, 2,900 miles from Wall Street.

Now the bank is planning to depart the rainy timber town that gave the world Kurt Cobain. The next-closest Chase branch is 40 miles away.

At the same time, JPMorgan plans to open 70 branches in the vicinity of the other Washington -- the wealthy national capital. Among the new locations is suburban McLean, Virginia, the 25th richest town in the U.S.

These two different communities are in fact part of the same story. For years the nation’s largest banks have been shrinking their vast branch networks. They’ve been cutting back faster in relatively poor neighborhoods than in more affluent ones.

Even with the spread of online banking, JPMorgan and its rivals have said storefronts remain a critical part of their growth. The banks say they’re committed to serving all their customers regardless of income, a requirement of the Community Reinvestment Act.

Small Businesses

Yet, consumer advocates warn that the closings risk widening the wealth gap by leaving scores of low-income areas with less competition for services such as personal checking and small-business lending. A 2014 study by an MIT economist found that, even with other banks nearby, branch closures in low-income and minority neighborhoods made it harder for local businesses to get loans.

“Bank branches are a crucial part of financial access,” said Scott Astrada, a policy advocate at the Center for Responsible Lending. “The argument that we all live in this digital society so we don’t need bank branches is completely false.”

No major bank exemplifies the industry trend of leaving lower-income areas better than JPMorgan.

National Expansion

The biggest U.S. bank announced plans a year ago to spend billions to open 400 branches and boost lending in a national expansion that would extend the lender’s profile to new states for the first time in a decade.

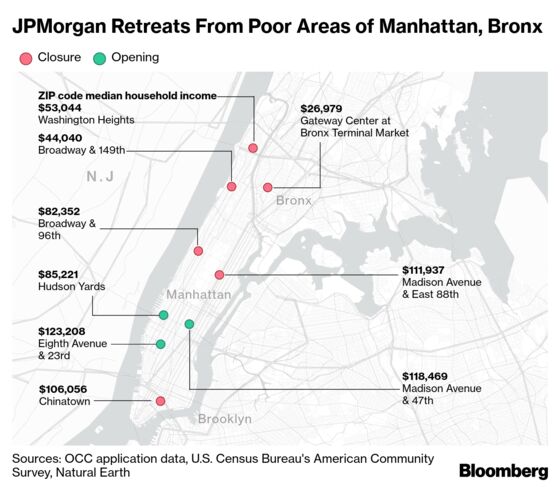

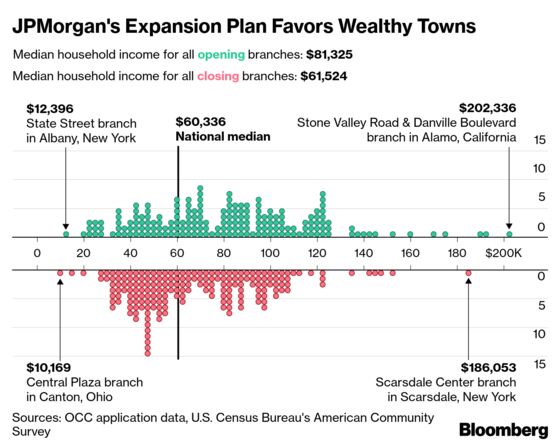

In the 13 months through January, JPMorgan has applied to open 185 new branches, with 71 percent of them in more affluent areas. The bank in that time has given notice to regulators of its intention to shut 187 branches. About half of those are in neighborhoods where household income is below the national median of $60,336, according to a Bloomberg analysis of regulatory and U.S. Census data.

Anne Pace, a JPMorgan spokeswoman, said a national view of the data is skewed because it assumes that family income in all communities is the same.

“In our footprint, Chase has significantly more branches and more deposits in low- to moderate-income neighborhoods than any other competitor,’’ Pace said in an emailed statement. “Even when we’ve consolidated branches, we continue to grow market share in those neighborhoods. In the vast majority of cases, the next closest branch is less than two miles away.’’

JPMorgan said it prefers a measure that excludes states where it doesn’t have a presence. By that measure, the firm had 26 percent of its branches in low- and moderate-income areas, while Wells Fargo & Co. and Bank of America Corp. each had 29 percent, according to data from JPMorgan. In response to questions from Bloomberg, JPMorgan said 30 percent of its new branches will be in such communities, up from an earlier pledge of at least 20 percent.

Consumer Banks

Nationally, banks have shut 1,915 more branches in lower-income neighborhoods than they’ve opened in the four years through 2018, according to S&P Global Inc. The three largest consumer banks -- JPMorgan, Wells Fargo and Bank of America -- led the way, S&P said.

JPMorgan has consistently had a smaller proportion of its branches in low- and moderate-income areas than its two rivals over the last 12 years, Federal Deposit Insurance Corp. data show.

Wells Fargo, whose growth is constrained as punishment for millions of fake accounts it opened without customer knowledge, serves “significantly more markets than any other national bank peers, including in underserved communities,” said spokeswoman Hilary O’Byrne.

Aberdeen Branch

Approximately one-third of Bank of America’s network is in low- and moderate-income neighborhoods “and that has been consistent over a number of years,” said spokeswoman Betty Riess.

Bank of America also shut its only Aberdeen branch, just across the street from JPMorgan’s -- part of a cluster of banks that once vied for deposits during the timber boom.

After taxpayers and the Federal Reserve rescued the country’s financial system, government regulators stifled JPMorgan’s growth for almost six years due to misdeeds, Bloomberg reported. The Office of the Comptroller of the Currency’s lifting of the ban last year paved the way for the expansion.

Banks are required by the Community Reinvestment Act to serve communities across a range of incomes, but the OCC has been slow to police them. The agency is supposed to examine them every four years, but none of the three biggest banks has undergone testing since 2013. An OCC spokeswoman said it will begin JPMorgan’s next examination this year. The agency declined to comment further.

CRA Revisions

Treasury Secretary Steven Mnuchin and OCC head Joseph Otting have been pushing for revisions to the CRA test that some say would weaken the law by making it easier for banks to pass.

In poor and minority neighborhoods, the number of new small-business loans declined 13 percent in the years after a branch closing, according to a 2014 paper by Hoai-Luu Q. Nguyen, then an economist at the Massachusetts Institute of Technology.

Lending in those communities tends to be driven by relationships, so once the bankers leave, residents can face higher barriers to credit access, Nguyen said.

Wealthy Customers

At a Feb. 26 investor conference, JPMorgan’s chief executive officer, Jamie Dimon, said that the bank’s “biggest opportunity” is its wealthy customers. The number of Chase Private Client branches, located inside Chase storefronts, soared from just one in 2008 to about 3,000 today. JPMorgan has captured just 1 percent of the market catering to customers with at least $250,000 in assets, Dimon said.

“It’s not that hard to say, ‘Why not 10 percent?’” he said.

JPMorgan isn’t planning to close branches only in low-income areas. Seven locations in Westchester County, New York, are slated to go, as well as in well-to-do suburbs outside Chicago, Houston and Los Angeles.

Likewise, some planned openings are in less affluent communities. Many of those, however, are in or close to universities.

A portion of JPMorgan’s proposed branch openings in the Washington area are in low-to-moderate-income communities, such as Wards 7 and 8, east of the Anacostia Freeway.

The rest will dot affluent neighborhoods. Two branches will bookend a mile stretch of popular Wilson Boulevard in Arlington, Virginia. One will sit across from a Whole Foods Market and the other a half-block from the upscale fast-casual lunch spot Sweetgreen. About a dozen banks already have locations along the strip.

“There’s a disconnect,” said Stephan Weiler, director of the Regional Economic Development Institute at Colorado State University. “They’re branching out in places that have much higher potential in terms of their balance sheet, but they’re also not providing capital to precisely those areas that need it the most.”

--With assistance from Jeremy Lin.

To contact the reporter on this story: Michelle F. Davis in New York at mdavis194@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Bob Ivry, David Scheer

©2019 Bloomberg L.P.