As Fed to Oaktree Fret Risks, Leveraged Loans Hit New Milestone

As Fed to Oaktree Fret Risks, Leveraged Loans Hit New Milestone

(Bloomberg) -- The growing chorus of voices fretting the boom in leveraged loans may wish to look away now -- because the market just got even bigger.

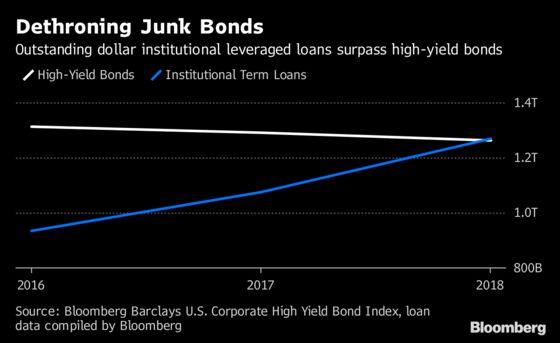

The total of outstanding U.S. dollar leveraged loans has hit $1.27 trillion, according to data compiled by Bloomberg, overtaking high-yield bonds in the past week to cement their status as the go-to financing source for speculative-grade companies. October is on course for the highest issuance since June, while junk bond sales are the slowest since 2009.

The latest surge extends a trend that’s been on show all year and which has drawn words of caution from influential figures across financial markets. Members of the Federal Open Market Committee became the latest to weigh in on Wednesday when the minutes of their latest meeting were released. For the first time policy makers made explicit that they’re watching for “possible risks to financial stability” from the leveraged loan industry.

Concerns were also voiced by the Bank for International Settlements in its quarterly outlook last month, while billionaire investor Howard Marks and JPMorgan Asset Management are among those who have pointed to leveraged loans as the bigger threat when the credit cycle turns.

“Growth has been in levered loans, not high-yield bonds,” Marks, the co-chairman of investment firm Oaktree Capital Group LLC wrote in a September memo to clients. “We think the risk level has risen in loans while remaining stable in high yield bonds.”

CLO Machine

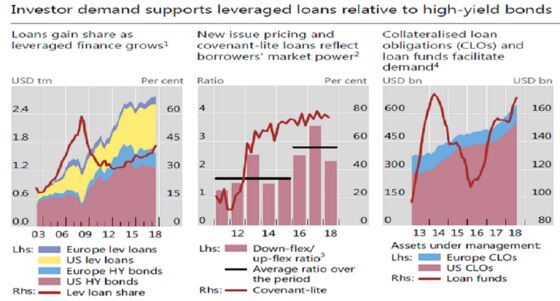

Part of the reason for the growth is ceaseless demand from Wall Street’s CLO machine.

Collateralized loan obligations, which are securitized structures built to exploit interest-rate arbitrage, raised $90 billion in the first half in the U.S., compared with $53 billion over the same period last year, according to data compiled by Bloomberg.

In the largest post-crisis leveraged buyout, Blackstone Group LP last month boosted the size of term loans in its $13.5 billion debt package to pay for its stake in Thomson Reuters Corp.’s financial-and-risk operations.

For regulators at the BIS -- sometimes called the central bank for central banks -- a boom in leveraged loans often presages a bust in the wider economy. The market is “particularly procyclical,” according to the report, and it rose faster than high-yield bonds in the run-up to the global financial crisis.

The worry is that outsized demand for loans allows excesses to flourish and debt loads to run up unchecked.

“Overall, loan documentation is weaker and there’s further evidence that new borrowers coming to the market for the first time are coming with much weaker credit than in the past,” Morningstar Credit Ratings analyst John Nagykery warned in a Sept. 24 note. “These features can enable or worsen the next crisis.”

Dodging Bonds

At JPMorgan Asset Management, Bob Michele and his colleagues have passed on some prospective high-yield bonds this year, only to discover that the borrower later circumvents the bond market entirely and sells loans.

“You find they surface later with a lower yield in the loan market, where they’re swept up by floating-rate buyers and CLOs,” said Michele, the chief investment officer and head of global fixed income at JPMorgan AM.

High debt loads look manageable so long as the U.S. economy keeps powering ahead. But as monetary policy tightens and the business cycle ages, companies that rely heavily on floating-rate loans will face bigger debt burdens, triggering defaults, the BIS and others warn.

Leveraged loans are already becoming more default-prone, with the rate of non-payment of U.S. institutional leveraged loans rising to 2.5 percent in June 2018 from about 2 percent in mid-2017, according to the BIS.

“There’s potentially an over-extension of cheap borrowing,” said Michele at JPMorgan Asset Management. “That’s always what seems to get the system in trouble.”

--With assistance from Laura Benitez, Anchalee Worrachate and Lara Wieczezynski.

To contact the reporters on this story: Cecile Gutscher in London at cgutscher@bloomberg.net;Sid Verma in London at sverma100@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Yakob Peterseil

©2018 Bloomberg L.P.