Argentine Sovereign Risk Is Overblown, Finance Secretary Says

Argentine Sovereign Risk Is Overblown, Finance Secretary Says

(Bloomberg) -- Investors have placed an excessively high risk premium on Argentine assets compared to their peers, according to Finance Secretary Santiago Bausili.

“I don’t think the relative value between Argentina and other similar credits is at a balanced level,” Bausili said in an interview in Buenos Aires. “When we compare it to other countries in the region including Brazil, there’s an overshooting on the country risk in Argentina.”

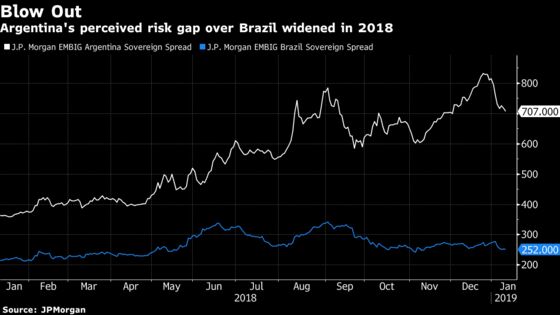

Country risk, which is the extra yield that investors demand to hold a country’s debt over U.S. Treasuries, spiked at the end of 2018 to 8.3 percentage points before narrowing in the New Year to 7.04 percentage points. Those swings have more to do with international events than with real fundamentals or change in policy at home, said Bausili, a former Deutsche Bank AG and JPMorgan Chase & Co executive.

The spread between Argentina and Brazil’s country risk has widened to more than 4.5 percentage points from just 1.4 percentage points a year ago. In that time frame President Mauricio Macri struggled to combat a currency crisis that led to a record International Monetary Fund credit line and Brazil elected a far-right conservative president vowing to impose liberal economic policies and privatizations.

Even Ecuador, with a much smaller economy, exposure to falling oil prices, no IMF credit line and a lower credit rating, is trading in line with Argentina in the bond market.

So what does Bausili see that perhaps some international fund managers are missing?

Argentina won’t tap international debt markets for the foreseeable future. Its dollar maturities over the next two years are mostly limited to a $2.75 billion bond due in April this year and another in October of next year. The government is actively trying to convert a greater percentage of its total debt into local currency and has set conservative rollover targets for its local notes known as Letes, meaning it only needs to rollover 46 percent of the debt this year to meet its plan.

“There’s no need to tap international debt markets. If there’s an opportunity to refinance long-dated peso maturities would we do something? If the conditions are favorable, yes we would. That’s being constructive and prudent,” he said. “But as of today, there’s nothing in the pipeline.”

The Treasury will also have a surplus of dollars this year. When Argentina receives revenue from export tariffs and large dollar disbursements from the IMF, it will be exchanging them for pesos, and will be able to provide more hard currency to meet any rise in demand in case there is a flight to greenbacks amid the potential political volatility ahead of October’s election.

The central bank’s plan to stamp out volatility in the peso by imposing a trading band and draining liquidity from the market has worked so far. After sinking 50 percent last year, the currency has gained 1.4 percent this year. The monetary authority intervened on Thursday to buy dollars after the rally caused the peso to trade through the floor of the band.

“What can we do to lower sovereign risk? Continue executing an Orthodox response to the crisis,” Bausili said.

To contact the reporters on this story: Patrick Gillespie in Buenos Aires at pgillespie29@bloomberg.net;Ignacio Olivera Doll in Buenos Aires at ioliveradoll@bloomberg.net;Daniel Cancel in Sao Paulo at dcancel@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, Matthew Malinowski

©2019 Bloomberg L.P.