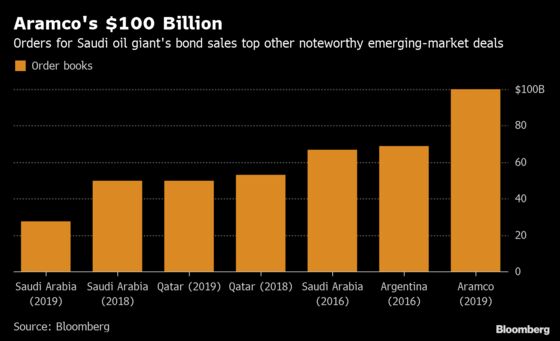

Aramco Receives Blockbuster $100 Billion Demand for Debut Bond

Aramco Receives Blockbuster $85 Billion Demand for Maiden Bond

(Bloomberg) --

After being shunned by Wall Street and international investors last year, Saudi Arabia made a historic comeback on Tuesday as oil giant Aramco received more than $100 billion in orders for its maiden global bond.

The bond sale, the most highly anticipated in recent memory, is set to be the largest-ever in emerging markets and one of just a handful of times that a company anywhere in the world received more than $100 billion in bids for a debt offer. It’s a clear sign of investors’ hunger for yield in a world where bonds from some developed nations -- and even companies -- have negative interest rates.

The anticipated low pricing and strong order book underscores the financial strength of the world’s largest -- and most profitable -- oil company. The yield on the Aramco bond is expected to be less than Saudi Arabia’s sovereign debt, which is highly unusual for a state-owned company.

Aramco’s bond sale dominated the attention of fixed-income investors globally and may have even weighed on the market for U.S. Treasuries.

Read more: Aramco Guidance Shows Oil Bonds Pricing Through Sovereign Curve

"The market shows no signs of wishing to balk at the latent political risk attached to Saudi," said Anthony Peters, a strategist at Blockex Ltd. In London.

Aramco is expected to raise $10 billion to $15 billion in the sale, which will price later today. The strong demand opens the door for the company to go even higher. By comparison, CVS Health Corp., Anheuser-Busch InBev NV and Verizon Communications Inc. all drew orders in excess of $100 billion, but also each borrowed at least $40 billion in their respective M&A transactions.

Aramco received the strongest demand for longer-dated, highest-yielding bonds, which are effectively are a bet on Saudi Arabia and oil around the year 2050. Longer-dated bonds are usually popular with pension funds and insurance companies seeking to match the duration of their assets and liabilities.

The deal is largely seen as Plan B to raise money for the Saudi Arabia’s economic agenda after the initial public offering of Aramco was postponed. In effect, Saudi Crown Prince Mohammed bin Salman, who runs the country day-to-day, is using the state oil producer’s pristine balance sheet to finance his ambitions.

For Saudi Arabia, the strong demand for the debt of its state oil company will comfort the country’s wealthy royal family, which has been in crisis mode since the assassination of journalist Jamal Khashoggi in October. The murder, which U.S. intelligence concluded was ordered by Prince Mohammed himself, triggered a global uproar that prompted Wall Street banks, investors and business tycoons to give the kingdom a cold shoulder.

Political Turnaround

An investment summit in Riyadh that month dubbed “Davos in the Desert” was mostly boycotted by its A-list participants. Yet, little by little, the power of money has attracted Wall Street again, first at the real World Economic Forum in Davos, Switzerland, where bank bosses said it was time to let the kingdom out of the penalty box. And later in the bond market itself, where the Saudi government successfully raised debt this year.

The Aramco bond sale will be final confirmation of the turnaround for the Middle Eastern nation. The company told investors it would sell debt in six portions, from three to 30 years, according to the people familiar with the matter.

Given the massive demand, Aramco told investors on Tuesday it expects to pay about 1.1 percentage points more than U.S. Treasuries for its 10-year notes, compared with Saudi sovereign bonds trading about 1.2 percentage points. The indicative price of Aramco’s bonds dropped by 15 basis points from initial price talk on Monday.

In addition to potentially luring away U.S. debt investors seeking higher yields, the Aramco deal may weigh on Treasuries through the mechanics of how bonds are sold. Issuers of dollar-denominated debt often enter into what’s known as rate-lock agreements, in which they bet on Treasury prices falling to guard against higher yields. Once the debt is sold, the wagers are ended.

What Bloomberg Intelligence Says"Saudi Arabia’s fiscal reliance on Aramco may eventually drive spreads on the oil company’s proposed bonds significantly wider than those of similar maturity sovereigns. Longer-maturity issues will be more susceptible to this trend, in our view, despite a solid cash balance that offsets any near-term increase in corporate debt."--Jaimin Patel, energy credit analyst Click here to read the research |

This isn’t the first time Saudi Arabia has turned to debt markets since the death of Khashoggi. In January, the nation sold $7.5 billion in international bonds, the first sign that the outcry hadn’t stifled foreign investors’ interest in the country.

Banking Friends

Aramco has lined up a roster of international banks supporting its jumbo bond deal, another indication of how the mood in Wall Street toward the kingdom has changed. The banks not only want to participate on the bond sale, but also ensure they’re well placed in case Aramco goes ahead with its planned IPO.

Jamie Dimon, JPMorgan Chase & Co.’s chief executive officer, spoke at a lunch in New York Thursday to market the deal, according to one person familiar with the matter. Last year, Dimon and others skipped the investment conference in Riyadh, but still sent senior bankers to make sure they kept their contacts with the kingdom.

JPMorgan and Morgan Stanley are managing the bond sale along with Citigroup Inc., Goldman Sachs Group Inc., HSBC Holdings Plc, and NCB Capital Co.

The bond sale, being pitched to investors over the last week in a global roadshow from Tokyo to New York and London, has forced Aramco to reveal financial and operational secrets held closely since the company’s nationalization in the late 1970s, shedding a light on the relationship between the kingdom and its most important asset.

Both Fitch Ratings and Moody’s Investors Service assigned Aramco the fifth-highest investment-grade rating, the same as Saudi sovereign debt, but lower than oil majors Exxon Mobil Corp., Royal Dutch Shell Plc and Chevron Corp.

The company plans to use the proceeds of the bond sale to pay part of the $69 billion acquisition of a majority stake in local petrochemical company Sabic from the country’s sovereign wealth fund. The deal between three government-owned entities -- where the kingdom’s sovereign wealth fund sells its 70 percent stake in Sabic to Aramco -- moves money from one pocket of the state to another.

--With assistance from Brian Smith, Molly Smith and Neil Denslow.

To contact the reporters on this story: Javier Blas in London at jblas3@bloomberg.net;Archana Narayanan in Dubai at anarayanan16@bloomberg.net;Lyubov Pronina in Brussels at lpronina@bloomberg.net

To contact the editors responsible for this story: Will Kennedy at wkennedy3@bloomberg.net, Lynn Thomasson, Shannon D. Harrington

©2019 Bloomberg L.P.