Apple Results Spark Rally But Wall Street Remains Cautious

Apple Results Spark Rally But Wall Street Remains Cautious

(Bloomberg) -- Signs of a recovery in demand for Apple Inc.’s iPhone reassured investors and sparked positive commentary on Wall Street, even as many analysts remain reluctant to get significantly more bullish on the stock after a 33 percent run-up this year.

The tech giant’s fiscal second-quarter results and third-quarter forecast will “help fuel the bull case,” according to analysts at Jefferies. The bank was one of several that raised its price target on Apple shares after the results. The average analyst target among 36 firms tracked by Bloomberg is now $213, up from $206 on Tuesday, but that implies just 1 percent upside from the current price.

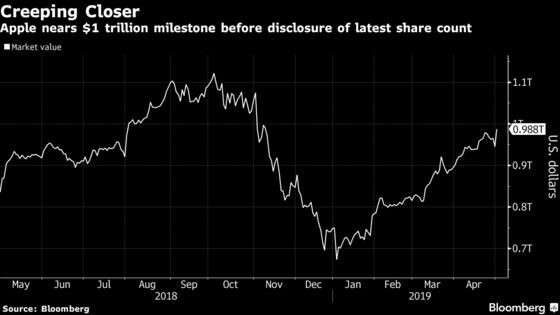

The stock rose 4.4 percent at 9:35 a.m. in New York. Apple’s market value will likely remain below the closely watched $1 trillion threshold when the company discloses how many shares are outstanding in its quarterly regulatory filing, expected after the close of trading.

Here’s what analysts are saying about Apple’s results:

JEFFERIES (Timothy O’Shea)

- Apple’s second quarter results will help fuel the bull case with a “nice” beat on revenue and EPS and third quarter revenue guidance ahead at the midpoint

- Investors will react favorably to commentary around improvements in China demand

- Apple continues to be a Services and Wearables-led growth story, and Jefferies was particularly encouraged by the Services number considering the lack of mobile game approval in China drove App Store weakness

- Jefferies has hold rating; target increased to $210 from $160

PIPER JAFFRAY (Michael J Olson)

- Fundamental performance was “strong” and Apple will be returning more cash to shareholders

- Expects “limited excitement” around this year’s iPhone launches

- However, as long as services revenue continues to perform at or above expectations, this will tide investors over until anticipation for 5G iPhones begins to build

- Piper Jaffray has an overweight recommendation; target raised to $230 from $201

MORGAN STANLEY (Katy L. Huberty)

- Better-than-expected June quarter guidance and more bullish iPhone commentary were positive surprises against cautious investor positioning

- Demand was helped by trade-in and financing programs, stimulus in China such as VAT tax reduction, and improved consumer confidence from advancing trade dialogue between the U.S. and China

- Next catalysts are a re-acceleration in Services in the second half and the launch of 5G in 2020

- Morgan Stanley’s rating is overweight; price target raised to $240 from $234

WEDBUSH (Daniel Ives)

- Better-than-expected headline numbers will be a “major sigh of relief” for investors and will give the bulls “another feather in their cap” going into the next few quarters

- While China appears to be soft, Apple saw strength in the last few weeks of the quarter across the board on a rebound in iPhone demand

- Company beating the Street will put shares on a path to make new highs over the next three to six months

- Wedbush has an outperform rating; price target raised to $235 from $225

HSBC (Erwan Rambourg)

- Apple’s 3Q guidance looks reassuring in terms of sales, although not as solid from a cost/margin perspective

- Investors may be reassured by China comments and impressed by the cash return

- However, HSBC does not expect many upgrades to come through to operating income given sales look in-line or a bit better, but costs were a bit heavier than expected

- HSBC has a reduce rating and a target of $180, among lowest on Street, according to data compiled by Bloomberg

GOLDMAN SACHS (Rod Hall)

- “Pleasantly surprised” by positive trends in iPad, Wearable and Mac in both reported revenues and guidance, although iPhone numbers were weaker than Goldman expected

- Operating expense guidance implies operating margins of around 21 percent, the lowest since 2008

- Believes fundamentals get more challenging as the year progresses and that the stock remains toward the top of its valuation range versus the S&P 500

- Goldman has a neutral rating and price target of $184

What Bloomberg Intelligence says

Apple’s year ahead may not be as bad as feared. The company expects continued strength in all non-iPhone categories and marginally better iPhone growth relative to the first quarter, suggesting the worst may be over.

-- John Butler, senior telecom analyst

-- Click here for the research

--With assistance from Ryan Vlastelica and William Canny.

To contact the reporter on this story: Kit Rees in London at krees1@bloomberg.net

To contact the editors responsible for this story: Beth Mellor at bmellor@bloomberg.net, Catherine Larkin

©2019 Bloomberg L.P.