Apollo Thinks It’s Big Enough, Tough Enough to Be GE Capital

Apollo Global Management, is slowly picking off pieces of the finance arm that nearly brought down General Electric Co.

(Bloomberg) -- Jim Zelter says he wants to build the GE Capital of tomorrow.

You read that right.

Zelter’s firm, Apollo Global Management, is slowly picking off pieces of the finance arm that nearly brought down General Electric Co.

Apollo has already bought billions of investments once managed by GE Capital, and it’s been sizing up GE’s insurance and jet-leasing businesses, people familiar with the matter have said. GE’s new leader, Larry Culp, is working to turn around the embattled conglomerate, which expects negative cash flow this year in its industrial businesses.

It’s quite a switch for both GE and Apollo, the buyout giant led by Leon Black. Apollo is trying to rekindle some of GE’s old magic without repeating the company’s mistakes, which led to a 2008 taxpayer bailout. Few think it’ll be easy to recreate GE Capital, which, at its peak, held more than $500 billion in assets, dwarfing Wall Street rivals.

“Apollo can still build a great business, but it’s quite hard to build one of the scale and breadth that GE built,” said John Dionne, a senior lecturer at Harvard Business School and a senior adviser to one of Apollo’s closest competitors, Blackstone Group LP.

The talks with GE aren’t Apollo’s only foray into industrial financing. On Thursday, it agreed to buy a majority stake in Direct ChassisLink, one of the largest companies for chassis leasing and other services to shipping firms, railroads, terminal operators and logistics companies. The price: $2.5 billion, according to a report by Reuters.

Wall Street

It’s part of the reordering of Wall Street following the longest recession in 70 years. No longer do the biggest banks have domain over extending credit. The so-called shadow banking system has filled the gaps where regulators limited deposit-taking institutions, and firms like Apollo have swooped in to take advantage. Regulators employ less oversight on shadow banks, which don’t take customer deposits.

In the meantime, GE Capital has shrunk to about one-fifth its peak size.

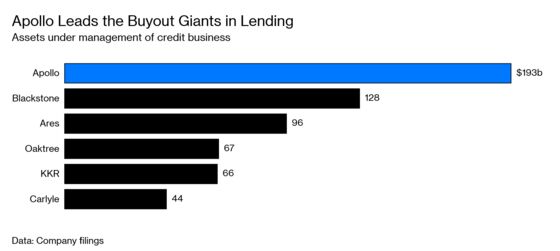

Zelter, Apollo’s co-president, is betting Apollo can do GE Capital better than GE could. Apollo’s credit business already manages $193 billion, the most of its private equity rivals. The New York-based firm will benefit from a range of funding sources that GE Capital could only envy. They include investors in its funds, its own employees and Athene Holding Ltd., an insurance company with more than $125 billion in assets and most of its funds invested with Apollo.

“I don’t come into work every day thinking I want to have a bigger business than everyone else,” Zelter said in an interview. “Size is a result, not an objective.” Zelter and an Apollo spokesman declined to comment on any discussions regarding transactions with GE.

Debt Markets

Apollo’s three co-founders, Black, Josh Harris and Marc Rowan, know their way around debt markets, having built their careers at Drexel Burnham Lambert, the junk-bond pioneer run by Michael Milken. Harris has had his eye on GE Capital assets since at least 2015.

The firm is no stranger to GE Capital. It boosted the growth of MidCap Financial in 2015 with the purchase of $3.6 billion in loans managed by GE Capital and Abu Dhabi’s Mubadala Development Co. Apollo had acquired MidCap, a health-care lender with a $2 billion portfolio at the time, two years earlier.

MidCap now has more than $19 billion of commitments and is one of Apollo’s largest permanent-capital vehicles, meaning investors can’t pull their money out on short notice. MidCap’s 2018 returns were 19 percent, according to a February investor presentation. It finances real estate, mid-market companies and corporate takeovers led by other -- usually smaller -- private equity firms.

Leasing Jets

Merx Aviation Finance, which Apollo created in 2012, also boosted growth through an acquisition from GE Capital. It bought 26 planes from GE Capital Aviation Services in 2013, launching the buyout firm’s jet-leasing business. Merx has acquired 168 aircraft since its founding.

One of Apollo’s ready-made money sources -- its own employees and investors -- gave the firm the luxury last year of replacing a $275 million leveraged loan sale that had failed to clear the market. They provided additional equity to close the acquisition of a $1 billion portfolio of energy investments from GE Capital, people familiar with the transaction said.

Apollo and Athene have expressed interest in buying all or part of GE Capital’s insurance business, people familiar with the matter have said. Problems at the unit have caused the industrial conglomerate to take billions of dollars in writedowns and spurred a regulatory review.

Underwriting Loans

Culp said it “remains to be seen” whether GE will sell the insurance division or continue to manage it as a runoff liability. Apollo is one of only a few potential buyers that would be able to acquire such a portfolio. Blackstone has expressed interest in helping to manage the assets rather than taking on the liabilities directly, people familiar with the matter said.

Another advantage Apollo has over its peers: It chooses to underwrite most of its loans. Jim Belardi, Athene’s CEO, told investors that Apollo had about 150 people dedicated to direct origination and looks to double that. MidCap originates loans, and Athene also partly owns AmeriHome Mortgage Co. Apollo and Athene have said they’re looking to create more debt originators.

Apollo’s long-term capital fuels the growth of its lending business and gives the buyout giant “the ability to be more patient with investments,” according to Steve Biggar, an Argus Research Corp. analyst. Investors lock their money in credit funds and liabilities managed by Athene for as long as 10 years. So-called permanent capital also comes from a publicly traded business-development corporation and a mortgage REIT.

Investors, including Apollo rivals Blackstone, KKR & Co. and Carlyle Group LP, are crowding into the credit business. The market is getting riskier, according to industry leaders such as Howard Marks, the co-founder of $120 billion Oaktree Capital Group. Marks said last year that it’s time to take some money off the table.

“There’s no doubt we’re at later stages of the cycle,’’ Zelter said. “I wouldn’t want to be investing today unless I had a large, diverse platform.’’ Like Apollo’s.

--With assistance from Richard Clough.

To contact the reporters on this story: Sonali Basak in New York at sbasak7@bloomberg.net;Davide Scigliuzzo in New York at dscigliuzzo2@bloomberg.net;Sabrina Willmer in Boston at swillmer2@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, ;Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, ;Margaret Collins at mcollins45@bloomberg.net, Bob Ivry, Steve Dickson

©2019 Bloomberg L.P.