(Bloomberg Opinion) -- Anglo American Plc is dabbling in creative M&A. Buying an English fertilizer project for just over $500 million, excluding debt, is more than manageable for a $35 billion mining giant that generated $1.3 billion in free cash flow in the first half of last year. It’s also a gamble on an unproven niche market that speaks to the paucity of large-scale acquisition options for cashed-up diggers.

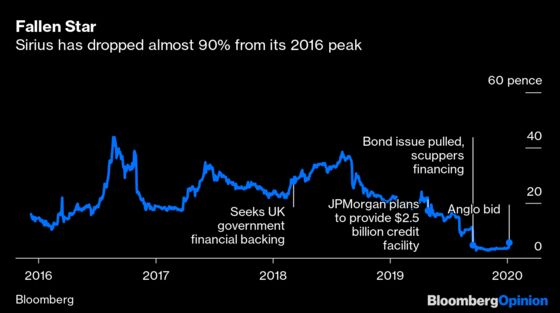

Anglo said on Wednesday it may bid for London-listed Sirius Minerals Plc, owner of a giant potash project under the North York Moors national park. The mine’s future has been in question since a funding plan collapsed last year, after Sirius was forced to pull a $500 million junk bond sale, making it impossible to unlock a $2.5 billion credit facility from JPMorgan Chase & Co.

That makes this an opportunistic move by Chief Executive Officer Mark Cutifani. Anglo is offering 5.5 pence per share for a stock that traded at four times that less than a year ago. It’s an affordable option — Anglo can easily support both the cost of the initial deal and a development spend estimated at $300 million a year for the next two years.

It’s a laudable effort at diversification too, away from South Africa, into a counter-cyclical commodity and a space the miner hasn’t been in since selling its niobium and phosphates business in Brazil in 2016. It’s also purchasing at a relatively low point for fertilizer ingredients — notable for an industry that in the past burned billions buying at the top.

None of this means Anglo should press ahead with a firm offer.

Anglo shareholders still bear bruises from its disastrous, peak-of-the-market Minas Rio deal – a Brazilian iron-ore project that was plagued by years of cost overruns and delays, and ultimately contributed to the departure of Cutifani’s predecessor. The $5 billion Quellaveco copper mine in Peru, meanwhile, which was supposed to prove Anglo’s ability to build from scratch, is still two years from production.

Anglo argues the Sirius development is far more advanced than Minas Rio was. That’s true. But it will still require some $3 billion, by Sirius estimates, and a 37-kilometer (23-mile) tunnel under a national park, for a conveyor belt to take rock to port. A challenge, even with permits in hand.

Investors should be far more worried about Anglo bosses’ willingness to bet on a project where demand for the end product — an alternative to traditional potassium-bearing minerals called polyhalite — is unproven, and prices are unclear. The selling point is that it combines several key nutrients along with potassium — magnesium, sulfur and calcium — and is low-chloride too, which matters for some crops. It’s unclear how those extras are valued, though.

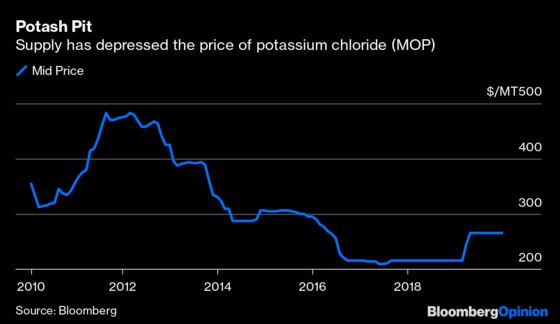

Only one company, Israel Chemicals Ltd., currently produces polyhalite, from one mine. Price estimates range from $100 to $200 per metric ton, making the economics difficult to calculate, including Sirius’s promised 50%-plus Ebitda margin.

Polyhalite accounts for a tiny sliver of the wider potash market, even among low-chloride alternatives, largely because it contains far less potassium.

That means the capacity of the Yorkshire mine dwarfs current demand. The polyhalite market amounts to less than one million tons a year, but the Yorkshire mine could produce 13 million tons. That’s a mighty step up, even accounting for the purchase agreements Sirius has already signed. Success will require building substantial new demand and clawing market share away from potash giants like Nutrien Ltd. With plentiful supply of standard potash in the medium term, that may be a challenge.

There is some element of reassurance here. Even if it bids, Anglo won’t be committing to develop the mine, making this an option of sorts.

That’s small consolation for investors, though, who will fret that cash-rich miners looking for growth — and wary of overspending on coveted metals like copper — will begin to experiment. Expect mixed results.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Clara Ferreira Marques is a Bloomberg Opinion columnist covering commodities and environmental, social and governance issues. Previously, she was an associate editor for Reuters Breakingviews, and editor and correspondent for Reuters in Singapore, India, the U.K., Italy and Russia.

©2020 Bloomberg L.P.