An $8 Billion U-Turn Works for Europe’s Top Tech Firm

(Bloomberg Opinion) -- It’s not a good look to sell a company less than two years after buying it. But SAP SE’s planned listing of its Qualtrics unit makes sense for the same reason the original acquisition by Europe’s largest technology company was flawed.

SAP’s then-Chief Executive Officer Bill McDermott agreed to pay $8 billion for Qualtrics in 2018 to expand into customer satisfaction surveys. This record purchase for the company always looked more like desperation than sound strategy, coming as it did after repeated promises that there would be no more big deals. With sales expansion slowing at SAP, the Utah-based startup’s 40% growth rate was attractive. The deal was to be McDermott’s last: he was replaced in October last year.

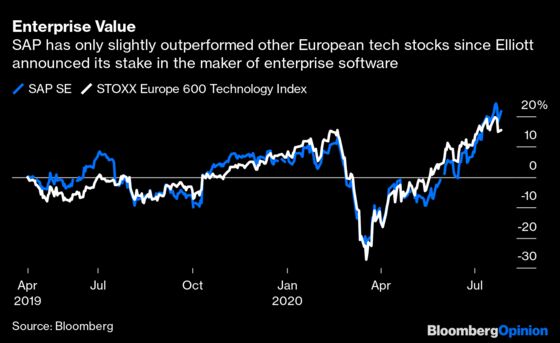

Customers and investors alike have justifiably complained about SAP’s poor record at integrating its existing acquisitions – McDermott spent $31 billion in nine years at the helm, and many of those technologies continued to work poorly together. The need for change became more urgent when the activist investor Elliott Management Corp. announced in April 2019 that it had built a stake in the German firm, and called for “focused execution on these operational opportunities.” In other words: Stop buying new stuff and make everything you already have work better.

After a brief stint with two co-CEOs, SAP is now led by former Chief Operating Officer Christian Klein. The plan to list Qualtrics is the first stamp of his authority and unraveling of his predecessor’s approach.

It was open to doubt from the start whether Qualtrics could perform better as a division of SAP than as an independent company. So-called customer experience management was a new business area for the German acquirer, and beyond the use of the parent’s sales teams, there was little obvious crossover with the rest of the operations.

The rationale for the initial public offering announced on Monday therefore appears to be grounded more in operational logic than financial chicanery. Sure, a spin-off will shine some light on Qualtrics’ value and raise some cash, but these benefits will be incremental when SAP is already valued at 170 billion euros ($200 billion).

Some customer experience rivals are valued more generously than SAP, but not by much: Medallia Inc. has an enterprise value of seven times next year’s expected sales, versus SAP’s 5.9 times multiple. The impact of any share repurchase funded by a Qualtrics divestment would also be small. Jefferies analysts value Qualtrics at between 5.2 billion euros and 14 billion euros. Were SAP to sell a little under half of the unit, a buyback would represent at most 4% of the outstanding shares.

But it makes sense to recognize that Qualtrics will probably thrive better at arm’s length from its new owner. Giving the business its own stock creates a potentially attractive acquisition currency. That may appear to provide Klein with some air cover to do deals via the subsidiary without looking like it’s another round of SAP empire building. But whether it’s SAP or Qualtrics doing the M&A, investors will hope the lessons of the McDermott era have been heeded.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2020 Bloomberg L.P.