Americans’ Credit Card Debt Poised to Reach 10-Year High

Americans’ Souring Credit Card Debt Poised to Reach 10-Year High

(Bloomberg) -- Americans are projected to fall seriously behind on their credit card bills at the highest rate in a decade as banks push a record number of people to get plastic.

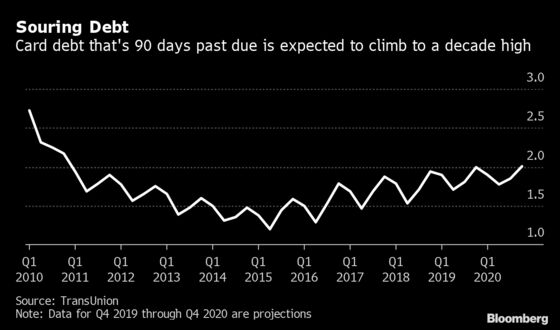

The share of credit card borrowers who are at least 90 days past due on their accounts will probably tick up to 2.01% next year, the highest level since 2010, according to a forecast by TransUnion. Still, the credit-rating company said the increase isn’t a cause for concern, noting that bad card debt still remains much lower than the level seen during the last recession.

“This is well-managed delinquency,” Matt Komos, TransUnion’s vice president of research and consulting, said in an interview. “It’s still healthy. This uptick is not concerning with the amount that credit has been expanding.”

The number of people with access to revolving credit reached a record 200.5 million in the third quarter. That figure was helped by private-label credit card originations, which reversed a 10-quarter slump by posting 2.4% growth, according to TransUnion.

As lenders sign up more people for credit cards, the newest borrowers are increasingly falling behind on their bills. Accounts opened in recent years have been souring at faster clips than prior years, suggesting that more new borrowers are struggling to keep up with their minimum payments. For instance, 5.4% of credit cards originated in 2018 were delinquent within nine months, up from 4.5% the year before.

Major card issuers including American Express Co. and Discover Financial Services have warned they’ve begun to tighten their credit standards in anticipation of a potential economic downturn. Still, lenders say their customers have continued to keep up with their bills as the U.S. unemployment rate remains near historic lows.

“The fact that a lot more people are employed and wages are going up, I think that’s certainly helping,” Margaret Keane, chief executive officer of Synchrony Financial, told investors at a conference this week. “Pretty much all what I would call ‘precursor signs’ of what we’d start to see if there’s pressure in the system, none of those are coming to fruition.”

Increasing distress in credit cards contrasts with how Americans are handling other major sources of debt. The share of seriously late payments in auto, home and unsecured personal loans are projected to fall next year, TransUnion data show.

To contact the reporters on this story: Jenny Surane in New York at jsurane4@bloomberg.net;Shahien Nasiripour in New York at snasiripour1@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Daniel Taub, David Scheer

©2019 Bloomberg L.P.