Amarin Stock Jumps as Debate Moves to Heart Drug’s Potential Label

Amarin Stock Jumps as Debate Moves to Heart Drug’s Potential Label

(Bloomberg) -- The unanimous panel backing to expand the label for Amarin Corp.’s heart drug Vascepa sparked debate across Wall Street as analysts and investors weighed whether the drug could be sold to as many as 15 million Americans.

The divide comes after members of an advisory panel to the U.S. Food and Drug Administration “offered different opinions when it came to specific recommendations for a potential Vascepa label,” according to analysts at Roth Capital Partners. That may leave billions in sales hanging in the balance. But Jefferies’ Michael Yee disagreed, saying the “label debate doesn’t really matter to the thesis” for investors. He believes doctors will use the drug “widely across patients.”

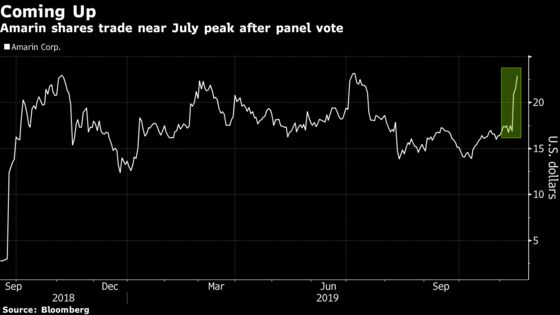

Amarin shares climbed as much as 11% Friday after being halted all day Thursday. With the stock briefly nearing $24 a share, it traded about a nickel short of a July peak.

Read more: Amarin Judgment Day for Heart Drug Has 400% Returns at Stake

Here’s what analysts had to say about the news.

Roth Capital Partners, Yasmeen Rahimi

“With unanimously favorable response for label expansion, question moves to which patients make it on label, with 10/16 docs voting in favor of both” atherosclerotic cardiovascular disease groups. Roth highlighted that some committee members “were caught up with analysis that showed a 12% relative CV risk reduction” without significant benefit for patients who had not had something like a heart attack or stroke and are at a lower risk.

Counted 10 of the 16 panelists “who were receptive to Vascepa label expansion including primary and secondary prevention patients” with the six others wanting the drug’s label to include patients who have had a stroke, or have cardiovascular disease.

Says there was “lots of safety talk, but vote indicated AdCom members felt the two signals could be adequately managed through label, thus meaning no patient restrictions.”

Maintains buy rating with $31 price target.

Jefferies, Michael Yee

“Our thesis and valuation are not based on specific ‘details’ of a label as we think docs will use this widely across patients...if stock was down, we think it bounces since label details don’t matter in big picture.”

Notes that while Amarin got the positive vote for approval, “investors will debate whether the labeled indication will include a more broad ‘primary prevention’ (high-risk) population which is patients w/o established CV disease but have diabetes and at least one other major” cardiovascular risk factor.

Highlights that the “stock has already run-up a lot and we wouldn’t be surprised if it’s volatile on this labeling discussion but we aren’t changing numbers as the populations are huge already.”

Maintains buy rating, $30 price target.

Cantor Fitzgerald, Louise Chen

“There were few-to-no surprises brought up during the meeting, in our view, and we think Vascepa is well on-track now for expected approval by year-end.”

Notes that most of the meeting “focused on concerns about the impact of mineral oil, as well as on which patient populations should be included in the label. Although some AdCom members believe mineral oil may have affected results somewhat, they agreed that the REDUCE-IT data are meaningful enough to warrant approval.”

Highlighted that panelist discussions on how high patients’ triglycerides, a type of fat in the blood, must be to benefit were “less clear-cut compared to the mineral oil debate.”

Maintains overweight rating with a $35 price target.

Citi, Joel Beatty

Amarin is unlikely to reach a market value above $10 billion over the next several months with its market value at $7.7 billion as of Wednesday’s close.

Sees the drug as “likely to be used in high-risk primary prevention patients regardless of” the exact label wording, though there will likely be some debate over the coming weeks regarding the label.

“We believe the exact wording of the indication matters relatively little compared to other drugs, because we believe physicians will still use Vascepa in very high risk” primary prevention patients.

Maintains buy rating and $23 price target.

Stifel, Derek Archila

“While the panel was in agreement Vascepa should be approved for secondary prevention patients (our base case), the key question that remains is whether or not Vascepa will receive a broader label inclusive of primary prevention patients, which would be upside to our model.”

“We believe approval in secondary prevention alone offers an addressable market that is at least ~10-15 million patients for Vascepa, making us comfortable with our ~$3 billion in peak sales estimate.”

Rates shares at buy with a $26 price target.

To contact the reporter on this story: Bailey Lipschultz in New York at blipschultz@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Scott Schnipper, Richard Richtmyer

©2019 Bloomberg L.P.