PG&E Bankruptcy's Ripple Effects Will be Felt Beyond California

PG&E Bankruptcy's Ripple Effects Will be Felt Beyond California

(Bloomberg) -- PG&E Corp., owner of the largest electric utility in America’s most populous state, plans to file for bankruptcy Tuesday, and the ripple effects are likely to stretch far beyond California and the company’s stakeholders.

Power-plant operators that sell electricity to its utility are already being downgraded to junk. Federal taxpayers may get stuck with the bill for government loans to renewable-power projects in California if they can’t be repaid. And the shape of the Golden State’s electricity industry could fundamentally change, with delays to a clean-energy mandate and a bigger role than ever before for public power.

More directly affected, of course, are stockholders, bondholders and thousands of PG&E retirees and their families who are casting nervous eyes on the pension fund. Wildfire victims suing the company -- PG&E’s stated main reason for bankruptcy -– also risk later, smaller settlements.

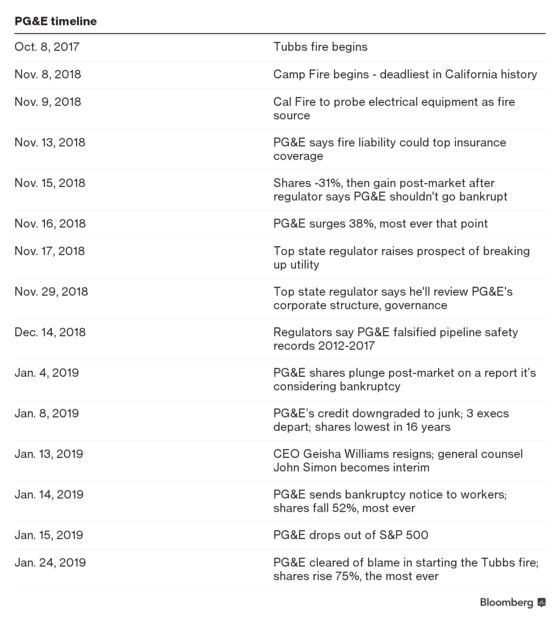

PG&E’s shares rose 2 percent to end the session at $12.01. They traded between $10.61 and $14.15.

Here are all of the companies and groups which may be affected by PG&E’s bankruptcy.

Meet the stakeholders

Sixteen million people in northern and central California -- or about 40 percent of the state’s population -- rely on PG&E for power and natural gas. It employs 23,000 and has almost as many retirees and family members drawing pensions.

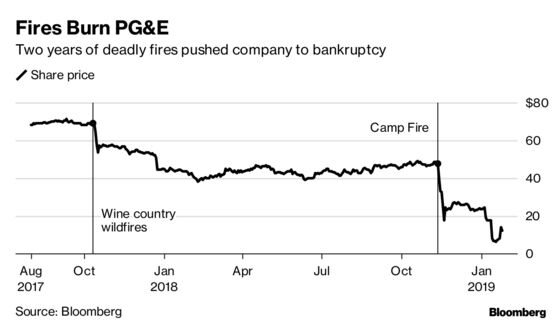

- Customers could see higher rates as the company seeks to share the pain of potential liabilities of as much as $30 billion from wildfires in 2017 and 2018.

- “There’s either going to be a bankruptcy or a bailout, and, one way or another, PG&E’s going to try to get more money out of us,” said Mindy Spatt, communications director for the Utility Reform Network consumer group. She said the bankruptcy process gives greater emphasis to the concerns of creditors than customers. “Even though we customers are at such enormous financial risk, we don’t automatically get a voice in bankruptcy court.”

- Stockholders may be able to make the case that they shouldn’t be diluted in favor of bondholders. PG&E’s stock price has plunged more than 80 percent since the 2017 fires broke out but hasn’t neared zero, indicating that investors think that there is recovery value. Investors haven’t received a dividend since 2017, and they won’t until the company exits bankruptcy, most likely in several years.

- Bondholders have begun to organize in anticipation of the bankruptcy. The Pacific Gas & Electric utility’s debt has dropped in recent weeks but much of the unsecured bonds still trade with yields below 10 percent, suggesting investors aren’t overly concerned about their recovery. Bondholders were made whole in the unit’s last bankruptcy, in 2001.

- Wildfire victims suing PG&E may be forced to accept smaller settlements than they might have won otherwise. State investigators have blamed many of the blazes on PG&E equipment.

- There’s a “low probability but a high risk” that PG&E’s pension “will be put into play during a bankruptcy,” said Tom Dalzell, business manager of IBEW 1245, which represents over 12,000 workers at PG&E. “We are paying quite a lot of attention to it.”

Collateral damage

A lot of companies are getting caught in the downdraft.

- Gas suppliers fear nonpayment, and some are already taking steps to protect themselves, restricting sales to the company.

- Owners of several solar-power plants that sell to PG&E -- including a solar complex owned by Warren Buffett’s Berkshire Hathaway Inc. -- have been downgraded by the rating agencies, and the phenomenon could spread.

- Investors in California’s municipal bonds are watching to determine whether the state offers any assistance that would affect its finances as well as any potential effect from higher customer rates.

- Five banks that have agreed to act as buyers of last resort for more than $760 million of bonds that the teetering utility issued through California government agencies may face large liabilities.

- The bankruptcy could hurt California’s credit rating, which could cause state borrowing costs to rise.

- Shares in California’s other utilities aren’t performing as well as the industry average.

- Edison International’s Southern California Edison utility and Sempra Energy’s San Diego Gas & Electric both saw their credit ratings cut by Standard & Poor’s after PG&E’s bankruptcy prompted the agency to reassess all California utilities.

- “The sharp increase in the magnitude and frequency of catastrophic wildfires in California in 2017 and 2018 underscores risk that this phenomenon may continue into the future and with it mounting liabilities and financial stress on investor-owned utilities in the state,” according to a note last week from Fitch Ratings.

Clean-energy risk

A bankrupt utility could hamper California’s fight against climate change.

- The state passed a mandate last year to require that all California electricity come from wind, solar and other zero-carbon sources by 2045. PG&E hit the 2020 goal of 33 percent renewables back in 2017, so it’s actually ahead of the game, but whether a bankruptcy will delay further progress is uncertain.

- The state requires utilities to buy steadily increasing amounts of renewable power while also helping to deploy electric-vehicle charging stations and make homes more energy efficient. Again, it’s unclear what a bankruptcy would do to these goals. NextEra Energy Inc., the largest U.S. renewable-energy provider, indicated Friday that a bankruptcy could chill investments in wind and solar in the state.

- Analysts speculate that PG&E could use a bankruptcy to renegotiate some of its older renewable-power purchase agreements, signed when wind and solar power cost far more than they do today. NextEra Energy Inc. asked federal regulators to rule that the utility can’t change the agreements. Late Friday, the Federal Energy Regulatory Commission said it shares “concurrent jurisdiction” with bankruptcy courts over those types of contracts.

- Changing the deals could, in turn, jeopardize repayment of loans that the federal government made to renewable power projects under the same stimulus program that backed ill-fated solar manufacturer Solyndra.

Changing the landscape

The type of utility that will emerge from a bankruptcy could look completely different. California regulators were weighing whether the company needed to be broken up or taken over by the state even before PG&E announced its intention to file.

- San Francisco officials are debating whether their “community choice aggregation” program, which already buys power for the city’s residents, should purchase PG&E’s local equipment. If other community choice programs follow suit, much of PG&E could be replaced by a constellation of publicly run utilities.

- PG&E could sell off its historic headquarters in space-starved downtown San Francisco. Estimates say it could be worth $1 billion.

--With assistance from Romy Varghese, Allison McNeely, Mark Chediak and Christopher Martin.

To contact the reporter on this story: David R. Baker in San Francisco at dbaker116@bloomberg.net

To contact the editors responsible for this story: Lynn Doan at ldoan6@bloomberg.net, Margot Habiby, Will Wade

©2019 Bloomberg L.P.