Alibaba's Financial Superstar is Shining Once More

(Bloomberg Opinion) -- Alibaba Group Holding Ltd. put in the kind of earnings performance that will satisfy the bulls (of whom there are many) yet support the bears (whose headcount is smaller).

China’s dominant purveyor of online commerce posted growth that highlights the weakness in its traditional businesses of selling ads to its online merchants, and collecting commissions from transactions. The latter climbed by just 23%, the slowest growth since Alibaba started providing figures two years ago.

It was only because of the massive expansion of its direct-sales, supermarket and groceries businesses that revenue wasn’t a total disaster. In the end operating income, excluding one-time items from a year ago, rose 27%. That’s the biggest improvement in two years, which says a lot about Alibaba’s recent performances.

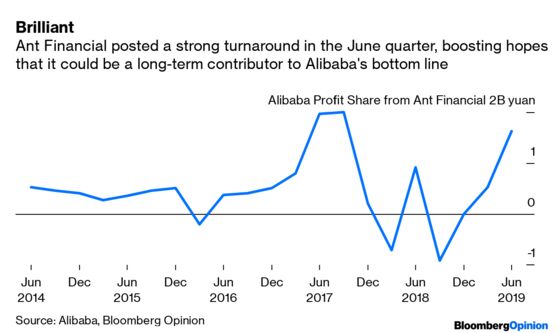

If investors really wanted something to cheer about then the financial wunderkind Ant Financial delivered. The Alibaba affiliate, which operates the e-commerce giant’s Alipay payment service, tripled its operating income from the prior quarter, according to data in Thursday’s financial report. Alibaba recognizes royalty fees, as well as those for software and technology services, as part of its profit-sharing arrangement with Ant.

At 1.63 billion yuan ($237 million), Alibaba’s share of Ant’s profit was the highest in almost two years. In three of the past eight quarters, Ant ran at a loss or provided zero earnings to Alibaba, according to the data. Despite this uptick, Ant’s contribution to Alibaba’s bottom line remains minor at around 7% of operating income. It could shrink again if Alibaba’s e-commerce business dwindles.

Yet Ant has plans to expand its reach throughout China’s economy, including moves deeper into wealth management and other financial products. This could make it relatively robust against any weakness in online and offline commerce should a macroeconomic slowdown continue.

Given Alibaba’s moves to broaden its business into offline shopping, cloud computing and entertainment, investors may not need to get panicky about retail just yet. But when that time comes, Ant may have have grown large enough to shine a bright enough light across the rest of the business.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2019 Bloomberg L.P.