Citi Wants to Bring Credit Card Perks Like Miles to Bank Accounts

Airline Miles for a Bank Account? Citi Vies With Goldman Online

(Bloomberg) -- As the world’s biggest credit-card issuer, Citigroup Inc. has enough plastic in American wallets to tile a path from its New York headquarters to the southern tip of Florida.

Yet many of those 28 million clients park their savings elsewhere.

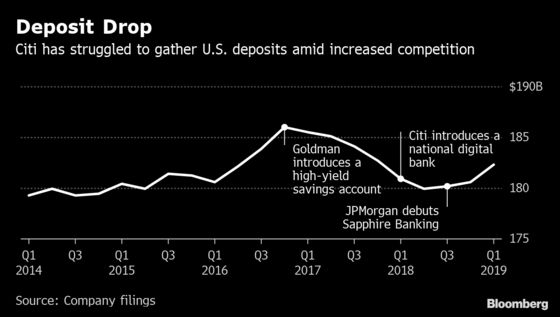

The gap between Citigroup’s credit-card strength and the rest of its retail banking franchise has grown starker in recent years: Citigroup’s deposits from U.S. consumers shrank by $5.4 billion in 2017 and 2018 as a slew of competitors launched or expanded digital platforms. Goldman Sachs Group Inc., for example, has amassed tens of billions of dollars in retail deposits, mostly from the U.S., since opening an online bank dubbed Marcus in 2016.

Now, Citi is fighting back.

After quiet experiments, the firm is expanding perks designed for credit cards to encourage sales of other banking products. In recent months, the company privately offered some cardholders 30,000 airline points to sign up for an online checking account. And this quarter, it plans to enhance its Thank You and Double Cash reward programs for select cardholders to encourage them to sign up for more products and services.

Executives are hoping Citigroup’s card dominance will propel a new digital banking platform, launched last year, to build it into a juggernaut.

“We go in already having these established Citi customers,” Chief Executive Officer Michael Corbat told investors on an April 15 conference call. “We know who they are, we know what they spend on, we know who their bank is, we’ve seen their payments come in if it’s not us. And we think we’ve got the ability around our value proposition to target them with offers.”

Citigroup’s strategy shows the advantages that large traditional banks wield as they look to fend off disruptors chasing billions of dollars in annual revenue. While new entrants have proven it’s possible to snap up customers with lower-cost technology, giant banks have ample resources to roll out counter offers, as well as relationships with millions of Americans and decades of data on their habits.

Early Success

Early testing proved promising, Corbat said. Digital deposits -- those gathered in accounts opened outside branches -- jumped in the first quarter by about $1 billion, more than what it collected that way all of last year, Chief Financial Officer Mark Mason said. More than half came from outside the six metropolitan areas where the bank operates most of its U.S. branches.

That drove a turnaround: Total U.S. consumer deposits rose 1 percent during the first quarter, after five straight quarters of declines.

Aside from Silicon Valley startups, an array of financial services firms born outside of traditional consumer banking have sought to mop up deposits in recent years, taking advantage of technology making it easier to verify and approve customers online. Some of the largest entrants, such as Goldman Sachs and American Express Co., have lured consumers by offering competitive interest on savings. Others focus on perks. Discover Financial Services, for example, offers online accounts with a debit card generating 1 percent cash back on purchases.

Citigroup’s strategy may help it come closer to a target set in 2017 to boost revenue from the consumer division by $5.5 billion to about $38 billion by 2020. Last year the bank acknowledged it had fallen behind on that goal.

`Buying’ Customers

Still, some analysts are skeptical that credit-card perks are a sensible way to lure consumers to a digital bank. Online customers are notorious for chasing rewards, shifting their money to other lenders once they’ve scored rich perks for signing up, or to nab a higher interest rate on their savings.

“All you’re doing is basically buying market share and buying customers, but if you can’t keep them, then the money you just spent is not worth it,” said Alyson Clarke, principal analyst at Forrester Research Inc. Offering a higher interest rate, for example, may boost market share, she said. “But it’s not sustainable over the long term.”

When Citigroup launched its digital bank platform last year, its overhauled app let customers open an account within minutes. That came with normal bells and whistles, such as the ability to pay bills, make mobile check deposits and obtain free access to the bank’s 65,000 ATMs.

Citigroup also rolled out a high-yield savings account similar to offerings from Goldman Sachs and AmEx, making it available for depositors outside its branch footprint in New York, Chicago, Miami, Washington, Los Angeles and San Francisco. The new account offers customers in certain zip codes 2.36 percent interest, according to data posted on Bankrate.com. The bank’s website shows branch customers, in contrast, may earn less than a 10th of that on standard savings accounts.

Harder to Leave

To be sure, branchless entrants aren’t the only ones making Citigroup compete for deposits.

Larger lender Bank of America Corp. launched its Preferred Rewards program in 2014, offering people who meet certain deposit criteria perks such as discounted stock trading and better interest rates. JPMorgan Chase & Co. debuted Sapphire Banking last year, building on the success of its Sapphire Reserve Card.

“A lot of it is leveraging what they know about the customer, particularly on the credit-card side,” said Jesse Rosenthal, senior analyst at CreditSights. And “by building products on each other you make it cost the customer to leave.”

To contact the editor responsible for this story: David Scheer at dscheer@bloomberg.net, Steve DicksonMichael J Moore

©2019 Bloomberg L.P.