Rally in Indian Bank Debt Under Threat on Higher Defaults

A rally in the debt of Indian banks is running up against concern they’ll need to take on greater risks.

(Bloomberg) -- A rally in the debt of Indian banks is running up against concern they’ll need to take on greater risks as the world’s worst bad debt pile is set to weaken further.

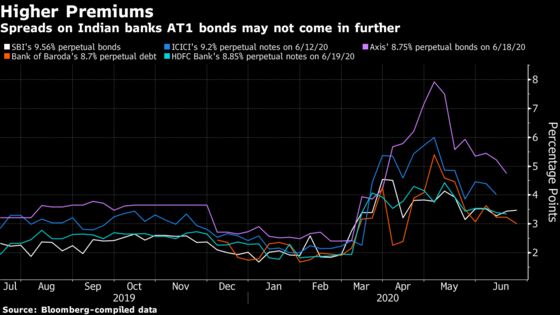

While average premiums on rupee-denominated Additional Tier 1 bonds of the five biggest Indian banks have fallen to about 195 basis points from the end of April, they are still up some 123 basis points this year. And some investors say the rally has little room to continue amid concerns India companies are getting downgraded like never before.

Prime Minister Narendra Modi’s $277 billion stimulus package is heavily reliant on more lending from state banks as he seeks to revive a sagging economy. Indian banks need to build up risk buffers to cushion against an impending jump in corporate defaults tied to the pandemic, as McKinsey & Co. forecasts an increase in the country’s bad debt ratio, which is already at 9.3%.

“I don’t expect spreads on banks’ Additional Tier 1 debt to compress from current levels due to the risky nature of these bonds and the worsening bad loan problem at lenders which will keep demand low for such debt,” said Aneesh Srivastava, chief investment officer at Star Health and Allied insurance Co. “It’s rather time to exit banks’ AT1 bonds.”

India’s bad debt ratio may rise by another 700 basis points due to the coronavirus crisis, according to McKinsey. The country’s lenders need to raise $20 billion of capital over the next year, of which state banks will require $13 billion, to build up cash cushions, Credit Suisse Group AG estimates.

Sentiment toward lenders’ perpetual notes, banks’ first line of defense against financial shocks after equity, weakened in March when the government wrote down the bonds of India’s fourth-biggest private lender in an unprecedented move. Creditors’ wariness deepened as a large mutual fund shut six debt plans in April and on concerns a six-month deferral of loan repayments until the end of August hides the extent of woes faced by pandemic-hit borrowers.

While a central bank rate cut in late May helped spreads to stabilize, they may not come in much further, investors said. And it’s just not the bond market which is cautious. India’s benchmark bank equity index has fallen about 32% since the start of the year, outpacing the 15% drop in the broader market.

“Bitter experience of the past, and concerns asset quality of banks will worsen further after the loan moratorium is withdrawn will keep demand for lenders’ Additional Tier 1 bonds low,” said Mahendra Jajoo, chief investment officer for fixed income at Mirae Asset Investment Managers India Pvt. “For now, we will not buy banks’ capital bonds as the situation remains grim.”

©2020 Bloomberg L.P.